Most startup money problems show up late. Predictive risk analytics helps you spot them earlier.

If I had to sum up the article in a few lines, it would be this:

- Predictive risk analytics looks ahead, not back

- It helps startups flag cash shortfalls, runway pressure, churn, payment delays, fraud, and cost overruns

- It works best when I tie it to one clear finance decision

- The first step is not a fancy model. It’s clean data, steady labels, and clear actions

- For many startups, the best place to start is cash flow and burn forecasting

Put simply, this is about using past and live finance data to estimate what may go wrong next - before it hits the bank account.

A few points matter most:

- Standard reports show what already happened

- Predictive models estimate what is likely to happen next

- Common model types include:

- classification for late payments or churn

- regression for burn or revenue forecasts

- anomaly detection for fraud or odd spending patterns

- Good outputs only matter if they lead to action, such as:

- slowing spend

- changing collections priority

- reviewing fraud alerts

- adjusting hiring plans

The article also makes one thing very clear: bad data ruins the result. If bookkeeping is messy, tags change often, or timestamps are missing, the model learns noise instead of patterns.

Here’s the short version of what startups should do first:

| Area | What to do |

|---|---|

| Start point | Pick one high-cost risk like cash flow gaps or churn |

| Data | Use clean AR/AP, revenue, payroll, bank, and headcount data |

| Model | Start with the simplest model that answers the question |

| Action | Set a rule for what happens when risk crosses a threshold |

| Review | Check model drift and calibration every month |

The core idea is simple: if a prediction does not change what I do next, it is just extra work.

Below, the article explains where predictive risk analytics fits in startup finance, which data and models matter, how to roll it out without building too much, and which early mistakes to avoid.

Why Every Org Should Be Investing in Predictive AI

sbb-itb-17e8ec9

What Predictive Risk Analytics Means in a Startup Finance Context

Predictive Risk Analytics vs. Standard Reporting: A Startup Finance Guide

Predictive risk analytics uses historical and live data, statistical models, and machine learning to estimate the odds and impact of future financial problems.

For startups, that usually means one thing: seeing trouble before it shows up in the bank account.

It helps teams forecast fast-moving revenue, spending, and customer behavior. That includes cash shortfalls, runway pressure, churn, and payment delays, even when the company has only a limited operating history.

The aim is simple: make better decisions. Founders can estimate future outcomes with measurable accuracy and act sooner, not after the damage is done.

