A pre-Series A bridge round should buy proof, not just time. If I’m between seed and Series A, I should use bridge money to add 6–12 months of runway, hit a short list of milestones, and start the next round from a stronger position.

Here’s the short version:

- I should look at a bridge when I have about 3–6 months of runway left and I’m close to Series A metrics

- Most U.S. bridge rounds land around $1 million to $5 million

- The main structures are SAFEs, convertible notes, and sometimes short-term venture debt

- I should size the round based on burn, timing, and milestone costs - not guesswork

- I need clean financials, a simple story, and a tight process that moves in about 2–4 weeks

- After closing, I should track the few metrics that matter most, like ARR/MRR, retention, gross margin, and burn multiple

A simple way to think about it: if my company needs 9 months to hit target numbers, plus about 3 months to run a Series A process, I need about 12 months of runway. At a $250,000 monthly net burn, that points to a bridge of about $3,000,000.

Bridge Financing Explained: Short-Term Startup Funding Between Rounds

sbb-itb-17e8ec9

Quick comparison

| Option | Best time to use it | Main upside | Main risk |

|---|---|---|---|

| Bridge round | I’m close to Series A, but not there yet | More time to hit better metrics | Extra dilution and term stacking |

| Start Series A now | My metrics are already near target | I may skip an in-between round | Weak numbers can hurt price and demand |

| Cut burn and wait | Market is rough or I’m too early | No new dilution right now | Slower growth can hurt the next round |

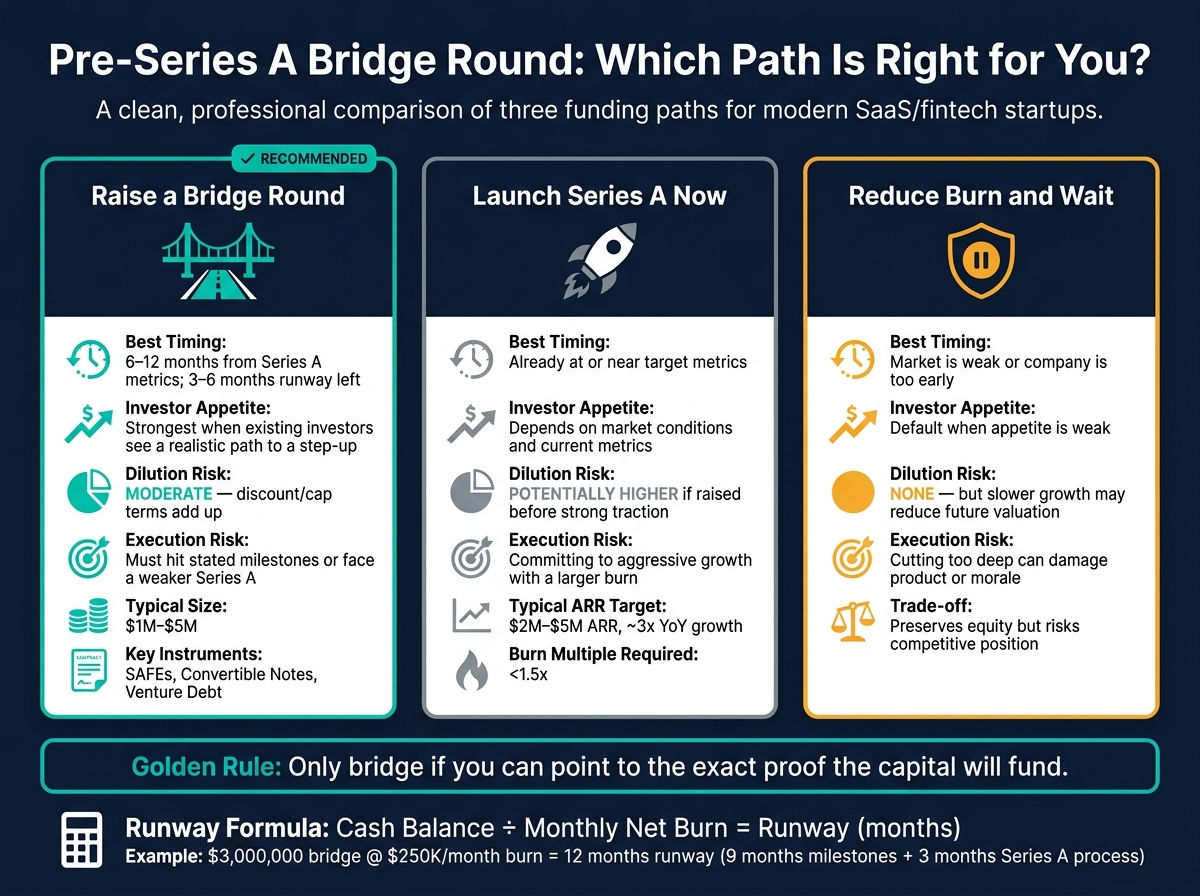

The core idea is simple: I should only do a bridge if I can point to the exact proof it will fund.

