Phantom equity plans let employees share in a company's financial success without owning actual shares. Employees receive "phantom units" linked to the company's value, which pay out in cash during events like a sale or IPO. These plans avoid ownership dilution, cap table changes, and legal complexities tied to traditional equity. However, they create cash payout obligations and are taxed as ordinary income, which can be less favorable for employees.

Key Points:

- No Ownership: Employees don't get voting rights or actual shares.

- Cash Payouts: Payments are made in cash, not shares, during exit events.

- Tax Implications: Employees face higher tax rates (up to 37%) compared to stock options.

- Company Impact: Phantom equity is recorded as a liability, which can affect financial reporting.

- Best Fit: Works well for LLCs, S-corps, and companies avoiding ownership dilution or operating internationally.

Phantom equity is practical for businesses prioritizing simplicity and control but may strain cash flow during payouts. Early planning is crucial to avoid financial surprises.

1. Phantom Equity Plans

Ownership and Cap Table Impact

For startup founders, getting a handle on how phantom equity affects their capital structure is key for long-term planning. Phantom equity grants employees "phantom units" tied to the company’s value, but these units don't change the cap table. That means the ownership structure remains untouched. However, when the time comes for cash payouts, those payments reduce the proceeds available at an exit. This clean cap table setup can make investor due diligence during fundraising a lot simpler. On the financial side, phantom equity is recorded as a liability on the balance sheet since it represents a future cash obligation.

Tax and Legal Considerations

Tax and legal details are critical when it comes to phantom equity. Payouts are taxed as ordinary income, which can mean federal tax rates as high as 37%. Compare that to the maximum 20% rate for long-term capital gains, and the tax burden becomes a significant factor for employees. Compliance with IRC Section 409A is another big deal. For instance, if your plan allows the CEO to approve early payouts, it could violate 409A rules. That would trigger immediate taxation on vested amounts and add a 20% excise tax penalty. To stay compliant, companies typically conduct annual 409A valuations through independent appraisers.

"If your plan says the CEO can authorize early payouts whenever they see fit, the plan likely violates 409A." - LegalClarity Team

Beyond taxes and legalities, phantom equity also comes with cash flow challenges.

Cash Flow Implications

Unlike stock options, which are settled with shares, phantom equity involves real cash payouts when units vest. At exit events, companies must pay out all vested phantom units in cash before founders and investors see any proceeds. Additionally, under ASC 718 accounting rules, phantom equity needs to be marked to market at each reporting period. If the company’s valuation has skyrocketed between the grant date and payout, the company must record higher compensation expenses. This can add volatility to financial statements, making financial planning trickier.

These cash flow pressures add to the administrative burden of managing phantom equity plans.

Administrative Complexity

Phantom equity requires ongoing management and careful tracking. Companies need systems in place to monitor vested and unvested units, handle forfeitures, and forecast future cash obligations. When structured as "top hat" plans - restricted to senior executives or highly paid employees - phantom equity avoids most ERISA requirements. The only step is filing a one-time Department of Labor registration within 120 days. For startups with global teams, phantom equity sidesteps the legal hurdles of cross-border securities registration that come with issuing real shares. It’s also a practical option for S-corporations, which are capped at 100 shareholders. Phantom equity lets these companies incentivize more employees without breaching that limit.

sbb-itb-17e8ec9

2. Other Startup Equity Tools (e.g., Stock Options, RSUs)

Ownership and Cap Table Impact

Unlike phantom equity, stock options and RSUs grant actual legal ownership to employees. This means holders get voting rights and access to company records, which adds a layer of complexity. However, issuing these shares comes at a cost - existing ownership is diluted, and the cap table becomes more intricate. This can complicate future fundraising efforts and the overall structure of ownership. The legal and tax implications tied to these ownership rights are worth noting, as they differ significantly from phantom equity.

Tax and Legal Considerations

The tax treatment of stock options and RSUs is more nuanced and, in many cases, more advantageous for employees. For example:

- Incentive Stock Options (ISOs): If held long enough after exercising, employees may qualify for long-term capital gains tax rates (0–20%).

