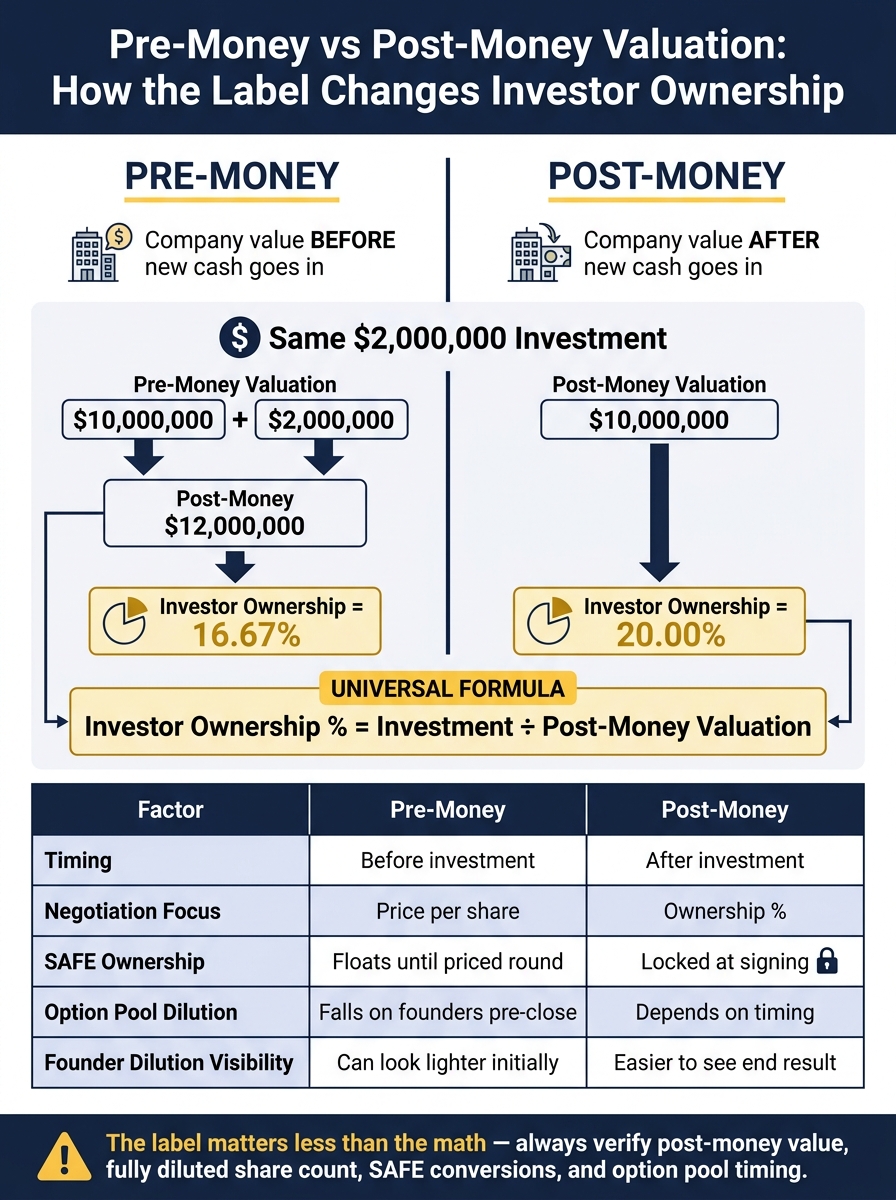

A valuation label can change investor ownership by several points in the same deal. If I invest $2,000,000, I get 16.67% at a $10,000,000 pre-money valuation, but 20.00% at a $10,000,000 post-money valuation.

Here’s the short version:

- Pre-money = company value before new cash goes in

- Post-money = company value after new cash goes in

- Investor ownership = investment ÷ post-money valuation

- Fully diluted shares matter because options, SAFEs, and notes can cut the stake I think I’m buying

- Option pool timing changes who takes dilution

- Post-money SAFEs lock ownership at signing; pre-money SAFEs do not

- Convertible notes depend on caps, discounts, interest, and the priced round math

- Investors also model future dilution, next-round step-ups, and exit returns

Pre-Money vs Post-Money Valuation: Investor Ownership Breakdown

Venture Capital Valuation Explained: Pre-Money vs Post-Money

sbb-itb-17e8ec9

Quick Comparison

| Item | Pre-Money | Post-Money |

|---|---|---|

| Timing | Before new investment | After new investment |

| Ownership effect | Final stake depends on post-round math | Final stake is shown more directly |

| Common negotiation focus | Price | Ownership % |

| SAFE impact | Ownership can move as more SAFEs are added | Ownership is fixed at signing |

| Founder dilution visibility | Can look lighter at first | Easier to see end result |

I’d sum it up like this: the label matters less than the math. If I don’t check the post-money value, the fully diluted share count, SAFE and note conversions, and any pre-close option pool increase, I can misread the deal from day one.

