If your VC fund has foreign investors, offshore entities, or non-U.S. portfolio companies, tax reporting gets harder fast. I’d focus on five things first: investor tax forms, withholding rates, partnership filings, non-U.S. reporting, and a calendar that ties everything together.

Here’s the short version:

- Missing W-8 forms can trigger 30% withholding on some U.S.-source payments.

- Forms 1042 and 1042-S are due March 15, and Form 8966 is due March 31.

- Foreign LPs may trigger ECI withholding at 37% for individuals and 21% for corporations.

- Section 1446(f) can require 10% withholding when a foreign LP sells a fund interest.

- CRS, AIFMD, and DAC6 can apply even when the main fund is U.S.-based.

In plain English, I’d treat cross-border tax reporting as a data problem before I treat it as a filing problem. If investor records, entity records, and income records do not match, the cleanup usually costs more time than the filing itself.

A quick way to think about it:

| Area | What I’d watch |

|---|---|

| Investor onboarding | W-9s, W-8s, CRS self-certifications, expiry dates |

| U.S. withholding | 30% default withholding, treaty claims, 1042/1042-S |

| Partnership tax | Form 1065, K-1s, K-2, K-3, ECI allocations |

| Transfer events | 1446(f) 10% withholding on foreign LP sales |

| Non-U.S. rules | CRS, AIFMD, DAC6, local filing dates |

My main takeaway: the biggest risk is usually not the rule itself. It’s missing paperwork, old forms, and mismatched reporting across the fund, GP, feeders, and SPVs.

The article below walks through those rules, who usually handles each filing, and how I’d set up the tracking process early.

How to Stay Compliant with U.S. International Tax Laws: FATCA, FBAR & Offshore Reporting Explained