- Non-Qualified Stock Options (NSOs): Taxed as ordinary income at the time of exercise, based on the difference between the strike price and the fair market value.

- RSUs: Taxed as ordinary income when they vest, similar to phantom equity payouts.

For employers, the tax dynamics are reversed. Companies can deduct NSO exercises and phantom equity payouts, but they generally cannot deduct ISOs or traditional stock grants. Additionally, Section 409A compliance applies to stock options, requiring strike prices to match or exceed fair market value at the grant date. This compliance necessitates a formal 409A valuation, regardless of the equity tool used.

Cash Flow Implications

Stock options and RSUs offer a clear advantage for startups with limited cash reserves. Since these instruments are settled in shares rather than cash, they don't create liquidity challenges at exit - unlike phantom equity, which requires cash payouts. Employees gain ownership stakes, while the company retains its financial resources. However, as Matt Schiff of Schiff Executive Benefits aptly puts it:

"Once you give away equity, you've invited someone else into the 'kitchen.' They have voting rights, the right to inspect your books, and a seat at the table for every major decision."

While cash flow is preserved, the trade-off is a loss of some control.

Administrative Complexity

The administrative burden of stock options and RSUs is notably higher compared to phantom equity. These instruments require frequent cap table updates, adherence to securities laws, and shareholder approvals. In some cases, state-level filings may also be necessary. For LLCs, granting actual membership units transforms employees into partners for tax purposes, which means issuing K-1s instead of W-2s and potentially triggering self-employment taxes. For S-corporations, there’s an added risk - issuing shares to the wrong type of shareholder, such as a non-U.S. resident, could jeopardize the company's S-corp status. Phantom equity avoids these pitfalls entirely, as it doesn't involve actual ownership.

| Feature | Stock Options / RSUs | Phantom Equity |

|---|---|---|

| Ownership Rights | Full legal rights, including voting | None - contractual only |

| Cap Table Impact | Dilutes existing owners | No dilution |

| Tax (Employee) | Capital gains (ISOs) or ordinary income (NSOs/RSUs) | Always ordinary income |

| Tax (Company) | Deduction for NSOs only | Full deduction at payout |

| Settlement | Equity-settled | Cash-settled |

| Cash Flow Impact | Preserves cash | Creates cash obligations |

| Administrative Effort | High; legal and securities filings required | Moderate; functions like a bonus plan |