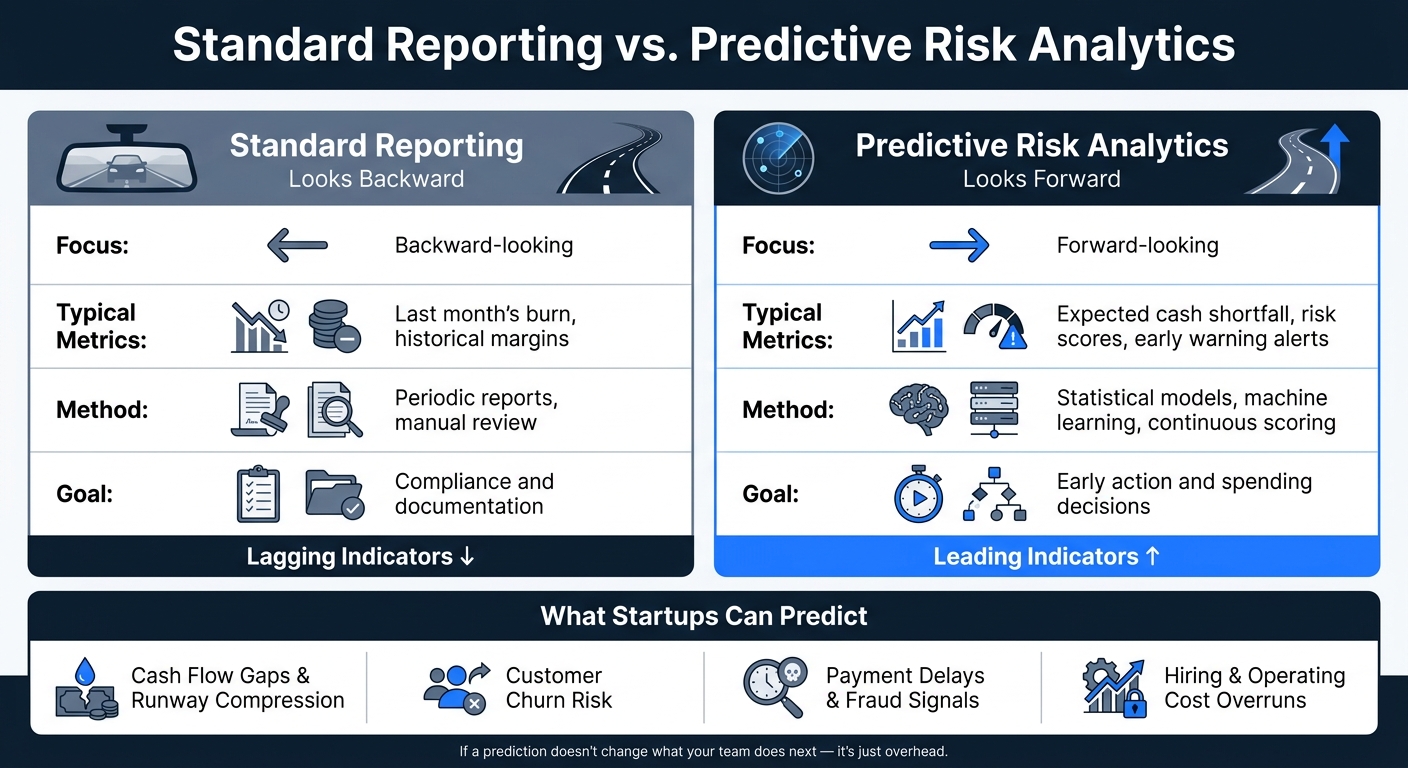

How It Differs from Standard Reporting

Standard financial reporting tells you what already happened. Predictive risk analytics tells you what’s likely to happen next.

That timing gap matters a lot.

Standard reporting is about looking in the rearview mirror. Predictive risk analytics is more like looking a few miles ahead on the road. One shows where you've been. The other helps you avoid the next problem.

| Standard Reporting | Predictive Risk Analytics | |

|---|---|---|

| Focus | Backward-looking | Forward-looking |

| Typical Metrics | Last month's burn, historical margins | Expected cash shortfall, risk scores, early warning alerts |

| Method | Periodic reports, manual review | Statistical models, machine learning, continuous scoring |

| Goal | Compliance and documentation | Early action and spending decisions |

The big shift is moving from lagging indicators to leading ones. That's what makes predictive analytics so useful in startup finance.

Instead of reacting to a cash crunch after it hits, a founder can adjust spend or extend runway before the gap opens up.

What Types of Risk Startups Can Predict

Predictive models don't stop at one part of the business. Startups can use them across several practical risk areas:

- Cash flow gaps and runway compression - spotting when and where cash may run short before it turns into a crisis

- Customer and churn risk - flagging which accounts are likely to churn in the coming weeks

- Payment delays and fraud signals - detecting transaction-level anomalies or patterns that come before late payments or fraudulent activity

- Operating risks - forecasting cost spikes tied to hiring timelines or vendor costs

That level of detail turns a forecast into something a team can actually use. Instead of a vague warning, you get signals tied directly to cash flow, customer behavior, and operations.

These are often the first risks startups model because they show up fast and hit the business where it hurts most.

Where Startups Use Predictive Risk Analytics

Startups get the most out of predictive risk analytics when they use it in repeat decisions tied to cash, customers, operations, and reporting. These are the areas where small misses can turn into big problems fast.

