Fraud costs businesses billions each year, and startups are especially vulnerable. Real-time fraud detection can stop suspicious activity in milliseconds, protecting your finances and saving hours of manual reviews. Unlike older systems that analyze transactions in batches, real-time detection works during authorization, blocking fraud before funds are moved.

Key Takeaways:

- Why it matters: U.S. businesses lost $8.8B to fraud in 2022, a 30% increase from 2021. Startups can't afford these risks.

- How it works: Combines machine learning, behavioral analytics, and stream processing to evaluate transactions instantly.

- Benefits: Cuts fraud losses, reduces manual reviews to 0.1%-0.5% of transactions, and boosts compliance with regulations.

- Technologies used: Tools like Apache Kafka, machine learning models, and device fingerprinting power these systems.

- Case Study: Ramp reduced account takeover attacks by 60% with real-time fraud detection.

If you're a startup, implementing a fraud detection system can take as little as 2-8 weeks. Focus on features like real-time monitoring, device tracking, and latency under 100ms. With the right tools, you can secure your financial operations and scale confidently.

Build Realtime Fraud Detection AI from Scratch - End to End Machine Learning Project - Part 1

sbb-itb-17e8ec9

What Is Real-Time Fraud Detection?

How Real-Time Fraud Detection Works: 3-Step Process

Real-time fraud detection evaluates transactions as they happen, delivering a risk decision in milliseconds to seconds - an essential feature during critical phases like bank data synchronization. Unlike traditional fraud prevention methods, which analyze transactions in batches after they've occurred, real-time systems act during the authorization phase, stopping fraudulent transactions before funds are moved.

The technological difference is stark. Traditional systems depend on historical data stored in analytic warehouses, while real-time detection operates with stream-processing engines that analyze data as it flows in. This capability, with response times under 100 milliseconds, allows these systems to intercept threats during authorization, effectively preventing fraud at its source.

For startups, the advantages are clear. Real-time detection not only prevents financial losses from unauthorized transactions but also reduces the need for extensive manual reviews, focusing only on the riskiest cases. It fosters user trust by sending instant alerts that encourage quick action. Advanced algorithms can spot intricate patterns - like coordinated attacks or unusual behaviors - that might escape human investigators. A PwC report found that nearly 50% of organizations encountered fraud within two years. With limited resources, startups can automate detection, reducing manual reviews to just 0.1% to 0.5% of transactions. This capability is particularly valuable in addressing the specific fraud risks startups face.

Common Fraud Challenges Startups Face

Startups face various fraud types that can threaten their financial stability. Account Takeover (ATO) happens when fraudsters gain control of user accounts. Real-time detection counters this by identifying unusual login or spending behaviors within seconds. Card testing, another common threat, involves small transactions to validate stolen card details before larger purchases are made. Synthetic identity fraud, where real and fake identity elements are combined to create new accounts, poses a significant challenge for traditional detection methods.

Between 2019 and 2022, suspected digital fraud attempts in financial services surged by 39%. In 2022, the Central Bank of Nigeria reported losses of ₦5.45 billion due to attempted fraud, with a 45% rise in financial fraud highlighted in its 2024 stability report. For startups, even one successful attack can disrupt cash flow or undermine investor confidence. Real-time systems also help startups stay compliant with regulations like PCI DSS 4.0, GDPR, and Strong Customer Authentication (SCA). By spotting suspicious activity that must be reported or blocked under these rules, these systems mitigate compliance risks while protecting financial operations. These challenges emphasize why instant fraud detection is critical, especially during bank data synchronization.

