Phantom equity allows employees to earn cash bonuses tied to company stock value without owning actual shares. It's popular among startups and LLCs because it avoids ownership dilution and simplifies tax reporting. However, understanding taxation and compliance with Section 409A is critical to prevent costly penalties.

Key Points:

- What it is: A cash bonus linked to stock value, with no ownership transfer.

- Why companies use it: Retains employees, avoids ownership dilution, and simplifies administration.

- Taxation:

- Section 409A compliance: Ensures deferred compensation rules are followed to avoid penalties.

- Comparison: Phantom equity differs from profits interest units (PIUs) and stock appreciation rights (SARs) in terms of taxation, ownership, and payout structure.

Phantom equity is a flexible way to reward employees, but it requires careful tax planning and compliance to maximize benefits and minimize risks.

Phantom Equity: Its Advantages and Disadvantages for Incentivizing Employees

sbb-itb-17e8ec9

How Phantom Equity Is Taxed

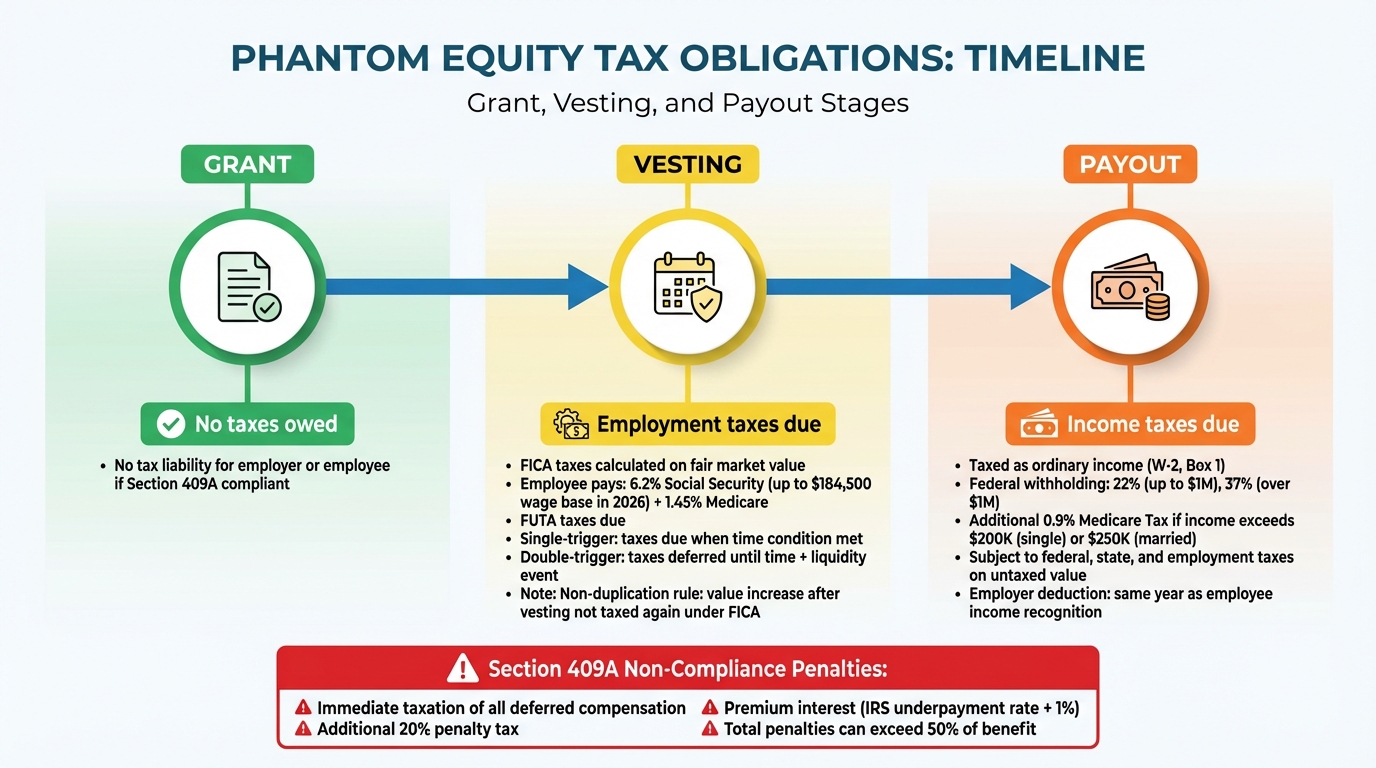

Phantom Equity Tax Timeline: Grant to Payout

When it comes to phantom equity, timing plays a big role in determining tax obligations. Here's how it works: income taxes are postponed until the payout is received, but employment taxes - like FICA (Social Security and Medicare) and FUTA - become due when the phantom shares vest. Vesting happens when the compensation is no longer at risk of being forfeited.