The table below shows the startup use cases you’ll see most often, the data behind them, and the decisions they help shape.

| Use Case | Data Inputs | Prediction Output | Business Impact |

|---|---|---|---|

| Cash Flow & Burn | AR aging, vendor payment history, historical burn, transaction volume | Funding gap alert, reserve requirements, payment delay probability | Extended runway, improved capital planning |

| Customer & Payment | Payment history, transaction volume, behavioral signals, delinquency patterns | Late payment score, churn risk score, probability of default | Reduced bad debt, better collections prioritization |

| Fraud & Security | Device anomalies, failed logins, transaction volume, interaction sequences | Real-time risk score, fraud probability, anomaly alert | Fewer chargebacks, lower analyst workload, preserved customer trust |

| Operating & Hiring | Headcount costs, software utilization, system usage data, vendor performance | Capacity overrun alert, vendor disruption risk, likelihood of cost overrun | Optimized spend, stronger operational controls |

Cash Flow, Burn, and Runway Forecasting

Cash flow is usually the first place startups apply predictive risk analytics. The reason is simple: the data is often already there, and the pressure is immediate. Most teams start here because they can connect the model to day-to-day finance decisions without building a huge system from scratch.

A model based on accounts receivable aging, vendor payment history, and historical burn can spot slow-paying customers early. That gives founders more time to step in before runway gets tight.

"The business value comes from timing. If you can detect risk earlier, you can set limits sooner, route alerts faster, strengthen controls earlier, and preserve cash." - Jeffrey Hammel, CFO

Customer, Payment, and Fraud Risk

After cash flow, the next place startups tend to see strong signals is customer and transaction behavior. Models can score invoices for late payment risk and score accounts for churn risk. That gives collections and customer success teams a clearer way to decide where to focus first.

Fraud detection follows the same pattern. Instead of asking a team to review every transaction, the model flags anomalies based on device patterns, login behavior, or transaction volume. That cuts manual work and helps protect revenue.

Hiring and Operating Risk

The same approach also works inside the business. Hiring and operating decisions can create cost or capacity risk long before the damage shows up in a monthly report.

Headcount costs, software utilization, system usage data, and vendor performance can all be modeled to estimate the chance of a cost overrun or vendor disruption before a decision is locked in. In plain English, teams get faster decisions and a clearer view of risk before committing time or money.

What Data and Models Startups Need

After you figure out where predictive risk analytics can help, the next step is simpler: what data do you need, and what kind of model should you use?

It starts with the data. Strong predictions usually come from clean, consistent inputs before anything else.

The Minimum Data Foundation

Risk signals only work when the data underneath them is clean, current, and labeled the same way over time. For most startups, the core inputs are bookkeeping, bank and card activity, payroll, revenue, AR/AP, tax, and headcount data.

Models also need three connected kinds of data:

- Outcomes: past events such as confirmed fraud, defaults, or missed payments

- Exposures: what was at risk and for how long

- Leading indicators: signals like transaction velocity, utilization changes, and delinquency patterns

Two operating habits matter just as much as the raw data: fast month-end closes and a stable chart of accounts. If expense categories move around or definitions change from quarter to quarter, the model won’t learn the pattern you want. It will learn the mess.

"If your definition of fraud changes every quarter... your model will learn noise and call it signal." - Jeffrey Hammel

Which Model Type Fits Which Risk Question

Once the data base is in place, the next job is matching the model to the business question. Startups don’t need to know every modeling method. They just need to know what each model is meant to answer.

| Model Type | Question It Answers | Finance Team Output |

|---|---|---|

| Classification | Will this payment or customer be late? | Risk scores used to prioritize collections or adjust credit terms |

| Regression | How large will next quarter's burn rate or revenue be? | Dollar estimates used for runway planning and budget allocation |

| Anomaly Detection | Is this transaction or expense pattern unusual? | Real-time fraud, billing, or audit alerts |

For many startups, logistic regression is a practical place to start for classification. It’s fast, stable, and easy to explain to stakeholders or auditors.

One more thing matters here: define the decision before you build the model. If the action isn’t clear, your thresholds and metrics will miss the mark.

Once the model type is clear, the next step is deciding how that output will change a weekly or monthly decision.

How to Put Predictive Risk Analytics into Practice Without Overbuilding

Once you know the model type, the next step is simple: tie it to a real finance decision. Start with one decision that matters. The model should support the action, not run the show.

For startups, predictive risk analytics should help teams respond to cash flow gaps, runway pressure, collections risk, and churn. It shouldn’t turn into one more reporting layer that eats up time.