How Real-Time Detection Works

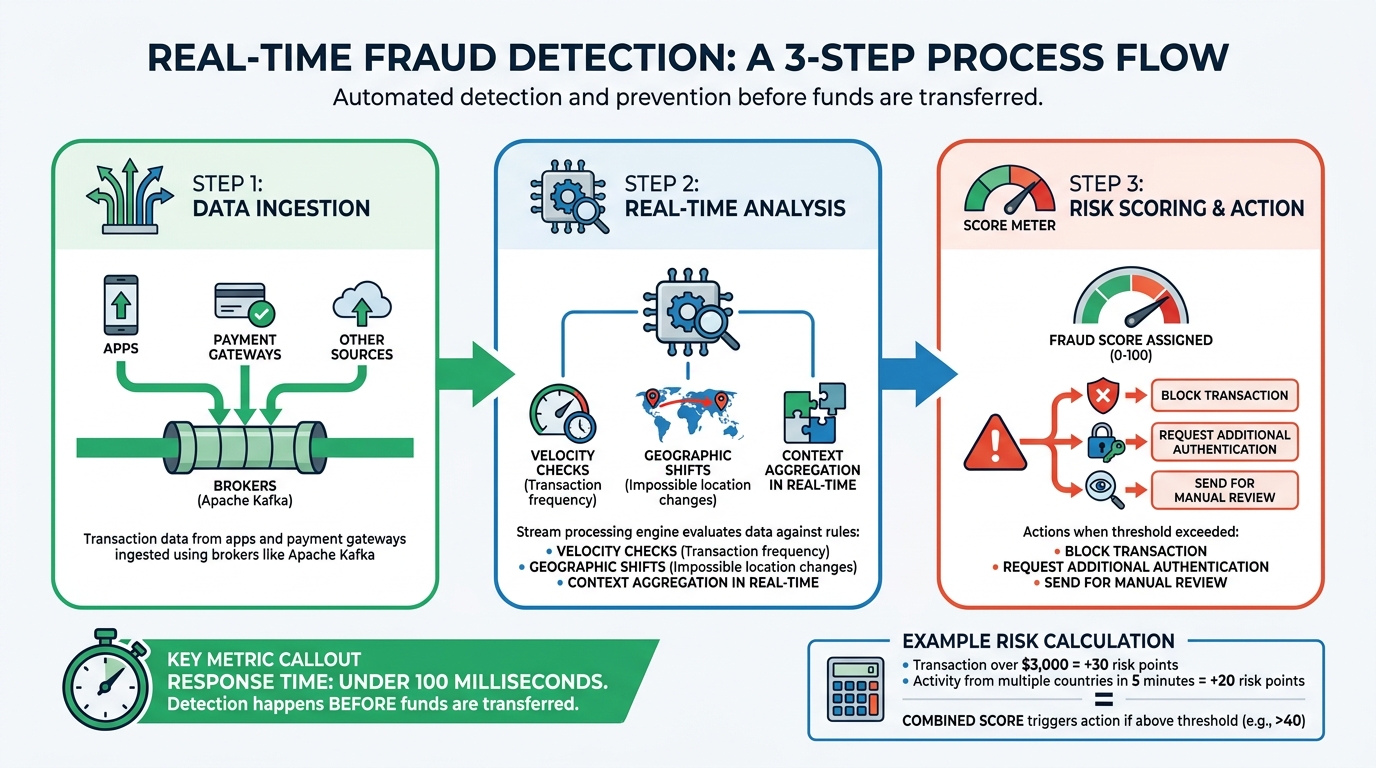

Here’s a closer look at how real-time fraud detection operates. The process involves three key steps. First, transaction data from apps and payment gateways is ingested using brokers like Apache Kafka. Next, a stream processing engine evaluates this data against predefined rules - such as velocity checks (monitoring transaction frequency) and geographic shifts (detecting impossible location changes) - while aggregating context in real time. Finally, the system assigns a fraud score (ranging from 0 to 100), with scores above a set threshold triggering actions like blocking the transaction or requesting additional authentication.

A great example of this in action is Ramp, a financial technology company. Before switching to real-time detection, Ramp relied on batch processing, taking over an hour to detect Account Takeover attacks. By adopting Materialize for real-time detection, the company reduced detection times to just 1–3 seconds. This change led to a 60% drop in successful ATO attacks, with half of the compromised accounts flagged without incurring extra costs.

Real-time systems combine multiple signals to build a detailed risk profile. For instance, a transaction over $3,000 might add 30 risk points, while activity from multiple countries within five minutes could add another 20 points due to the impossibility of card-present transactions in such scenarios. If the combined score exceeds the threshold, the system can block the transaction, prompt additional authentication, or send it for manual review - all before any funds are transferred.