1. Decide whether a bridge round is the right move

Pre-Series A Bridge Round: 3 Funding Path Comparison

Make this call fast. Look at runway, burn, and how far you are from the milestones needed for Series A. A bridge round makes sense only if you're close enough that extra time and cash can turn into better terms. If that's the case, the next step is figuring out the round structure and how much to raise.

Check your runway, burn rate, and milestone gaps

Start with the math. Take your current cash balance and divide it by your monthly net burn. That gives you runway in months. If you have about 3 to 6 months left and you're still short of Series A-ready metrics, a bridge round is worth a hard look.

Here’s a simple example. If your net burn is $250,000 per month and you need 9 months to hit your target milestones, plus a 3-month cushion for the Series A process, you need 12 months of runway. That comes to $3,000,000 for the bridge target.

Then get specific about what “Series A-ready” means in your market. Spell out the metrics, then map the hires, product work, and sales goals needed to get there. That’s what makes the ask feel grounded instead of sounding like you just want more time.

Once you know the cash gap, the next issue is whether your current investors are likely to back the round.

Signs that investors will support a bridge

A bridge is much easier to raise when the company is close to Series A shape. Investors, and especially current investors, want to see steady month-over-month growth, strong retention, and proof that the team has delivered on past milestones on schedule.

The smaller the gap to Series A, the easier it is for current investors to say yes and put in more money. Bridge rounds are often funded by existing investors. One of the best signs is simple: your seed investors stay engaged. They take meetings fast, dig into the plan, and hint that they’re open to re-upping.

If investors will only support you at a lower valuation than you want, or they say they need more traction before leading, a bridge can buy time to hit the numbers that support better terms and help you avoid a down round.

Start raising before the company runs low on cash

Don’t wait until the bank account is almost empty. Start planning the bridge when runway drops to 3 to 6 months. Once you’re down to 1 to 2 months, your leverage can disappear in a hurry. In the U.S., fundraising often takes 3+ months from first meeting to money in the bank. Start too late, and it’s not just your terms that suffer. You may run out of cash while the process is still dragging on.

Use this table to compare your options and see which path gives you the best shot at reaching Series A with some leverage still intact:

| Criteria | Raise a Bridge Round | Launch Series A Now | Reduce Burn and Wait |

|---|---|---|---|

| Timing | 6–12 months from Series A metrics; 3–6 months runway left | Already at or near target metrics | Market is weak or you're too early |

| Investor appetite | Strongest when existing investors see a realistic path to a step-up | Depends on market conditions and current metrics | Default when appetite is weak |

| Dilution risk | Moderate; discount/cap terms add up | Potentially higher if raised before strong traction | None; but slower growth may reduce future valuation |

| Execution risk | Must hit stated milestones or face a weaker Series A | Committing to aggressive growth with a larger burn | Cutting too deep can damage product or morale |

2. Structure the Round and Size It Correctly

If a bridge makes sense, the next job is to set it up in a way that protects the Series A. The goal is simple: get enough runway to reach the next funding milestone without turning the cap table into a mess. That starts with picking the right instrument, then sizing the round with care.

Choose Between a SAFE, Convertible Note, or Short-Term Venture Debt

For most pre-Series A bridge rounds in the U.S., founders usually pick from three instruments.

SAFEs (Simple Agreements for Future Equity) are usually the fastest and simplest. They carry no interest, no maturity date, and convert into equity in the next priced round based on a valuation cap and/or discount. They make the most sense when speed and simplicity matter more than creditor-style protections.

Convertible notes come with interest and a maturity date. That gives investors more protection, but it also adds risk for founders. They tend to fit cases where investors want debt-like rights or where the timing of the next round is less clear.

Short-term venture debt is a different animal. It fits companies with revenue that can handle repayment. Interest rates usually fall between 8% and 15% per year, and facilities often include warrant coverage of about 5% to 10% of the loan amount.

| Instrument | Speed | Legal Complexity | Dilution Impact | Key Investor Rights | Typical Fit |

|---|---|---|---|---|---|

| SAFE | Fastest (days) | Low | Cap and discount drive conversion; multiple rounds can stack | Limited, mainly conversion economics and pro rata | Insider bridge rounds; existing investors |

| Convertible Note | Moderate (weeks) | Medium | Similar to a SAFE, but interest accrues into the conversion base | Stronger; creditor status and maturity leverage | Bridge rounds when investors want debt protections |

| Short-Term Venture Debt | Slowest | High | Lower equity dilution, but cash flow is affected by debt service and warrants | Strongest; covenants, security interests, and default rights | Revenue-generating companies with predictable cash flow |

Once you pick the structure, the next fight is in the terms - especially the ones that shape conversion and dilution.

