AI sentiment analysis can help, but it should not drive finance decisions by itself. From the studies in this review, I’d boil it down like this: sentiment tends to be more useful in short windows, during market stress, and when paired with price data, cash data, or other signals.

Here’s the short version:

- News sentiment has shown strong backtest results in some studies, including 51.02% annual excess return and a 1.06 Sharpe ratio in one long-run S&P 500 study.

- Social media sentiment is more noisy. Many models still sit around 50% to 60% out-of-sample accuracy, though some 7-day trend tests reported 86%+ on benchmark data.

- Negative language often matters more than positive language.

- High-volatility periods are where sentiment tends to matter most.

- Model drift is a big problem: some studies estimate 8 to 12 percentage points of accuracy loss per year as market language changes.

- For startups, sentiment is best used as context for timing, valuation windows, and downside planning - not as a stand-alone rule.

If I were using this research in practice, I’d treat sentiment as a support signal:

- Use it to watch for shifts in sector mood.

- Check whether that shift lines up with fundamentals.

- Stress-test cash runway before acting.

- Be extra careful in calm markets, where sentiment often adds less.

That’s the core takeaway: AI can measure market mood at scale, but the signal is uneven, noisy, and highly time-sensitive.

Financial Sentiment Analysis with AI Driven Insights #finance #trading #investing