sbb-itb-17e8ec9

The Main Global Reporting Rules VC Funds Need to Track

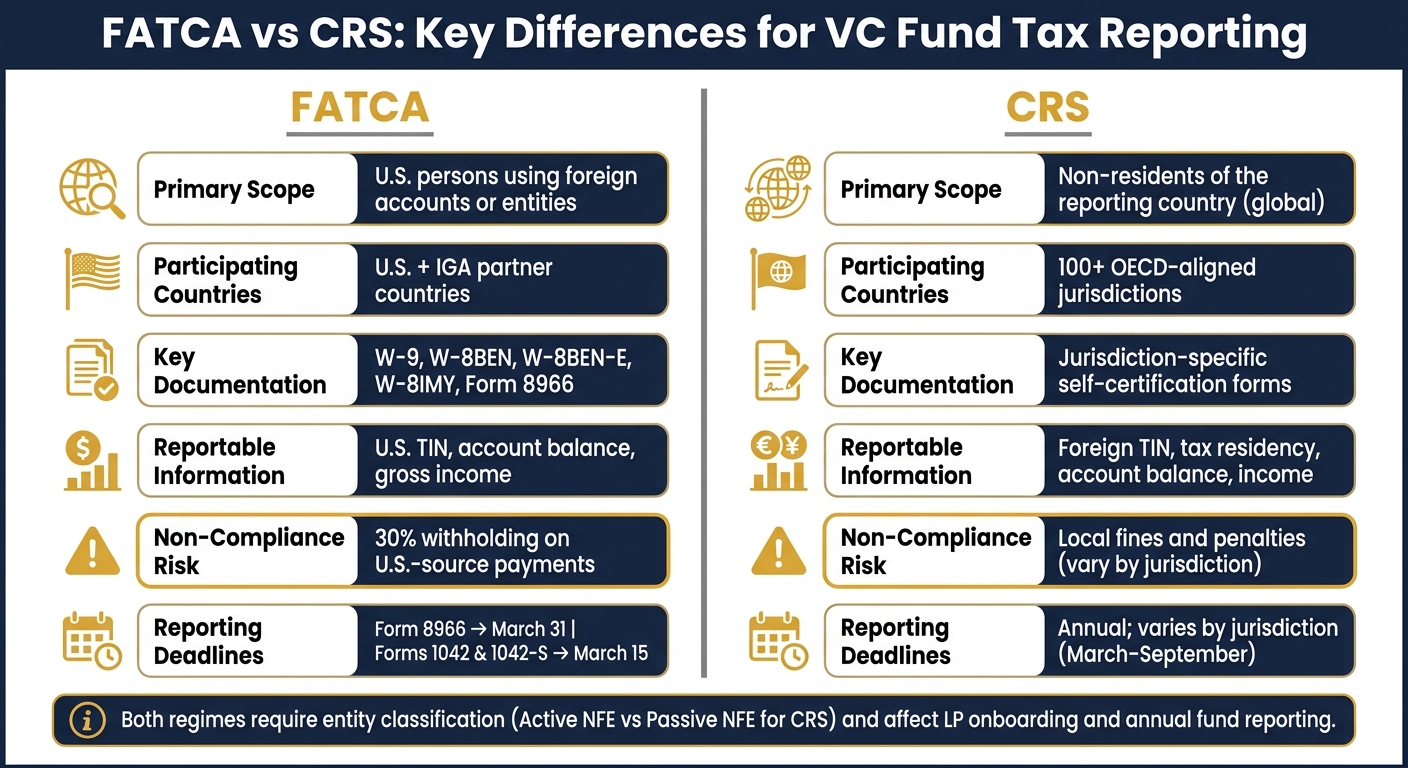

FATCA vs CRS: Key Differences for VC Fund Tax Reporting

FATCA, CRS, and BEPS drive most cross-border reporting for VC funds. They overlap, but they don't look at the same thing. Each one focuses on different facts, different parties, and different filings. Start with FATCA, because it shapes most investor onboarding and withholding controls.

FATCA: investor documentation, withholding, and annual reporting

FATCA is a U.S. law built to identify U.S. persons using foreign accounts or entities. For a VC fund, the day-to-day impact is pretty simple: if the fund or a related entity qualifies as a Foreign Financial Institution (FFI), it has to identify U.S. account holders and report them through IRS filing channels.

The main forms are the W-8 series for non-U.S. investors and Form W-9 for U.S. investors. In fund settings, the forms you'll see most often are W-8BEN, W-8BEN-E, and W-8IMY. These forms usually expire every three years, and once they expire, they should be treated as missing. That matters, because missing or expired W-8 forms can trigger default withholding.

The withholding rate is 30% on U.S.-source income when FATCA documentation is missing or invalid. The main annual filings are Form 8966 due March 31 and Forms 1042 and 1042-S due March 15. Treaty-based reduced rates are available only if the investor has provided valid documentation upfront.

CRS starts from a similar onboarding idea, but it points at a different group of taxpayers.

CRS: reporting non-U.S. tax residents and controlling persons

CRS is the OECD's global answer to FATCA. More than 100 jurisdictions have adopted it. Unlike FATCA, it requires financial institutions to identify investor tax residency and report relevant accounts to local tax authorities.

For VC funds with investors in CRS-participating countries, the main onboarding item is a self-certification form. That form captures the investor's tax residency and taxpayer identification number. Entity investors also need to be classified. The key split is whether the entity is an Active NFE or Passive NFE.

That classification drives the next step. It tells the fund whether it needs to identify controlling persons before accepting the LP. If the investor is a Passive NFE, the fund must report its controlling persons.

CRS reporting deadlines depend on the jurisdiction, but they usually fall sometime between March and September each year.

| Feature | FATCA | CRS |

|---|---|---|

| Primary Scope | U.S. persons | Non-residents of the reporting country (global) |

| Participating Countries | U.S. + IGA partners | 100+ OECD-aligned jurisdictions |

| Key Documentation | W-9, W-8 series, Form 8966 | Jurisdiction-specific self-certifications |

| Reportable Information | U.S. TIN, account balance, gross income | Foreign TIN, tax residency, account balance, income |

| Non-Compliance Risk | 30% withholding on U.S.-source payments | Local fines and penalties |

| Reporting Timeline | Annual (March 15 / March 31) | Annual (varies by jurisdiction, March–September) |

BEPS comes into play when the fund structure itself creates tax risk, not just investor reporting risk.