Core Definitions and the Basic Math

Once the terms are clear, the next step is simple: how does valuation turn into ownership?

Pre-Money Valuation vs Post-Money Valuation: What Each Term Means

Pre-money valuation is the company's value before new capital goes in. Post-money valuation is the company's value after the round closes, with that new capital included.

That difference matters a lot. For an investor, it shapes ownership, dilution risk, and upside from the minute the check clears.

How Investors Calculate Ownership from Valuation and Check Size

Most of the deal math comes down to four formulas:

| Calculation Goal | Formula |

|---|---|

| Post-Money Valuation | Pre-Money Valuation + Investment Amount |

| Pre-Money Valuation | Post-Money Valuation − Investment Amount |

| Investor Ownership % | Investment Amount ÷ Post-Money Valuation |

| Price Per Share | Pre-Money Valuation ÷ Pre-Money Fully Diluted Shares |

The key shortcut is this: investor ownership = check size ÷ post-money valuation.

A simple example helps. Airbnb's 2017 Series F closed at a $30.3 billion post-money valuation after a $1 billion raise on a $29.3 billion pre-money valuation.

But that ownership number only means something once you know the full share count.

Why Fully Diluted Share Counts Matter

Investors don't measure ownership against only the shares already issued. They use the fully diluted share count - that means every share that could exist if all options, warrants, SAFEs, and convertible notes were exercised or converted.

Why does that matter? Because more fully diluted shares mean:

- A lower price per share

- More shares issued for the same check

So hidden dilution changes what the investor is actually buying. That's why the cap table needs to be complete before anyone argues about valuation. If the cap table is missing pieces, the ownership math is off.

With the cap table set, the next step is to look at how that ownership moves as round terms change.

How Valuation Levels Affect Investor Ownership and Founder Dilution

Once the math is clear, the next step is simple: how much of the company does the same check actually buy? That answer changes fast when the valuation changes.

Higher vs Lower Pre-Money Valuation at the Same Check Size

At a fixed check size, pre-money valuation directly affects ownership. Here’s what that looks like with a $2 million investment:

| Valuation Level | Pre-Money Valuation | Post-Money Valuation | Investor Ownership % |

|---|---|---|---|

| Higher | $10,000,000 | $12,000,000 | 16.7% |

| Lower | $8,000,000 | $10,000,000 | 20.0% |

Same $2 million check. Different valuation. Different outcome.

At a $10 million pre-money, the investor ends up with 16.7%. At an $8 million pre-money, that same investor gets 20.0%. Lower valuation means the investor buys more of the company, which means founders give up more.

One detail people often miss is the option pool increase. If the option pool expands before closing, the dilution usually falls on founders and existing holders, which lowers the effective pre-money for them.

That’s not just a technical cap table point. Even a small option pool change can shift who takes the dilution hit.

How Post-Money Valuation Sets the Final Ownership Outcome

Post-money valuation shows the investor’s final ownership percentage after the round.

That’s why post-money framing can feel more direct. It locks in the investor’s end stake, so term sheets are often easier to compare side by side. Instead of arguing only about price, both sides can see the ownership result in plain terms.

How Valuation Framing Shifts Negotiation Dynamics

Because ownership is fixed in different ways under each approach, the negotiation changes too.

With pre-money framing, the back-and-forth usually centers on price. With post-money framing, the focus shifts to the investor’s exact ownership percentage. That may sound like a small wording change, but it can change leverage in the room.

So before debating other terms, make sure the framing is clear. If that piece is fuzzy, the rest of the discussion can drift fast.

Those effects get more complicated once SAFEs, notes, and pool adjustments enter the round.

SAFEs, Notes, Option Pools, and Other Adjustments Investors Watch

Pre-Money SAFEs vs Post-Money SAFEs

For investors, the big issue is simple: does this instrument lock in ownership now, or does it leave the final stake up in the air until the priced round?

With a post-money SAFE, the math is direct. Ownership equals the investment amount divided by the post-money cap. So a $1,000,000 investment on a $10,000,000 post-money cap locks in 10% ownership at signing.