A Simple Rollout Plan for Founders and Operators

Start with one or two decisions tied directly to survival, like cash flow gaps or runway risk. Focus on the risk that would hurt the business most if you spotted it too late.

Then keep the rollout tight:

- Define the decision first: What event are you trying to predict? Over what time horizon? For which accounts? And what action comes next?

- Check your data before you build. Make sure the data is clean, labeled, and time-stamped in a consistent way. You also need enough business context to explain what’s going on.

- Use the simplest model that can support the decision and is easy to explain, validate, and monitor.

- A forecast only matters when it triggers a specific response. Set alert thresholds based on the cost of acting now versus waiting. That’s the point where a credit hold or hiring freeze can materially change the outcome.

- Track calibration and drift monthly; retrain when performance drops. Use a drift metric such as PSI to catch problems before they hit the business.

How to Use Predictions in Weekly and Monthly Decisions

Once the model is live, work its outputs into the finance rhythm you already have. A forecast pays off only when it changes what the team does next.

In weekly reviews, watch live signals like transaction velocity, failed logins, and utilization shifts. These are early signs that can help teams route alerts faster and protect cash.

In monthly closes, check calibration. In plain English, look at whether predicted probabilities line up with actual outcomes. It’s also a good moment to review whether the model is still behaving well across key segments.

The shift here is practical. You move from "What went wrong last quarter?" to "Which exposures are most likely to break next?" In that setup, predictive risk analytics works as a decision-support tool, not extra reporting overhead.

Common Mistakes and Key Takeaways

What Startups Get Wrong Early On

Startups often trip over the same early issues: incomplete bookkeeping, messy revenue tagging, and missing timestamps. When that happens, the model doesn't learn risk patterns. It learns noise.

The answer isn't a more complex setup. It's cleaner data and one clear use case.

Each score should feed into a decision, not stand on its own as the final word. A prediction only helps if it changes what finance does next, like:

- setting collections priority

- tightening spend control

- sending a case to fraud review

The bigger problem usually isn't just weak predictions. It's how teams act on them.

Another common mistake is chasing broad detection rates. On paper, wide coverage sounds good. In practice, it can bury your team in false alerts while the risks that matter most slip past. You're better off focusing on one or two signals tied straight to a decision that changes the result.

Model drift is also easy to miss. Product mix changes. Customer behavior shifts. Spend patterns move around. If the model isn't checked, it goes stale. Track calibration every month - that is, whether predictions still line up with actual outcomes - and retrain when performance drops. That's why the best systems stay simple, watched closely, and tied to action.

Before You Start

Start with the risk that costs you the most, whether that's a cash flow gap, customer churn, or fraud risk. Keep the workflow simple. Make sure each forecast leads straight to a real finance decision.

If a prediction doesn't change what your team does next, it's just overhead.

Clean books and consistent reporting are what make predictive risk models usable.

FAQs

How much data does a startup need to begin?

Startups don’t need a long track record to start using predictive analytics. What matters more is data quality - along with consistency and easy access.