BEPS and country-by-country reporting in fund structures

BEPS focuses on whether a cross-border fund structure has real substance behind its tax position. For most VC funds, the main BEPS pressure points are treaty access, holdco substance, and CbCR, but CbCR usually matters only when the fund sits inside a large multinational group.

These global rules feed straight into U.S. partnership reporting and withholding.

U.S. Tax Reporting and Withholding for Cross-Border VC Activity

These rules usually show up in three places: partnership returns, withholding filings, and investor statements. In most VC funds, the order is pretty simple: partnership allocations first, withholding next, and regulatory filings after that.

Form 1065, Schedule K-1s, and foreign investor allocations

Every U.S. partnership files Form 1065, its annual partnership tax return. Each investor then receives a Schedule K-1 that shows their share of income, gains, losses, and deductions.

For funds with foreign LPs, that’s just the first layer.

If a fund has international activity or foreign partners, it also has to file Schedules K-2 and K-3. These cover partnership-level and partner-level international reporting items.

The big tax issue for foreign LPs is Effectively Connected Income (ECI). If the fund has ECI, foreign LPs may be subject to withholding on their allocable share at the highest graduated rates: 37% for individuals and 21% for corporations.

U.S. LPs may also need Form 8621 if the fund holds a PFIC.

Once the allocation reporting is done, the next step is withholding on foreign partner income.

Forms 1042, 1042-S, 1099, and treaty-based withholding rates

Form 1042 is the annual withholding tax return for U.S.-source income paid to foreign persons. Form 1042-S is the recipient-level statement that goes with it. Both are due March 15 .

FDAP income - dividends, interest, and similar fixed, determinable, annual, or periodical payments - is generally subject to 30% withholding under Section 1441. Lower treaty rates apply only if valid documentation is already on file .

The forms are straightforward:

- W-8BEN is for individual foreign investors

- W-8BEN-E is for foreign entities

Section 1446(f) comes into play when a foreign LP sells a partnership interest. In that case, the transferee must withhold 10% of the amount realized. If the transferee doesn’t withhold, the fund can become secondarily liable. That’s why a GP consent right in the LPA can serve as a useful checkpoint before a transfer closes.

Form 1099 handles domestic reporting for U.S. investors. Before filing, reconcile 1099s, K-1s, and 1042-S forms. If those reports don’t line up, problems tend to snowball.

Form PF, SEC reporting, and how they align with tax filings

Form PF is an SEC filing, not a tax return. Registered investment advisers with at least $150 million in private fund assets under management are generally required to file it.

It matters because the asset and exposure data on Form PF should line up with tax allocations and investor statements. When those numbers drift apart, they can trigger regulatory red flags that are much easier to avoid than explain.

Non-U.S. reporting rules create a separate set of obligations, and the next section covers those.

EU and Other Non-U.S. Reporting Rules That Can Affect VC Funds

Once U.S. tax filings are handled, the next layer is foreign reporting. This can come into play when a fund markets, sets up entities, or invests across borders. And yes, even U.S.-based VC funds can end up with European filing duties.

If a fund markets to EU investors or uses an EU feeder or SPV, two rules matter most: AIFMD and DAC6.

AIFMD reporting for funds with EU investor or marketing exposure

The Alternative Investment Fund Managers Directive (AIFMD) can apply when fund managers raise money from EU investors, even if the fund is formed in Delaware or the Cayman Islands. In plain English, access to EU capital through National Private Placement Regimes (NPPRs) can set off Article 24 reporting.