A pre-money SAFE works differently. The final ownership stake floats because each new pre-money SAFE changes dilution for everyone. That makes the end result harder to predict and much harder to model cleanly.

| SAFE Type | Ownership Certainty | Dilution Impact | Modeling Ease |

|---|---|---|---|

| Pre-Money SAFE | Floats until the priced round | Shared across founders and all SAFE holders | Complex; requires a full waterfall calculation |

| Post-Money SAFE | Locked at signing | Founders absorb all dilution from subsequent SAFEs | Simple: Ownership = Investment ÷ Post-Money Cap |

That one difference changes who takes the dilution hit.

How Convertible Notes Affect Valuation at Conversion

Convertible notes add another moving part. Ownership depends on both the note terms and what happens in the priced round.

Most notes carry an interest rate of about 8% per year and a maturity date of 12 to 24 months. They also often include a discount, usually 20% off the priced round price, plus a valuation cap.

At conversion, the investor gets whichever leads to the lower share price: the cap-based price or the discounted price. Because most convertible notes use a pre-money valuation cap, the investor's final ownership percentage stays unknown until the company calculates the full converting share count at the priced round.

Option Pool Expansion Before or After the Round

Option pool timing matters because it decides who gets diluted.

If the pool expands before the round closes, new investors price the deal using the larger share count. That means the extra dilution lands on existing holders. Investors usually check whether the quoted pre-money valuation already includes that pool increase, because a pre-close expansion lowers the effective pre-money valuation used to price the round.

That's why pool timing is often one of the first things investors test in the cap table.

Investor Modeling, Forecasting, and the Bottom Line

How Investors Model Future Rounds, Dilution, and Exit Returns

After a round closes, the conversation shifts from price to dilution. Once the post-money valuation is set, investors start modeling what their stake looks like after future rounds - and what it might be worth at exit.

A common approach is the VC Method. Investors estimate the company’s exit value 5–7 years down the road, discount that value by their target IRR, and then work backward to find the highest entry valuation they can justify. So a $20 million post-money seed valuation needs a clear path to a $500 million+ exit just to produce a 25x gross return.

And that math doesn’t stand on its own. It also has to line up with the next fundraise. With median seed pre-money sitting around $16 million and a median Seed-to-Series A step-up of about 2.8x, investors are backing a much steeper hurdle for the next round.

They also run downside cases. If things don’t go to plan, anti-dilution terms can change ownership in a big way and reshape incentives across the cap table.

What Financial Data Makes a Valuation Easier to Defend

To support that forecast, investors want operating data - not just a good story. A valuation is only as strong as the numbers behind it. That usually means close attention to ARR growth, gross margin, burn multiple, CAC, LTV, and a reconciled cap table that accounts for every SAFE, note, warrant, and option.

Lucid Financials helps founders keep clean books, get real-time Slack answers, and maintain investor-ready reporting.

Conclusion: The Ownership Math Matters More Than the Label

Bottom line: investors care less about the label and more about the ownership math. They also need clean data to back it up. SAFEs, convertible notes, option pool timing, and anti-dilution provisions all sit on top of that core math, and each one can shift ownership in a material way. That’s why the cap table and the financial model matter just as much as the headline valuation.

FAQs

How do I verify my true ownership after dilution?

Look past your first check and work out your ownership on a fully diluted basis. That means tying your cap table back to all issued shares, outstanding options, warrants, and convertible securities like SAFEs.

With post-money structures, the investor’s percentage is set up front. So when new shares get issued or an option pool grows, your stake usually takes the hit directly. That’s why clean, up-to-date records matter so much. In the end, your legal documents - not the pitch deck - are what decide your ownership.

When does a pre-money SAFE become riskier for investors?

A pre-money SAFE gets riskier when a company keeps stacking more SAFEs or other convertible instruments before a priced round.

Here’s the issue: the conversion price is based on the company’s capitalization before the new money comes in. So when later SAFEs are added, they can dilute people who invested through earlier pre-money SAFEs.

That means your final ownership stake - and what your return might look like - can stay unclear until the future priced round finally sets the cap table.

Should an option pool be added before or after a round?

This is a key negotiation point. People often call it the option pool shuffle.

In most venture capital deals, investors want the option pool set up or expanded before the round closes, as part of the pre-money valuation.

That timing matters a lot.

If the pool is included pre-money, only existing stockholders take the dilution. If the pool is added after closing, the dilution is spread across all stockholders, including the new investors.

A simple rule of thumb: size the pool based on a realistic 12- to 18-month hiring plan. Don’t pick a number out of thin air. Tie it to the hires you expect to make and the equity you’ll likely need to offer.