Technologies That Power Real-Time Fraud Detection

Real-time fraud detection combines machine learning, behavioral analytics, and streaming architectures to evaluate transactions in milliseconds. These technologies transform raw data into actionable risk scores, playing a critical role in detecting fraud as transactions are processed.

Machine Learning and AI

Machine learning models can analyze hundreds of variables in under 50 milliseconds to assign fraud probability scores. Unlike static, rule-based systems, these models adjust to new fraud patterns. For example, supervised learning models - trained on historical data - spot known fraud types, while unsupervised learning identifies anomalies that could indicate new or unexpected fraud attempts.

A two-step inference approach helps balance speed and accuracy. A quick filter, such as LightGBM, processes data in around 5 milliseconds, while more complex neural networks handle ambiguous cases. Tools like Graph Neural Networks (GNNs) map connections between accounts, devices, and IP addresses to uncover coordinated fraud schemes.

Machine learning can lower false positive rates by 40% to 60% compared to traditional systems. This is crucial because each legitimate transaction wrongly flagged as fraud costs businesses an estimated $118 in lost revenue and operational expenses.

"Accuracy alone is not enough. Latency, false positives, auditability, and cost all matter just as much." – Raghav Sharma, Data Scientist

While AI excels at crunching numbers, behavioral analytics adds another layer by providing context to these risk evaluations.

Behavioral Analytics and Device Fingerprinting

Behavioral analytics creates a baseline for normal user behavior by tracking patterns like typing speed, session length, and navigation habits. When activity deviates from this baseline - such as unusual transaction amounts or access from unexpected locations - the system flags the behavior for review.

Device fingerprinting enhances this process by identifying users through features like browser type, screen resolution, and hardware identifiers. This method can recognize users even in incognito mode or when they attempt to remain anonymous. It also detects risky setups, such as VPNs or proxy servers, often used by fraudsters.

Velocity tracking monitors the frequency of transactions and device activity, helping to identify patterns like card testing or bot-driven fraud. These combined signals build a complete risk profile. For instance, a single device linked to multiple accounts or a credit card used across different regions could indicate fraudulent behavior. Without biometric verification, organizations risk significant losses from synthetic identity fraud, with average losses reaching $10,000 to $15,000 per account before detection. Behavioral analytics is particularly effective in spotting synthetic fraud, which often lacks a natural digital footprint and shows sudden "bust-out" behavior.

By combining advanced modeling with user behavior analysis, real-time scoring systems turn these data points into actionable decisions.

Real-Time Scoring and Data Analysis

Real-time scoring systems evaluate transaction data - like geolocation, IP address, and transaction history - to produce fraud probability scores. Using tools such as Redis or DynamoDB for feature storage and Apache Kafka or Flink for streaming, these systems continuously process and analyze data, even during high-traffic periods.

Based on these scores, transactions are categorized: low-risk ones may be approved automatically, medium-risk cases might require additional verification, and high-risk transactions can be blocked. This fast scoring process ensures that threats are intercepted before any funds are transferred.

Explainable AI (XAI) tools, like SHAP, provide clear reasons for why a transaction was flagged. These tools highlight factors such as unusual amounts or high-risk IP addresses, meeting regulatory standards for transparency and clarity.

How to Implement Fraud Detection in Your Startup

Getting a fraud detection system up and running doesn’t have to be a long, drawn-out process. By focusing on the essentials and scaling as your transaction volume grows, most startups can launch a functional system in just two to eight weeks. Below, we’ll break down the key features, integration steps, and cost strategies to help you build an effective fraud detection setup.

Key Features to Prioritize

Start by identifying the fraud risks specific to your business. Common threats for startups include card-not-present fraud, account takeovers, card testing, and promo abuse. To tackle these challenges, prioritize the following features:

- Real-time monitoring: Your system should process transaction events as they happen, whether they come from payment gateways, bank feeds, or streaming platforms like Kafka. Use velocity signals to flag unusual activity, such as a card being used multiple times in quick succession. Add geographic anomaly detection to catch scenarios like “impossible travel,” where a card is used in two far-apart locations within minutes.