Plan Your Key Terms Before Negotiating

Before you sit down with investors, model the valuation cap, discount rate, interest rate, maturity date, MFN language, and pro rata rights. Of those, the valuation cap usually matters most.

A cap that’s too low means investors convert at a cheaper price than your Series A valuation suggests, which gives them more shares than you planned. For context, pre-Series A valuation caps for software companies in the U.S. often land in the $8 million to $15 million range, with stronger companies toward the top end.

Discounts usually run 10% to 20%. A 20% discount is more common in earlier-stage bridge rounds, where investors are taking on more risk. If you’re using a convertible note, model the interest accrual with care. Even a small interest rate can add more dilution than founders expect by the time the Series A closes.

MFN (Most Favored Nation) clauses and pro rata rights need close attention too. MFN language lets early investors take any better terms you give later investors. So if you issue a second SAFE with a lower cap, earlier investors may be able to match it. That can increase total dilution without much fanfare.

Broad pro rata rights can cause a different problem. If too many small bridge investors have them, Series A allocation gets harder, and your room to bring in a new lead can shrink. If you already have several SAFEs or notes from earlier rounds, clean them up if you can - or at least map out how each one converts before adding another layer. A messy cap table can slow the next round.

With terms mapped out, you can size the raise around the cash needed to hit the next milestone.

Size the Round Based on Runway and Use of Proceeds

Start with current net burn. Then add planned hires and go-to-market spend to estimate projected monthly burn. From there, use the basic formula: Runway (months) = Cash balance ÷ Monthly net burn.

The round should be large enough to get you to the Series A milestone, with enough room left to begin the next raise before runway gets tight. That part matters more than many founders think. You don’t want to be out pitching with only a few months of cash left. That’s when leverage disappears.

The use of funds matters just as much as the total amount. Investors want to see where the money goes and what proof point each dollar is meant to move. General “working capital” language won’t do much work here.

| Category | Purpose | Target KPI |

|---|---|---|

| Sales hires + marketing | Expand pipeline and increase revenue | ARR growth |

| Product + engineering | Ship the features needed to improve the product | Retention or activation improvement |

| Buffer | Cover timing slippage and preserve runway | Series A milestone progress |

Clean books and a simple model make the ask much easier to defend.

3. Get Your Financials Ready and Run the Process Fast

Once the structure and check size are set, shift to diligence prep. Bridge rounds move fast. That means your materials should be ready before you start outreach.

Clean Up Your Numbers Before Reaching Out

Investors expect a monthly accrual P&L, balance sheet, cash flow statement, cap table, runway analysis, burn metrics, and a 12-month forecast, all reconciled to bank accounts. Reconcile every account, keep expense categories consistent, and make sure ARR, MRR, and churn match your billing or CRM data. Revenue recognition should follow U.S. GAAP. Clean financials cut friction and help the round close on schedule.

Use Lucid Financials to get reconciled books and live runway reporting fast, so investors can diligence clean numbers without delay.

Once your numbers are in order, turn them into a short milestone story.

Build a Short Bridge-Round Narrative Tied to Milestones

A strong bridge story answers five questions:

- Why the bridge is needed now

- How much is being raised

- Where the money goes

- Which milestones it unlocks

- When you expect to launch the Series A

The goal is simple: show how this capital leads to a stronger Series A.

Keep it concrete. Instead of "accelerate growth", say: "We're raising a $2,000,000 bridge round via SAFEs to extend runway and reach milestones like $150,000 MRR by 03/31/2027 and $220,000 MRR with gross margin ≥70% by 06/30/2027, with a Series A process planned for Q4 2027." Break the use of proceeds into three to five categories - Sales & GTM, Product & Engineering, Critical Infrastructure, and Contingency - and tie each one to a specific outcome. Investors want to see capital in, milestones out, not a general budget.

Back up every claim with metrics investors already track: ARR, burn multiple, runway, gross margin, and net revenue retention. A one- to two-page financial overview paired with an eight- to ten-slide deck is usually enough.

After the story is set, move fast so momentum doesn't fade.

Run a Focused 2–4 Week Process

Start with existing investors and board members. They can anchor the round the fastest. In the first week, share the package - deck, financial overview, and cap table - and offer pro rata or slightly enhanced allocations to those who move fast.

