A $2 million seed round can burn up to $60,000 in legal fees alone. And a lot of that cost shows up late, after the term sheet is signed.

If I were planning a fundraise, I’d budget for more than my own lawyer. I’d also set money aside for:

- Investor counsel fees, often paid by the company

- SEC Form D and state Blue Sky filings

- Cap table and governance cleanup

- IP assignment fixes

- 409A valuation work

- D&O insurance tied to closing

Here’s the short version:

- Legal costs often equal 1% to 3% of capital raised

- Legal can make up 50% to 60% of total deal costs

- Investor counsel caps often land at $10,000 to $25,000 for seed and $25,000 to $50,000 for Series A

- Blue Sky fees can run $100 to $1,000 per state

- Cleanup work often adds $5,000 to $15,000

- A priced round usually costs more than a SAFE or convertible note

The main point is simple: hidden legal costs are usually not random. They come from a short list of places, and I can plan for them early by splitting them into separate budget lines, cleaning up records before diligence, and setting hard fee caps in the term sheet.

That’s what this article covers.

Before You Raise: Legal Essentials for Startup Capital Raising | Sprintlaw

The most commonly overlooked legal and compliance expenses

These costs usually show up in three places: counsel, filings, and cleanup.

Investor counsel fees and deal document costs

Most founders plan for their own lawyer. What often slips past them is that the company usually also covers the lead investor’s counsel fees.

That lawyer reviews and negotiates the deal, and the company often pays those fees up to a cap set in the term sheet. For seed rounds, that cap usually lands between $10,000 and $25,000. For Series A and B rounds, it often sits between $25,000 and $50,000.

The deal structure matters too. SAFEs and notes are usually leaner. Priced equity rounds bring more paperwork: a charter restatement, preferred stock terms, and extra investor documents. That’s where legal bills start to climb.

Total legal spend usually falls in these ranges:

- $20,000 to $75,000 for a priced seed round

- $75,000 to $200,000+ for a Series A

Securities filings, Blue Sky fees, and multi-state compliance

Once counsel fees are on the table, filings add another layer of cost.

After closing, the company has federal and state filing duties. The SEC Form D must be filed within 15 days of the first security sale. On top of that, most states require Blue Sky notice filings in each investor’s state, with fees usually running $100 to $1,000 per state.

Federal filing plus legal prep can add up to about $5,000 for a seed round. And if the startup is incorporated in Delaware but doing business in other states, it may also need foreign qualification filings. Those can add $500 to $1,500 per state.

This is the kind of cost that doesn’t look huge at first glance. Then you stack a few investor states, a filing deadline, and outside counsel time on top of each other, and the bill gets a lot less friendly.

Diligence cleanup, cap table fixes, and governance work

The last hidden cost is cleanup. This is where diligence tends to shine a harsh light.

When investor counsel reviews company records, they want clean paperwork for equity issuances, board actions, IP ownership, and founder agreements. If the company has missing stock issuance records, IP assignment gaps, missing founder vesting documents, or missed 83(b) elections, legal work is needed to fix them.

And timing matters. These problems usually cost more once diligence is already in motion, because they have to be fixed before closing. In plain English: small paperwork misses can turn into expensive fire drills.

The table below shows what cleanup items usually cost:

| Cleanup Item | Estimated Cost Range |

|---|---|

| Cap table corrections | $1,000 – $3,000 |

| IP assignment documentation | $1,000 – $3,000 |

| Board minutes and retroactive consents | $2,000 – $5,000 |

| 409A valuation | $1,000 – $5,000 |

| Typical cleanup total | $5,000 – $15,000 |

A 409A valuation is another cost founders often put off until they can’t avoid it anymore.

How to build a realistic fundraising legal budget

Startup Fundraising Legal Costs by Round Type: SAFE vs. Note vs. Priced Equity

Once you know where the costs hide, the next step is simple: give each one its own line before the round starts.

Budget by round type: SAFE, note, or priced equity

The kind of round you run shapes your legal bill and when those costs land.

SAFEs and notes usually stay lean. Priced equity is a different story. It brings more documents, more diligence, and often investor counsel reimbursement too.

Use separate line items instead of one legal placeholder

One line called “legal” doesn’t tell you much. By the time the round closes, that single bucket often includes a mix of charges that were easy to miss at the start.

Split legal spend into separate budget lines so each cost is visible from day one.