Phantom Equity: Its Advantages and Disadvantages for Incentivizing Employees

Pros and Cons

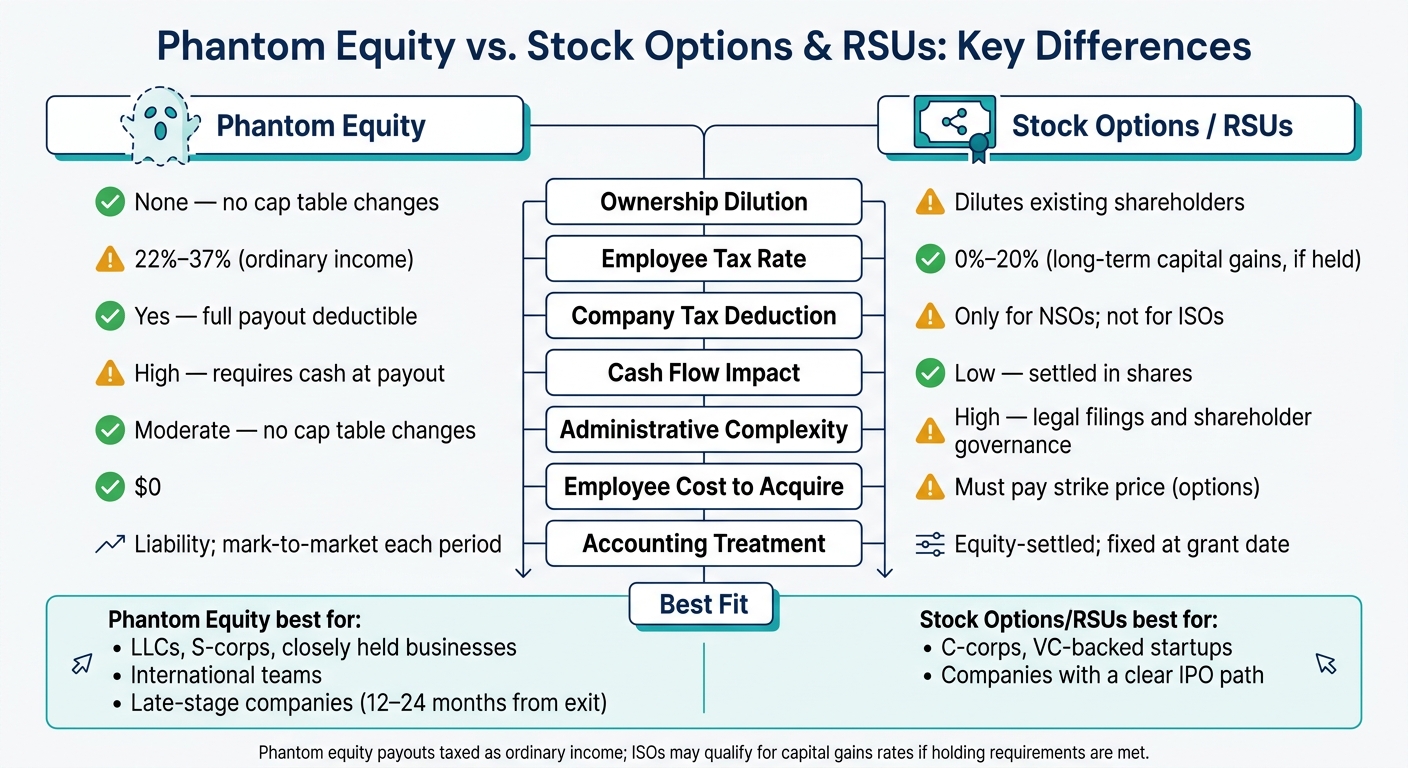

Phantom Equity vs. Stock Options & RSUs: Key Differences

Phantom equity comes with its own set of advantages and challenges, especially when compared to traditional equity awards like stock options or RSUs. Let’s break down the key points.

One major benefit of phantom equity is that it avoids ownership dilution and steers clear of complex legal entanglements. For LLC founders, this is a big deal. Issuing actual equity can turn employees into members, triggering K-1 forms, potential self-employment taxes, and more intricate governance. Jennifer Brits, Partner at Weil, explains it well:

"It's a way to allow a broad group of participants without getting into all the complications of having a large number of employees be partners... which could cause a lot of complications for the lower level employees."

However, there are trade-offs. Payouts from phantom equity are taxed as ordinary income, with federal rates reaching up to 37%. By contrast, employees with certain stock options may qualify for lower long-term capital gains rates (0–20%) if they hold their shares long enough. Some companies try to offset this higher tax burden by grossing up payouts by about 17%, but this increases the company’s cash obligations. Moreover, unlike share-based awards, phantom equity payouts require cash, which can create liquidity challenges - especially for startups.

Here’s a quick comparison of phantom equity and stock options/RSUs:

| Factor | Phantom Equity | Stock Options / RSUs |

|---|---|---|

| Ownership Dilution | None | Dilutes existing shareholders |

| Employee Tax Rate | 22%–37% (ordinary income) | 0%–20% (long-term capital gains, if held) |

| Company Tax Deduction | Yes - full payout deductible | Only for NSOs; not for ISOs |

| Cash Flow Impact | High - requires cash at payout | Low - settled in shares |

| Administrative Complexity | Moderate - no cap table changes | High - legal filings and shareholder governance |

| Employee Cost to Acquire | $0 | Must pay strike price (options) |

| Accounting Treatment | Liability; mark-to-market each period | Equity-settled; fixed at grant date |

Another challenge with phantom equity is earnings volatility. Since it’s treated as a liability, its value must be re-evaluated regularly. If the company’s valuation spikes, the expense tied to phantom equity rises too, potentially causing swings in earnings that complicate financial reporting. In contrast, traditional equity awards are fixed at the grant date, offering more predictability.