sbb-itb-17e8ec9

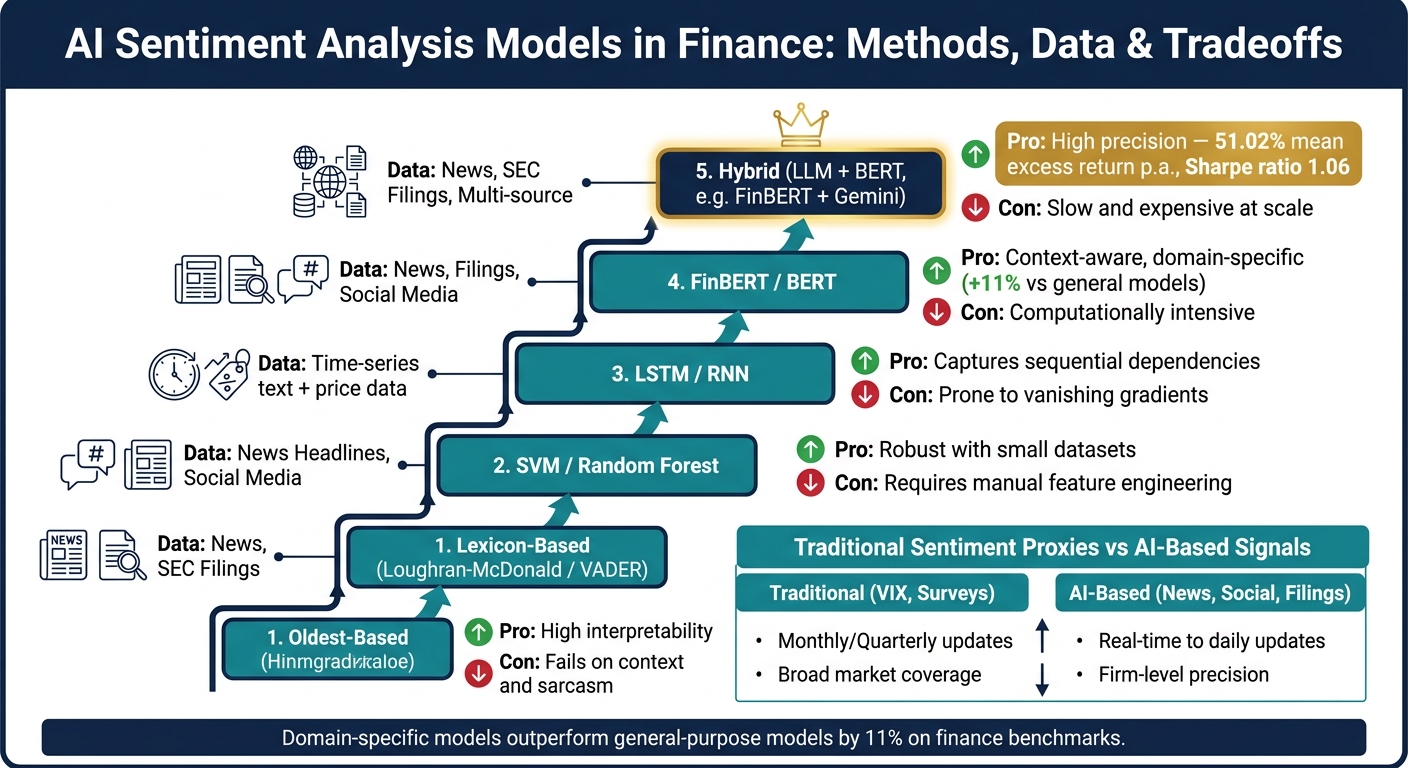

How Researchers Turn Text Into Sentiment Signals

AI Sentiment Analysis Models in Finance: Methods, Data & Tradeoffs

Researchers usually measure sentiment in two ways: indirect market proxies or text-based signals.

Traditional Sentiment Proxies vs. AI-Based Text Signals

For years, researchers had to infer sentiment from broad market proxies like trading volume, IPO returns, the VIX, and consumer surveys. Those measures can still be useful, but many only update monthly or quarterly. They can also move for reasons that have little to do with sentiment itself.

AI-based signals work differently. They pull sentiment straight from text, which means they can update in real time.

| Data Source | Measure Type | Update Frequency | Market Coverage | Common Research Use Case |

|---|---|---|---|---|

| Investor Surveys | Traditional Proxy | Monthly/Quarterly | Broad Market | Long-term sentiment trends |

| VIX / Volatility | Traditional Proxy | Real-time | Equities/Options | Measuring market fear/stress |

| Financial News | AI-Based Signal | Daily/Intraday | Specific Tickers | Event-driven return prediction |

| Social Media (X/StockTwits) | AI-Based Signal | Real-time | Equities/Crypto | Short-term momentum/retail sentiment |

| SEC Filings (10-K/10-Q) | AI-Based Signal | Quarterly/Annual | Public Companies | Fundamental/long-term risk assessment |

Why does this matter? Because the source and the model shape what the signal is good for. Some are better for short-term trading. Others fit longer-horizon risk work. Traditional proxies track the market’s broad mood, while AI-based signals can isolate firm-level sentiment and react much faster.

NLP and Machine Learning Methods Used in the Literature

The tools researchers use have changed a lot over time. Each wave got better at handling context.

The earliest method was lexicon-based scoring. This approach counts positive and negative words with dictionaries like Loughran-McDonald. It’s easy to inspect and simple to audit. The downside is plain: it often misses context, tone, and sarcasm.

Next came classical machine learning models like SVMs and Random Forests. These can work well on smaller labeled datasets, but they need manual feature engineering. In other words, a lot of the setup work falls on the researcher.

After that, deep learning models such as LSTMs started to gain ground. These models read text as a sequence, so they do a better job of tracking how meaning builds across a sentence or paragraph.

Now the field is centered on transformer-based models. Finance-tuned systems like FinBERT, which are pretrained on financial corpora, tend to beat general-purpose models on finance text. That edge isn’t small either: a benchmark of 28 state-of-the-art systems found that domain-specific approaches outperformed general-purpose ones by 11%. Financial language is packed with jargon and context, so generic models often miss the point.

Recent studies also use large language models like Google Gemini or FinGPT as filters for false positives. That setup makes practical sense. Faster models are a better fit for intraday and short-horizon signals, while slower, audited models make more sense for filings and longer-term risk work.

| Model Type | Typical Data Source | Main Tradeoffs |

|---|---|---|

| Lexicon-based (Loughran-McDonald/VADER) | News, SEC Filings | High interpretability; fails on context and sarcasm |

| SVM / Random Forest | News Headlines, Social Media | Robust with small datasets; requires manual feature engineering |

| LSTM / RNN | Time-series text + price data | Captures sequential dependencies; prone to vanishing gradients |

| FinBERT / BERT | News, Filings, Social Media | Context-aware; computationally intensive |

| Hybrid (LLM + BERT) | News, SEC Filings, Multi-source | High precision; slow and expensive at scale |

One result stands out. A hybrid framework that combined FinBERT with Google Gemini 2.5 Flash produced a mean excess return of 51.02% per annum and a Sharpe ratio of 1.06. That kind of precision sounds great on paper, but there’s a tradeoff: these models are expensive to run and slow at scale, which limits their use in high-frequency settings.