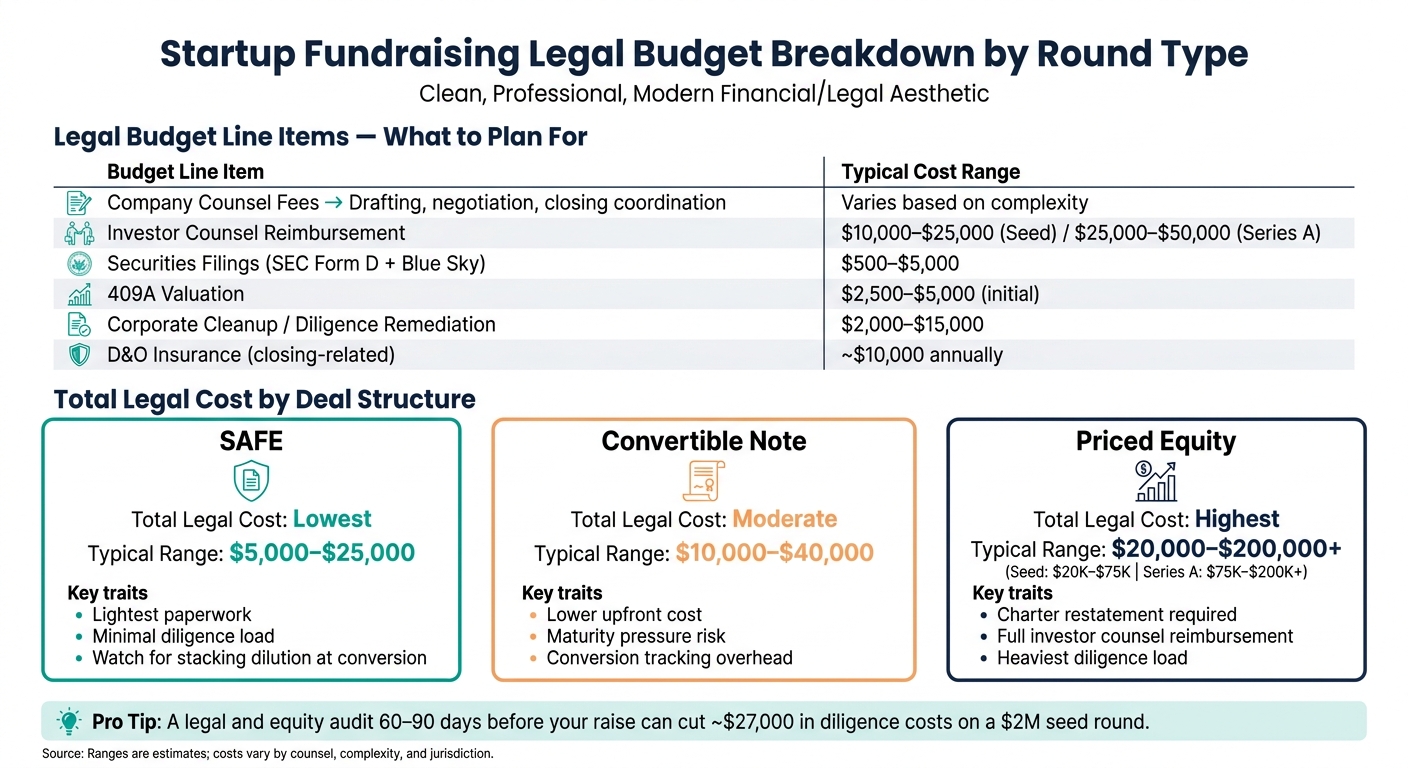

| Budget Line Item | Typical Budget Item |

|---|---|

| Company counsel fees | Drafting, negotiation, and closing coordination |

| Investor counsel reimbursement cap | $10,000–$25,000 (seed) / $25,000–$50,000 (Series A) |

| Securities filings | $500–$5,000 |

| 409A valuation | $2,500–$5,000 (initial) |

| Corporate cleanup / diligence remediation | $2,000–$15,000 |

| D&O insurance (closing-related expense) | ~$10,000 annually |

A few of these costs show up before the money hits your account. Cleanup work, 409A valuations, and filing prep often happen during diligence. That’s why a hard cap on investor counsel reimbursement in the term sheet matters so much. It’s one of the best ways to keep this part of the budget from drifting upward.

Track legal spend alongside runway and close timing

You’ll also want to track these costs next to runway and expected close timing.

Legal work often starts weeks before the invoice lands, so costs can pile up quietly while your runway model looks the same on paper. Track legal accruals every week so they show up in your forecast before close.

sbb-itb-17e8ec9

How to reduce surprises before and during the round

A budget helps. But the bigger win usually comes from cleanup and tighter controls before the round gets busy.