- Device fingerprinting and behavioral signals: Track key metrics like new devices tied to high-value transactions, the number of accounts linked to a single device, and spending patterns that deviate sharply from a user’s typical behavior. Combine these signals into a composite risk score (e.g., 0 to 100) to decide whether to allow, challenge, or block a transaction.

"The fraud happens in minutes. The detection happens in hours." – Fahad Shah, RisingWave

- Latency targets: Speed matters. For card-present transactions, aim for decisions in under 100 milliseconds. For e-commerce, keep it under 250 milliseconds to avoid losing conversions - checkout rates drop by roughly 1.5% for every 100 milliseconds beyond a 300-millisecond response time. Use a two-tier scoring system: an inline model for instant decisions (under 10 milliseconds) and a nearline tier for deeper analysis within one to five seconds.

Integration with Bank Data Synchronization

Fraud detection thrives on real-time data. Move away from batch updates - fraudulent cards can be drained in 20 to 30 minutes after their first use. Instead, adopt streaming data processing. Tools like Debezium’s Change Data Capture (CDC) can sync your operational databases with your fraud detection system without overloading your infrastructure.

To keep latency low, use incremental materialized views in an operational data warehouse. This approach enables sub-second query speeds while keeping costs manageable. For example, Ramp, a corporate card startup, switched to real-time streaming with Materialize in 2024. This reduced their detection latency from over an hour to just one to three seconds, cutting account takeover attacks by 60%.

Ensure your fraud engine has access to clean financial data by linking your accounting software (e.g., QuickBooks or Xero) directly to bank feeds and payment processors like Stripe. Automate alerts for high-risk transactions, sending them to Kafka topics or operational databases to trigger immediate actions like blocking transactions or notifying users via SMS.

Balancing Speed, Accuracy, and Cost

For startups with gross merchandise volume (GMV) under $500 million, a cloud-based fraud detection solution offers a quick and affordable way to get started. These systems typically charge a small percentage of GMV or a per-transaction fee and can be implemented in as little as two to eight weeks. As your GMV grows or your fraud patterns become more complex, you may want to transition to an in-house platform for greater control and transparency.

To manage costs while maintaining performance, use a tiered scoring approach:

- Simple rules for immediate blocking (under five milliseconds).

- Lightweight models like LightGBM for broader analysis (15 to 40 milliseconds).

- Advanced models, such as Graph Neural Networks, for ambiguous cases. This setup can cut machine learning inference costs by 60% to 80%.

Focus on feature engineering rather than obsessing over model complexity. High-quality features like transaction velocity, device fingerprints, and historical aggregates often improve accuracy more than upgrading to complex neural networks. Weekly model retraining can capture evolving fraud patterns and boost accuracy (AUC) by 8% to 12%. Keep an eye on concept drift by tracking feature distributions and retrain models when the Population Stability Index exceeds 0.2.

Lastly, keep decision thresholds flexible so your fraud operations team can adjust them on the fly without redeploying code. Use champion/challenger testing by routing 5% to 10% of traffic to a new model to validate its effectiveness before a full rollout. These strategies help you maintain real-time fraud protection while optimizing costs and keeping your financial workflows secure.

How Lucid Financials Supports Fraud-Resistant Financial Management

Lucid Financials goes beyond just tracking transactions - it merges real-time fraud detection with advanced accounting tools to safeguard your startup's financial operations.

By combining AI-powered accounting with real-time fraud monitoring, Lucid Financials ensures your financial records stay accurate while identifying suspicious activity immediately. It seamlessly connects to your bank accounts, payment platforms, and accounting software, analyzing data to catch anomalies the moment they occur.

The platform also integrates with Slack for quick incident response. As Slack explains:

"Slack helps the right experts - whether internal or external - come together quickly in Slack channels, where they can [...] improve time to resolution for critical fraud incidents."

This feature is especially valuable for startups without dedicated fraud teams, as it simplifies collaboration and speeds up investigations, ensuring faster resolutions when fraud is detected.

Lucid Financials' fraud detection capabilities have proven results. For example, in 2025, a leading global bank adopted Lucid's AI-driven system to monitor transaction patterns in real time. The results? An 85% boost in fraud detection speed and a 62% drop in fraudulent transactions, saving the bank $10 million annually. The bank's Chief Risk Officer highlighted the impact:

"Lucid Technologies AI-driven solutions improved our fraud detection accuracy and helped us cut financial losses significantly".