If you need to go beyond your current base, keep the new investor list tight:

- Five to ten names

- People who know your stage

- People who know your sector

Set a clear timeline up front: "We're targeting soft commitments by 07/24/2026 and final documents by 08/02/2026." Once terms are aligned, sign final docs within 48 hours. That's the danger zone for bridge rounds - after alignment, delays can kill momentum.

Lucid Financials keeps founders ready for live diligence with up-to-date numbers and real-time answers in Slack.

4. Use the Bridge to Set Up a Stronger Series A

After the bridge closes, the work shifts from fundraising to execution. At that point, you’re no longer just trying to bring in cash. You’re trying to show clear proof that the company is ready for Series A.

That’s the whole point of bridge capital. It only helps if it creates new evidence for the next round. If the metrics stay flat, the story stays flat too. And if the story doesn’t change, Series A gets tougher.

Track the Metrics That Matter After Closing

Set your Series A metrics before you spend the first dollar of bridge capital, then review them every month. For B2B SaaS, that usually means MRR, NRR, gross margin, CAC payback, burn multiple, and runway. For AI products, you also need to watch model accuracy, latency, uptime, and inference cost per task.

In the current U.S. Series A market, investors often look for around $2M–$5M ARR, about 3x year-over-year growth, and a burn multiple below 1.5x.

Use the table below to keep spending tied to the milestones investors want to see.

| Metric | Pre-Bridge (07/10/2026) | Bridge Plan | Series A Target |

|---|---|---|---|

| MRR | $60,000 | $120,000 by 01/10/2027 | $220,000 by 07/10/2027 |

| Burn Multiple | 2.2x | <2.0x | <1.5x |

| NRR | 94% | 100% | ≥110% |

| AI Model Accuracy | 93% | 97% by 02/10/2027 | 99% |

| Runway | 7 months | 12 months at close | 9–12 months at Series A kickoff |

A simple rule helps here: if a hire or infrastructure contract won’t move one of these metrics, push it back.

Common Mistakes That Weaken the Next Round

The fastest way to hurt the next round is to spend without milestone discipline. If you raise too little, you may enter the Series A process with less than 8–9 months of runway. That doesn’t look like momentum. It looks like pressure. Over-raising can cause a different problem. If the cap is too high and the numbers don’t catch up, you increase the odds of a flat extension or a down round.

Unresolved SAFEs and convertible notes can also create a mess. Stacking multiple post-money SAFEs without modeling dilution is a reliable way to reach Series A with much less founder ownership than expected. Before you start the Series A process, build a fully diluted cap table as of a set date - say, 07/10/2026. It should show how every instrument converts under different pricing cases. If there are conflicts or overlapping MFN provisions, deal with them now, not in the middle of diligence.

It also pays to watch for spending that doesn’t support the Series A story. Tangential product lines, vanity marketing campaigns, and hires with no direct link to a milestone can drain the bridge without improving the case for the next round. Money spent that way makes Series A weaker, not stronger.

Conclusion: Bridge Capital Should Buy Proof, Not Just Time

The clearest proof is often a simple Thesis vs. Reality slide. It should show each promised milestone, its planned date, and the actual result, using USD figures and U.S. dates. That one slide can show the difference between a founder who merely bought more time and one who earned the next round.

Raise early enough to keep leverage. Keep the structure simple. Size the round based on milestones, not comfort. And stay disciplined on spending after the close. The bridge should buy proof.

FAQs

How do I know if a bridge round is the right move?

A bridge round makes sense when your startup is moving in the right direction but needs a bit more time to hit clear milestones before a larger round. That might mean reaching target revenue, launching a key feature, or entering a new market.

It can also help you keep momentum going or give you breathing room when things don’t go as planned. If you need to extend your runway, this route works best when you have a clear, data-backed plan for making your next round stronger.

What milestones should a pre-Series A bridge fund?

A pre-Series A bridge round should fund clear, measurable milestones that make your startup more attractive for a larger raise while giving you more runway.

That usually means using the money to hit goals investors can see and measure. For example, you might finish product development, reach revenue or sales targets, grow your customer base, or enter new markets.

The key is simple: each goal needs a solid plan behind it. And you need accurate, up-to-date financial reporting to show how the business is tracking.

How can I avoid cap table issues in a bridge round?

Keep a complete, accurate, up-to-date record of every issued share, option, SAFE, and convertible note.

Before you lock in terms, model dilution from a few angles. SAFEs and notes don’t just sit there - they turn into future dilution. Option pool timing matters too. If you expand the pool before closing, more of that dilution can land on founders.

This is one place where messy spreadsheets can come back to bite you. Use professional management tools so your equity numbers stay clean, your records stay current, and investors don’t lose trust in the math.