If you don't handle the messy stuff early, legal bills can swell fast. And once diligence starts, small record issues have a way of turning into time-consuming fixes.

Run a legal and equity cleanup before fundraising starts

Fix issues before investors spot them. Once diligence begins, every problem found can add time, friction, and cost.

A pre-raise review should cover charter documents, bylaws, cap table, board minutes, option grants, IP assignments, and major customer or vendor contracts. One point matters a lot here: IP ownership. Every founder, contractor, and early employee should have a signed invention assignment agreement.

"Unsigned invention assignments and undocumented equity issuances turn diligence into expensive cleanup."

It also helps to reconcile every SAFE, note, and side letter against the cap table. If signed documents don't match what the cap table shows, you may end up doing pricey remediation right before closing.

Once the records are clean, the next step is simple: set boundaries before legal work starts to spread.

Set fee caps, scope, and payment responsibility early

Before legal work grows, ask counsel for a written estimate that lays out scope, billing assumptions, and what's included. That one move can cut down on nasty surprises during closing week.

The same rule applies to investor counsel. It's standard for the company to cover the lead investor's legal fees, but that doesn't mean the bill should be open-ended. Negotiate a hard reimbursement cap in the term sheet. And when you set that cap, make sure you know what it covers. Fees only? Or fees plus expenses? That small detail can add thousands of dollars to the final invoice.

Timing matters too. Ask when fees become payable. Some startup-focused firms defer payment until the round closes, which means you can pay from the proceeds instead of current cash.

After the term sheet is in place, the focus shifts to keeping diligence moving instead of letting it drag.

Keep finance, legal, and compliance records investor-ready

Accurate records cut diligence churn and reduce billable hours.

The core records to keep current include:

- cap table

- stock purchase agreements

- 83(b) election filings

- option grants

- 409A valuations

- board minutes

- IP assignments

A ready-to-go data room can save 20 to 40 hours of legal scrambling once an active raise begins.

Clean books and investor-ready reporting also reduce the back-and-forth with counsel. Less chasing, fewer gaps, and fewer last-minute fixes usually mean lower legal spend.

Investors want to see that the company is investable as presented. Investor-ready records send that signal and make it easier to get to close.

Conclusion: Turn hidden legal costs into planned fundraising expenses

Most fundraising legal costs are predictable. The problem is that founders often don't budget for them in a detailed way.

Instead, legal gets lumped into one broad line item. Then the surprise hits later, when that "one cost" turns out to be several different bills. That's why each part of legal spend needs its own line in the budget.

The fix is simple: price each cost before the round opens.

Clean records and early prep do most of the heavy lifting. A legal and equity audit 60–90 days before a raise can cut roughly $27,000 in diligence costs on a $2 million seed round.

The hidden-cost picture also shifts based on the deal structure. Here's the fastest way to think about it:

- SAFE: Lowest legal friction and the lightest cleanup burden, but dilution surprises at conversion can add up fast when multiple SAFEs stack

- Convertible note: Lower upfront cost, but maturity pressure and conversion tracking bring extra risk

- Priced equity: Highest legal spend and the biggest diligence load - manageable only with early planning

No matter which structure you choose, the rule stays the same: itemize legal costs early, cap them, and budget by round type.

FAQs

When should I start legal cleanup before a raise?

Start well before investors get involved. If you try to fix formation problems, cap table mistakes, or missing signatures in the middle of a live round, legal fees can climb, the deal can slow down, and your negotiating position can get weaker.

A early review of your equity and corporate records helps keep the process moving and supports your valuation. Lucid Financials can help by keeping your books clean and investor-ready.

Who usually pays the investor’s legal fees?

In most venture capital and priced funding rounds, the startup is expected to cover the investor’s legal fees. In most cases, that payment is subject to a negotiated cap.

At the early stage, some investors, especially those using SAFEs or convertible notes, may pay their own legal costs instead. That can make a big difference when cash is tight.

To keep costs under control, founders should negotiate the cap upfront and confirm exactly what it includes. For example, does it cover all related legal costs, or just part of the bill? That small detail can save a nasty surprise later.

Are SAFEs always cheaper than priced rounds?

Usually, yes. A standard, clean SAFE financing often costs about $1,500 to $15,000 in legal fees, while a priced equity round commonly costs $20,000 to $150,000 or more.

That said, it’s not always that simple. SAFE costs can climb if you have a long list of investors, complex side letters, or messy corporate records that need to be cleaned up before closing.