Tax Treatment at Grant and Vesting

If the plan complies with Section 409A, no taxes are owed when phantom equity is granted. Instead, income tax is delayed until the cash payout occurs.

However, FICA and FUTA taxes are calculated at the time of vesting based on the fair market value of the phantom shares. For single-trigger plans, where vesting depends solely on meeting a time-based condition, these taxes are due once that condition is fulfilled. For double-trigger plans, which require both a time-based condition and a liquidity event (like a sale or IPO), employment taxes are deferred until both conditions are met.

Employers are responsible for calculating and paying FICA taxes on the current fair market value of the vested shares. Employees, on the other hand, must pay their portion of FICA taxes - 6.2% for Social Security (up to a wage base of $184,500 in 2026) and 1.45% for Medicare. This can be done either out-of-pocket or through wage withholding. Once FICA taxes are paid on the vested value, the non-duplication rule ensures that any increase in value between vesting and payout is not taxed again under FICA.

Tax Treatment at Payout

While employment taxes are triggered at vesting, income tax remains deferred until the payout is received. At that point, the entire amount is taxed as ordinary income, not as a capital gain. This income is reported on Form W-2 in Box 1 and is subject to federal, state, and employment taxes on any untaxed value.

Here’s a quick breakdown of the tax classifications and timing:

| Tax Type | Timing of Taxation | Classification |

|---|---|---|

| Federal/State Income Tax | At Payout (when cash is received) | Ordinary Income (W-2) |

| FICA/FUTA Tax | At Vesting (when risk of forfeiture ends) | Ordinary Income (W-2) |

| Employer Deduction | At Payout (when income is recognized) | Compensation Expense |

Payouts are generally treated as supplemental wages. For amounts up to $1 million, a flat 22% federal withholding rate applies. For amounts over $1 million, the rate increases to 37%. Additionally, employees with total wages exceeding $200,000 (for single filers) or $250,000 (for married filing jointly) are subject to an extra 0.9% Medicare Tax. Employers can deduct the payout as a wage expense in the same year the employee recognizes the income.

If a phantom stock plan fails to meet Section 409A requirements, employees could face harsh penalties. These include an additional 20% penalty tax on all deferred compensation, plus interest calculated at the IRS underpayment rate plus 1%. In some cases, total penalties could exceed 50% of the benefit.

Section 409A Compliance Requirements

Understanding the tax rules tied to Section 409A is essential, especially when dealing with nonqualified deferred compensation like phantom stock. Since phantom stock represents a promise of future compensation for current services, it falls squarely under Section 409A. Failing to comply can result in immediate taxation and steep financial penalties.

"The architecture of 409A puts the employee in an uncomfortable position: you bear almost all of the penalty risk for failures that are often caused by the employer's plan design or administrative mistakes." – LegalClarity Team

The stakes are high because Section 409A violations don't just affect the company - they hit employees directly. This makes proper plan design and ongoing compliance a shared priority for both employers and employees.

Valuation and Documentation

A reliable fair market value (FMV) is the cornerstone of compliance. Using a safe harbor valuation from a qualified independent appraiser (like an ASA or ABV) is highly recommended. This shifts the burden of proof to the IRS, meaning the IRS must demonstrate that the valuation is grossly unreasonable, rather than the company needing to prove its accuracy.

Typically, a 409A valuation remains valid for 12 months unless a material event occurs. Material events include major financial shifts like a priced funding round, significant SAFE or convertible note raises, secondary market transactions, or other substantial changes. If such an event happens, a new valuation must be conducted immediately, even if the 12-month window hasn’t expired.

Compliance also requires a formal, written agreement for the phantom equity plan. Verbal agreements are automatically non-compliant. The written document must clearly define key terms like "separation from service" or "change in control" and restrict payouts to six specific events: separation from service, death, disability, change in control, unforeseeable emergency, or a fixed date. Additionally, once a payment schedule is locked in, the anti-acceleration rule prohibits advancing payments, even if both parties agree to an earlier disbursement. Deviating from these rules invites serious consequences.

Penalties for Non-Compliance

Violating Section 409A triggers severe financial repercussions. All deferred compensation becomes taxable in the year of the violation, regardless of whether the employee actually received the funds. On top of regular income tax, the employee faces an extra 20% federal tax on the affected amount, plus premium interest calculated at the underpayment rate plus 1%, starting from the deferral date.