The next section tests these signals against returns, volatility, and stress across news, social media, and markets.

What Recent Studies Find Across News, Social Media, and Markets

The main question isn’t whether AI can read text anymore. It’s when that text starts moving markets.

News-Based Sentiment as a Signal for Returns and Financial Stress

News-based sentiment tends to work better for longer-horizon signals and for tracking financial stress. In a 16-year study of S&P 500 constituents, a hybrid FinBERT-Gemini framework delivered a mean excess return of 51.02% per year net of transaction costs, with a Sharpe ratio of 1.06 and a Sortino ratio of 2.61.

That result came from a two-stage filter. The model first screened for likely signals, then applied deeper analysis only to the strongest ones. That makes sense. A lot of financial news is routine, and routine headlines don’t tell you much. By filtering out that boilerplate language before doing deeper reasoning, the system avoids acting as if every headline matters the same way.

Social Media Sentiment in Equities and Crypto

Social platforms tend to reflect short-term herding better than slow shifts in business fundamentals. Positive sentiment can increase herding, which makes short-term price moves bunch together and can chip away at market efficiency over time.

At the same time, not all posts matter equally. One post from an influential account can hit the market like a brick through a window, while hundreds of smaller posts barely leave a mark. To deal with that imbalance, newer models put more weight on posts that are both influential and recent. Using that approach, a FinBERT framework reached average trend prediction accuracy of over 86% on 7-day horizons with the STOCKNET dataset.

Some studies go a step further with event labeling. Instead of tagging posts as just positive or negative, LLM-based annotation sorts them into categories like:

- "Speculation/Rumor"

- "Geopolitical Tension"

That extra context can matter a lot. In one study, the "Geopolitical Tension" label produced a negative Sharpe ratio of -0.661 at a 1-day horizon, and the result was statistically significant at the 95% confidence level.

"Social media sentiment is a valuable, albeit noisy, signal in financial forecasting." - Yueyi Wang and Qiyao Wei

That “noisy” part is doing a lot of work here, and it helps explain why short-horizon prediction is still hit-or-miss.

Where Prediction Improves and Where It Breaks Down

Results tend to look best during high-volatility regimes. Research that used a Temporal Fusion Transformer with FinBERT and ESG data found that sentiment features matter most in turbulent periods, including the COVID-19 shock and banking stress events. In calmer markets, ESG scores did a better job of predicting outcomes. That pattern shows up again and again in the research.

Things get tougher once you look at out-of-sample results. Models may look strong in-sample, but many still have trouble getting much past the 50% to 60% directional-accuracy range on unseen data. In plain English, that means the jump from backtest to live prediction is still hard.

A lot rides on the labels and the clock. If the labeling is weak, or the timing between text and price action is off, the model’s edge can fade fast.

These gains depend on regime, labeling, and timing, which the next section examines.

Limits and Interpretation Challenges in the Research

Those gains are fragile. The big problems are drift, noise, and causality.

Data Bias, Model Drift, and Causality Problems

The hard part isn't just reading sentiment. It's keeping that reading stable while markets shift and language moves with them. Financial language changes over time, so static models wear down. Research estimates that sentiment models lose 8 to 12 percentage points of accuracy per year as market language evolves.

Social media adds another layer of messiness. Twitter/X sentiment systems score 40% to 71% across domains, and even finance-focused models still tend to land around 50% to 60% on social posts. Short posts, slang, and inside-joke language all make the signal less dependable.

"Sentiment analysis even in domain-specific contexts remains a difficult research problem." - Josiel Delgadillo, School of Engineering and Applied Sciences, University of Pennsylvania

There’s also a basic labeling issue. Many benchmark datasets, including Financial PhraseBank, tag text based on human judgment, not on what the market did later. So sentiment often reflects perceived tone, not proof that the tone moved prices. The gap matters. A sentence can sound bullish without leading to a bullish market move.

Studies also need a close read. If they don’t control for look-ahead bias or survivorship bias, the results can look better than they are.