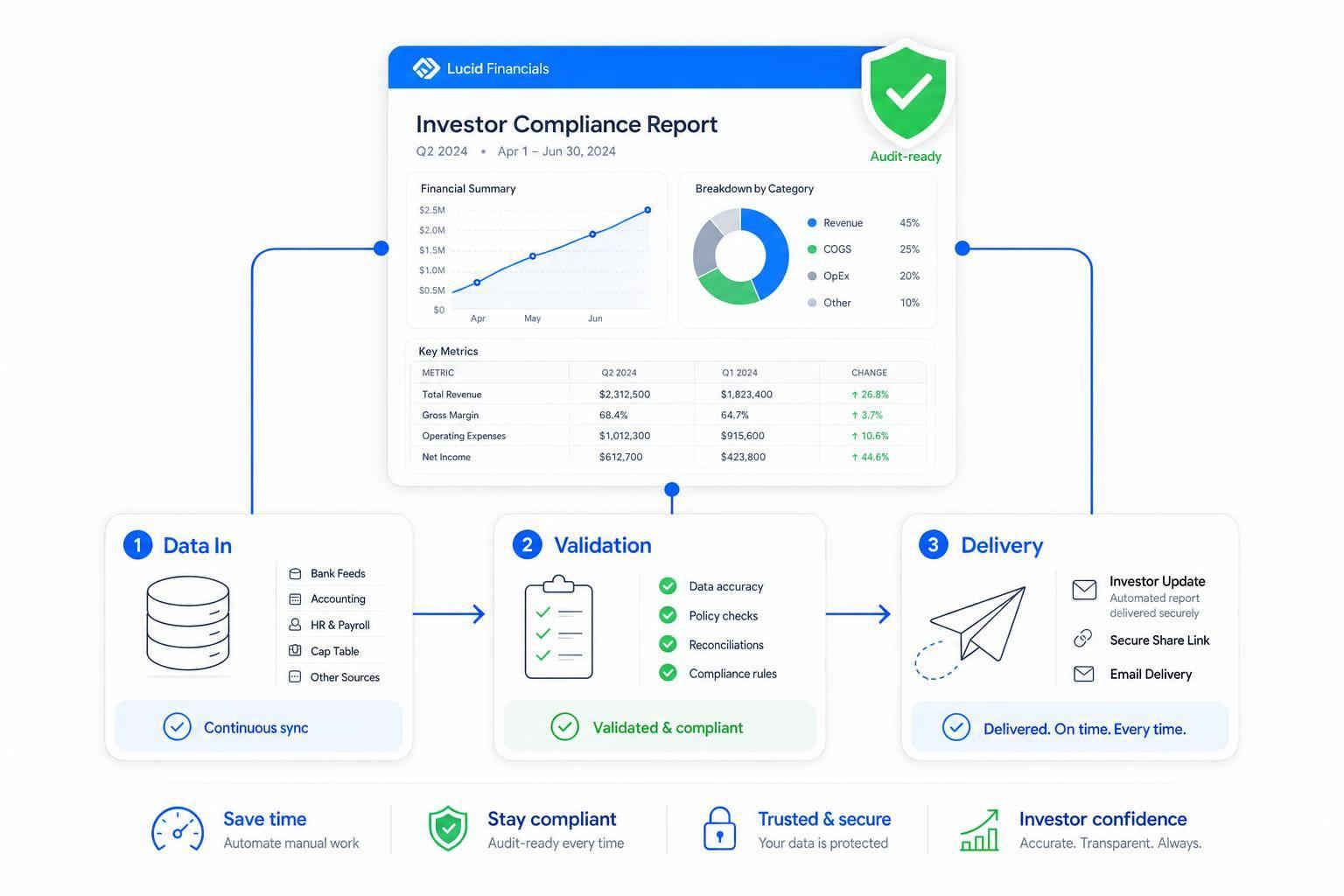

AI-driven platforms like Lucid Financials can pull from multiple data sources to surface insights for younger companies. So instead of worrying about having years of history, startups should get the basics right: use integrated accounting systems, track core operating metrics, and keep data clean enough to work with.

That simple setup gives predictive analytics something solid to build on.

How accurate should a predictive risk model be?

A predictive risk model should deliver measurable, actionable accuracy that beats older methods.

Rule-based systems often land in the 70% to 80% range, but they also tend to produce a lot of false positives. Machine learning models usually reach 90% to 95%. Deep learning models can push that even further, often hitting 95% to 99%.

For startups, the goal isn't perfection on day one. It's steady progress. That usually comes down to two things: strong data quality and regular retraining.

A good way to think about it: don't chase a perfect model out of the gate. Build one that gets better over time and helps teams make better calls now.

Who should own predictive risk analytics at a startup?

At a startup, predictive risk analytics should sit with the founder and executive team. They make the big calls, manage resources, and need a clear view of cash risks before they hit.

That means leadership shouldn’t just review the numbers. They should use them to guide decisions.

The rest of the team also needs enough training to understand what the data is saying. Not everyone has to build models, but people should know how to read the signals and respond.

Tools like Lucid Financials can help by handling automated, investor-ready reporting and real-time scenario modeling.