Aaron D. Werner, an attorney at Horwood Marcus & Berk Chartered, captures the essence of phantom equity well:

"Granting phantom equity is somewhat akin to dating before getting married – there are clear benefits to both the employee and employer... but if it does not work out, both sides can walk away with minimal, if any, strings attached."

This flexibility, along with the ability to forfeit units if an employee leaves, makes phantom equity an appealing option for rewarding key talent without permanently altering the company’s ownership structure.

Conclusion

Phantom equity is a focused solution designed for specific types of businesses. It’s particularly well-suited for LLCs, S-corporations, family-owned companies, closely held businesses, and firms working with international contractors who encounter obstacles with traditional U.S. equity structures. Additionally, it’s a practical choice for late-stage companies nearing an IPO or acquisition - typically within 12–24 months - where setting up a formal stock option plan might be too time-consuming or complicated.

On the flip side, phantom equity isn’t ideal for every situation. Startups that are pre-revenue, operating with tight cash reserves, or backed by venture capital may find it more of a hindrance than a help. As Angel Investors Network explains: "A pre-revenue company burning $100K monthly can't afford $2 million in phantom stock payouts at exit." Venture capitalists often view phantom equity obligations as a potential cash drain, which can lower the company’s overall valuation during fundraising rounds.

The decision largely depends on three critical factors: your entity structure, cash flow stability, and cap table priorities. For instance, C-corporations with venture backing and a clear path to an IPO are usually better off sticking with traditional stock options or RSUs. On the other hand, LLCs and closely held businesses aiming to reward key contributors without diluting ownership or losing control may find phantom equity an appealing alternative.

One key takeaway? Early modeling of phantom equity payouts is crucial. Without careful planning, large phantom obligations can quietly eat into founder proceeds at the time of exit. Tools like Lucid Financials can provide real-time financial insights and CFO-level guidance, helping you stay ahead of these liabilities and avoid unwelcome surprises during liquidity events.

To make phantom equity work effectively, define payout triggers clearly, ensure full Section 409A compliance to avoid hefty IRS penalties, and be transparent about phantom liabilities in discussions with potential investors. With proper planning and execution, phantom equity can serve as a powerful tool for retaining top talent. But if handled poorly, it risks becoming a costly burden at the worst possible moment.

FAQs

How do I estimate the cash needed for phantom equity payouts at exit?

To figure out how much cash you'll need for phantom equity payouts, start by defining your plan's structure - whether it’s based on full value or appreciation-only. This decision sets the foundation for everything else.

Next, forecast your company’s future value. This helps you create a budget for value-sharing and ensures you're prepared for upcoming obligations. It’s also essential to model potential payouts against liquidity events, like acquisitions or IPOs. Don’t forget to account for scenarios where there’s no immediate cash inflow, such as stock-for-stock transactions.

If managing these complexities feels overwhelming, services like Lucid Financials can help. They specialize in supporting startups with CFO-level expertise, helping you handle liabilities, track valuations, and keep your financial records investor-ready as your business scales.

What phantom equity plan terms can accidentally violate IRS 409A rules?

Phantom equity plans require a formal, written agreement to align with IRS Section 409A regulations. Skipping this step - like relying on verbal agreements - can trigger immediate taxation and an additional 20% penalty. To stay compliant, payouts must be tied to one of six specific events, such as separation from service, death, or a fixed date. Additionally, these plans must follow anti-acceleration rules, meaning payment schedules cannot be changed once they’re established.

When is phantom equity a better fit than stock options or RSUs?

Phantom equity is a great option for rewarding employees without granting actual ownership. This approach sidesteps common challenges like dilution, governance complications, and administrative hurdles. It's especially beneficial for LLCs, S-corporations, or businesses gearing up for a sale, as it helps avoid tax-timing issues, such as AMT exposure, while preserving control. Additionally, it’s an effective solution in regions where issuing equity is difficult or for companies that need to stay within shareholder limits.