One notable example involves Sehat Sutardja, the former CEO of Marvell Technology. In January 2004, Sutardja received stock options priced in December 2003 but not formally approved until January. Because the stock price had risen in the interim, the IRS ruled that the options were granted below FMV, violating Section 409A. Despite challenging the decision, Sutardja lost the case and faced penalties exceeding $5 million.

Some states, like California, add even more penalties - up to an additional 20% state tax on top of federal consequences.

If a violation is identified, immediate corrective action is critical. The IRS provides correction programs (outlined in Notices 2008-113 and 2010-6) that can help reduce or avoid full penalties if the issues - whether operational or documentation-related - are addressed promptly.

Phantom Equity vs. Other Compensation Tools

Building on the tax and operational details discussed earlier, comparing phantom equity with other compensation tools helps clarify when it might be the right choice. Alongside phantom equity, options like profits interest units (PIUs) and stock appreciation rights (SARs) each come with their own advantages and challenges.

Phantom Equity vs. Profits Interest Units

Profits Interest Units (PIUs) represent actual ownership in an LLC, while phantom equity is essentially a cash bonus tied to the company’s performance. One of the biggest draws of PIUs is their tax treatment. When structured correctly, recipients of PIUs can benefit from long-term capital gains taxation on future growth, instead of being taxed at higher ordinary income rates. For instance, in a $500,000 payout scenario, a PIU recipient might take home around $375,000 after taxes, while someone with phantom equity might end up with approximately $325,000. This difference comes down to how each is taxed.

However, PIUs come with added complexity. Recipients become legal partners for tax purposes, which means they lose their W-2 employee status. Instead, they receive K-1 forms and take on self-employment tax responsibilities. Mark Heroux, J.D., Principal at Baker Tilly Virchow Krause LLP, explains:

"The recipient of a profit interest grant... will not be eligible to be a W-2 employee from the date of grant. This removes their regular compensation from the wage pool in Sec. 199A calculations."

There are also structural limitations. PIUs can only be issued by LLCs or partnerships - corporations cannot use them. Additionally, while phantom equity payouts are tax-deductible for the company as a compensation expense, PIU distributions are considered profit sharing and are not deductible.

To address the tax disparity between phantom equity and PIUs, many startups use a "gross-up" strategy. For example, to match the $375,000 after-tax benefit of a PIU, a company might gross up the phantom equity payment to around $576,923, assuming a 35% ordinary tax rate.

PIUs are best suited for scenarios where genuine ownership transfer is a priority or when recipients specifically want capital gains treatment. On the other hand, phantom equity works well for retaining employees without the administrative burdens of partnership tax reporting. Choosing between these tools depends on aligning compensation strategies with the company’s tax and operational goals.

Phantom Equity vs. Stock Appreciation Rights (SARs)

Stock Appreciation Rights (SARs) only pay out the increase in stock value above a set strike price, while phantom equity can be structured to include either the full value or just the appreciation bonus. SARs offer recipients the flexibility to decide when to exercise their rights after vesting, whereas phantom equity payouts are typically tied to specific company milestones or trigger events, such as a sale or change in control.

Phantom equity has the added advantage of flexibility - it can mimic real equity more closely by including features like dividend equivalents or even voting rights. These are generally not part of SARs. Sarah Khuwaja from Product Resources highlights this distinction:

"Phantom stock can create a sense of ownership and tie to specific company milestones. SARs are a more narrow reward that never include complexities of dividends or total underlying value considerations".

Both SARs and phantom equity must meet Section 409A compliance requirements. A key difference is that SARs can sometimes be settled in actual shares, potentially qualifying for capital gains treatment in the future. Phantom equity, however, is almost always settled in cash. SARs are particularly useful for rewarding growth, while phantom equity offers a broader simulation of ownership without the need to issue actual shares.

These differences underline the importance of understanding each tool’s structure to simplify tax planning and align employee incentives with company goals.

Financial Planning for Phantom Equity Recipients

Payout Timing and Liquidity

Understanding when and how you’ll receive payouts from your phantom equity is a key part of financial planning. Unlike traditional stock options, where you can choose when to exercise, phantom equity payouts are tied to specific events outlined in your agreement. Common triggers include company sales, retirement, disability, death, or a pre-set date. These terms are locked in at the time of the grant under Section 409A.

When it comes to receiving your payout, you may have the option of a lump sum or installment payments. Each choice comes with its own financial implications. A lump sum provides immediate access to cash, but it can push you into the highest federal tax bracket (up to 37%) and may also trigger the 0.9% Additional Medicare Tax if your income exceeds $200,000 (single filers) or $250,000 (married filing jointly). On the other hand, installments spread the income over multiple years, potentially keeping you in lower tax brackets, though it delays full access to your funds.