Behavioral Feedback Loops and Governance Concerns

Automated systems can end up amplifying the sentiment they’re supposed to measure. That creates feedback loops and makes cause and effect harder to separate. At that point, the signal may be showing the market reacting to its own reaction.

There’s a quieter issue too: how the model is prompted. Research presented at the 6th ACM International Conference on AI in Finance found that asking LLMs to reason through sentiment step by step with Chain-of-Thought prompting reduced alignment with human expert labels when compared with simpler, more intuitive prompting. Put plainly, the prompting method can change the label itself, which makes the signal less steady.

"Reasoning, whether prompt-induced or built-in, does not improve alignment with human sentiment labels... intuitive, System 1-style prompting better matches human judgment in financial contexts." - Proceedings of the 6th ACM International Conference on AI in Finance

That’s why sentiment should be treated as an input, not a rule that makes decisions on its own. This becomes even more important when sentiment feeds runway planning, hiring, and fundraising timing. A model trained in one market regime can misfire in another, so human review needs to sit above the signal.

These limits hit hardest when sentiment is used in cash-flow, runway, and fundraising decisions.

What These Findings Mean for Startup Financial Planning

Using Market Sentiment as Context for Runway and Fundraising Decisions

This research starts to matter when founders use sentiment to make timing and risk calls.

Studies show that small, young, and hard-to-value firms are the most exposed to sentiment-driven mispricing. And that mispricing can open short fundraising windows. If sentiment around your sector turns upbeat, valuations can get pushed above what fundamentals alone would support. That lift usually doesn’t last forever. In many cases, reversals show up within 7 to 12 months.

So the issue isn’t whether sentiment can move valuations. It’s whether that move gives you a usable opening.

A good rule of thumb: watch for sentiment that isn’t explained by fundamentals. If enthusiasm jumps in your sector and there’s no clear business reason behind it, that may be a better moment to raise than waiting for a cleaner setup. On the other hand, when volatility jumps, sentiment should move down the priority list. That’s when founders need to spend more time on cash preservation and downside planning.

Sentiment can help you decide when to speed up a fundraising process or put runway assumptions under pressure. But it only earns a seat at the table when the signal is strong enough to affect the decision.

How Lucid Financials Fits This Research Context

Sentiment is only useful if you can tie it back to your current cash position.

That’s where Lucid Financials fits in. It connects outside sentiment context with real-time books, cash flow, and scenario modeling, so founders can react to timing signals using current internal numbers, not guesswork.

Conclusion: What the Research Supports Today

The current evidence points to sentiment as a secondary signal, with the most use in short time horizons and in stress periods. In high-volatility markets, technical indicators often beat sentiment-only methods. And even with domain-specific models, social media prediction accuracy still often lands in the 50% to 60% range.

That means sentiment works best as one input among several. Put it next to cash-flow data, technical indicators, and disciplined scenario planning. On its own, it’s not enough to run decisions.

FAQs

When is sentiment analysis most useful in finance?

Sentiment analysis works best in finance when you treat it like a filter or an early warning system inside a broader decision-making process, not as a trade signal on its own.

It usually matters most for short-term returns, harder-to-price areas like small-cap stocks or younger companies, and periods of market stress, big macro events, or key earnings releases.

Why does social media sentiment perform worse than news?

Social media sentiment often works worse than news because it’s noisier and less tied to actual market risk.

News tends to reflect a more rational view of what’s happening in the market. It usually connects more closely to fundamentals, which is why it can be a steadier signal for valuation.

Social media is different. It can get warped by bot activity, coordinated posting, sarcasm, and herd behavior. One viral post can spark a wave of reactions that has little to do with the asset itself.

That’s why news sentiment is often a more reliable signal for market valuation than social media sentiment.

How should startups use sentiment without overrelying on it?

Use sentiment as a supporting tool, not the thing that makes the call on its own.

For early-stage companies, sentiment scores can swing hard. A small sample size can skew the picture fast, which means those numbers shouldn’t trigger knee-jerk moves. They make more sense inside a broader, repeatable monitoring process.

Think of sentiment as an alpha signal that sits next to your current metrics, not above them. It can help you pressure-test runway assumptions, catch biases like recency bias, and flag sharp changes that deserve a closer look.

Before you change fundraising plans or operating plans, go back to the source material and check what’s actually driving the shift.