But Lucid Financials doesn't stop at fraud detection. It strengthens your financial workflows with top-notch security. The platform integrates with over 2,200 apps through Slack, consolidating alerts from its AI system into one place. This eliminates the need to juggle multiple tools, keeping fraud discussions secure and compliant with regulations like FINRA and GDPR. For external collaboration, Slack Connect ensures seamless yet secure communication with partners when necessary.

For startups building their own fraud detection systems, Lucid Financials offers a strong foundation. It leverages synchronized bank data to provide clean, real-time analytics for fraud models, investor-ready reports that document fraud-related losses, and CFO-level insights to balance prevention costs with business growth. Whether your startup handles $50,000 or $50 million in monthly transactions, Lucid Financials scales with your needs, adapting to the complexities of modern financial management.

Conclusion

Real-time fraud detection has become a must-have for startups managing financial transactions. The numbers are alarming: U.S. businesses lost $8.8 billion to fraud in 2022, while consumer losses exceeded $10 billion by 2023. These figures highlight the vulnerabilities of traditional batch processing, where fraudsters can exploit gaps of just 20 to 30 minutes to empty accounts before systems even react.

Thankfully, implementing modern fraud detection tools is now simpler than ever. Startups can leverage SQL-based stream processing without diving into complex coding. By combining multiple data signals into a single risk score, fraudulent activity can be identified and stopped almost instantly. For example, Ramp demonstrated how real-time detection - cutting response times to just 1–3 seconds - led to a 60% drop in fraud attacks. These advancements make it easier to integrate fraud prevention directly into financial workflows.

The best solutions are those that fit smoothly into existing operations. They should connect directly to bank data, payment systems, and operational tools without requiring a complete infrastructure overhaul. Scalability is also crucial - your system needs to grow with your transaction volume and adapt to evolving fraud tactics without frequent updates or redeployment.

For startups aiming to build fraud-resistant systems, success lies in combining cutting-edge technology with practical integration. Look for tools that offer sub-second detection, support standard SQL for quick implementation, and automate actions like blocking cards or flagging cases for review. The goal is clear: prevent fraud before it can settle, ensuring both operational efficiency and peace of mind.

FAQs

What data do I need to start real-time fraud detection?

To set up real-time fraud detection, you’ll need access to transaction data, including details like the amount, timestamp, location, device fingerprint, and merchant category. Additionally, behavioral signals play a critical role - things like transaction velocity, user activity patterns, and unexpected anomalies in devices or locations can help flag suspicious behavior.

This data is typically collected through transaction streams and processed in real time. By applying rules or leveraging machine learning models, you can quickly identify and respond to potential fraudulent activity.

How can I keep fraud decisions under 100 ms?

To keep fraud decisions lightning-fast - under 100 milliseconds - focus on optimizing your system for speed. Here’s how:

- Leverage high-throughput streaming tools: These handle large volumes of data efficiently, ensuring smooth and rapid processing.

- Use lightweight detection algorithms: Simplified algorithms cut down on processing time without sacrificing accuracy.

- Rely on in-memory databases: Storing data in memory (rather than on disk) allows for near-instant access and analysis.

- Pre-aggregate datasets: This makes querying faster since the data is already summarized or structured for quick retrieval.

- Deploy logic near data sources: Reducing the distance between where data is generated and where it’s processed helps minimize latency.

Finally, make it a habit to regularly monitor and fine-tune your pipeline. This ensures your system consistently delivers real-time fraud detection with ultra-low latency.

How should I set fraud score thresholds without blocking real customers?

To determine fraud score thresholds effectively, start by analyzing historical transaction data. This helps you understand normal customer behavior patterns, which can guide you in setting thresholds that make sense. Begin with a conservative approach and adjust gradually based on how often legitimate transactions are mistakenly flagged (false positives).

You should also establish velocity rules - for example, setting limits on the number of transactions allowed per hour. Regularly review flagged transactions to ensure your thresholds are working as intended. Adjust these rules as needed to strike the right balance between catching fraud and maintaining a seamless experience for your customers.