It’s equally important to review your agreement to confirm your status as a "good leaver" in cases like retirement or disability. This designation can protect unvested units during major life changes. However, keep in mind that as a phantom equity holder, you’re considered an unsecured creditor. If the company goes bankrupt before your payout, you could lose the entire benefit.

These factors make it clear that liquidity considerations go hand-in-hand with proactive tax planning.

Tax Planning Strategies

Phantom equity’s tax rules require careful planning. Employment taxes, such as FICA, are due when the equity vests, but federal and state income taxes aren’t triggered until you receive the actual payout. This timing mismatch can create a "phantom" tax liability, where you owe taxes before receiving any cash. It’s crucial to coordinate with your employer to understand how FICA withholding will be handled - whether it’s deducted from your regular wages, paid separately, or offset against your unit balance.

If you anticipate a payout in the near future, work with a tax professional to reduce other taxable income during that year. Since phantom equity payouts are taxed as ordinary income (reported on your W-2) rather than capital gains, a large payout could significantly increase your overall tax burden. Make sure your employer’s withholding rate matches your actual tax bracket to avoid underpayment penalties when filing your return.

Lastly, confirm that your phantom equity plan complies with Section 409A. Non-compliance can lead to immediate taxation of all deferred amounts, plus a 20% penalty tax and premium interest. For executives identified as "specified employees", there may also be a mandatory six-month delay on payouts following separation from service. Incorporating phantom equity into your annual tax planning can help you navigate these challenges effectively.

For startups or individuals seeking expert guidance, consider consulting Lucid Financials (https://lucid.now) for tailored advice on managing these complexities.

This approach to tax planning aligns with the broader financial considerations for phantom equity recipients.

Conclusion and Key Takeaways

Summary of Tax Obligations

Here’s a quick breakdown of the tax responsibilities tied to phantom equity plans:

- At grant: No tax liability arises for either party.

- At vesting: Employment taxes, such as FICA and FUTA, are due based on the fair market value at the time. This can catch some off guard since there’s no cash payout yet.

- At payout: The entire distribution is taxed as ordinary income, with rates reaching up to 37%. This amount will appear on your W-2.

An important note: FICA taxes paid at vesting only apply to the vested value at that time. Thanks to the non-duplication rule, any increase in value afterward isn’t subject to additional FICA tax when the payout happens. For startups, the tax deduction can only be claimed in the year employees recognize the income, which typically aligns with the distribution.

Failing to comply with Section 409A can lead to immediate taxation of all deferred amounts, even if they haven’t vested yet. On top of that, penalties can exceed 50% of the benefit.

Working with Financial Professionals

Given the complexities of tax timelines and penalties, professional advice is crucial. Startups should secure independent 409A valuations annually to establish defensible fair market values and avoid potential IRS scrutiny. It’s essential to formalize the plan in writing, clearly defining payment triggers like "change in control" or "separation from service." Verbal agreements won’t cut it and could lead to penalties.

For recipients, consulting a tax advisor is key. They can help manage FICA withholding at vesting and prepare for significant payouts. Additionally, reviewing "good leaver" provisions and understanding your rights as an unsecured creditor can provide added protection during pivotal life events.

Lucid Financials (https://lucid.now) is an excellent resource for startups and founders navigating phantom equity plans. They combine AI-powered bookkeeping with expert tax guidance to help ensure compliance with Section 409A and optimize tax strategies for equity compensation. With real-time support via Slack and straightforward pricing starting at $150/month, Lucid simplifies the process while delivering valuable expertise.

FAQs

How do I pay FICA taxes at vesting if I don’t get cash yet?

When phantom equity vests, FICA taxes become due, even if no cash changes hands at that moment. The IRS considers the value of the phantom stock at vesting as taxable income. While employers usually withhold FICA taxes from the eventual cash payout, if no cash is received at vesting, these taxes are typically settled when the payout is finally made.

What triggers a phantom equity payout under 409A rules?

When it comes to phantom equity payouts under 409A rules, the payout is activated by specific events or milestones. These triggers often include hitting a set date or achieving certain performance benchmarks. Once these conditions are met, the employee becomes eligible for a cash payment that’s linked to the value of the company’s stock.

How can I tell if my phantom equity plan is 409A-compliant?

To ensure your phantom equity plan aligns with 409A compliance, it must meet the IRS rules for non-qualified deferred compensation. This involves several key elements: designing the plan correctly, obtaining accurate valuations, and ensuring payment timing complies with the regulations. Typically, this process requires independent valuations and strict adherence to IRS standards to confirm everything is in order.