Under Article 24, the fund manager, or AIFM, reports details about the fund’s exposures, leverage, liquidity profile, and main markets. How often this report is due depends on AUM and the way the fund is set up. The filing duty generally sits with the fund manager, not the investors.

DAC6 is different. It is not about fund marketing. It is a separate disclosure regime aimed at reportable cross-border tax arrangements.

DAC6 disclosures for reportable cross-border arrangements

Unlike AIFMD, DAC6 turns on the structure of the transaction itself. DAC6 requires mandatory disclosure of cross-border tax arrangements that have reportable features. For VC funds, common triggers can include:

- standardized fund documents

- income recharacterization

- deductible cross-border payments to related parties in preferential-tax jurisdictions such as Luxembourg or Ireland

Who files depends on the parties involved. EU-based advisors, lawyers, or fund managers generally file first. But if your fund manager is U.S.-based and no EU intermediary is involved, the duty shifts to the relevant taxpayer, often the EU investor or the fund.

The deadline is tight: file within 30 days of the earliest trigger, whether the arrangement is made available, ready for implementation, or the first step has been taken. Don’t assume your advisor handled it. U.S. managers should ask for a filing reference or confirmation number. If there’s no process to spot reportable arrangements, that gap can become an internal control issue on its own.

For EU investors, it may help to include side letter clauses that require the fund manager to provide registration and disclosure numbers for the investor’s own tax returns.

Penalties for non-compliance vary a lot. They range from €25,000 to €100,000 in the Netherlands to €300,000 in Poland. That’s a steep price for a missed filing.

Building a Compliance Calendar and Filing Process

A simple framework for onboarding, data collection, and deadline tracking

Once the rules are clear, the next risk is simple: missed deadlines and source data that doesn’t match. In practice, the most common breakdown is missing or expired investor tax documentation. That’s why investor tax certifications should be collected before capital closes. After the close, chasing missing forms gets much tougher. And the stakes are higher than they seem, because the same investor data often feeds FATCA, CRS, withholding, and partnership reporting.

The next step is to map each entity - fund, GP, feeder, and SPV - to its own filing duties. A Delaware LP does not face the same rules as a Cayman feeder, so treating them the same can create problems fast. A master entity list helps keep things straight, especially when it includes named owners and due dates. It also helps to review AUM and other size thresholds every quarter so new filings don’t show up at the last minute.

Use one master calendar that ties each entity, each filing, and each owner back to the same source data.

| Regime | Inputs | Filing Deadline | Responsible Owner |

|---|---|---|---|

| FATCA (Form 8966) | W-8/W-9, GIIN, account balances | March 31 | Fund admin / GP |

| U.S. Withholding (1042/1042-S) | FDAP income, treaty claims | March 15 | Tax preparer / GP |

| Partnership Tax (K-2/K-3) | International tax items, foreign tax credit data | March 15 (Sept. 15 if extended) | Tax preparer |

| CRS Reporting | Tax residency, self-certifications, TINs | Annual; local deadline varies | Fund admin |

| Form PF | AUM, leverage, portfolio data | April 30 (annual) | CCO / finance team |

Where Lucid Financials fits into cross-border reporting workflows

Lucid Financials puts bookkeeping, tax support, and multi-entity reporting into one Slack-connected workflow, which helps teams keep filing data up to date.

Conclusion: the key reporting risks VC funds should address first

The goal isn’t only to file on time. It’s to keep investor data, entity data, and withholding data aligned across every return. Build the calendar early, before fundraising or distributions add more pressure to the reporting process.

FAQs

When does a VC fund need both FATCA and CRS reporting?

A venture capital fund may need to handle both FATCA and CRS reporting if it is treated as a financial institution in a jurisdiction where both rules apply.

Here’s the simple version:

- FATCA comes into play when the fund has U.S. investors or U.S. assets. In that case, it must report U.S. persons to the IRS.

- CRS applies when the fund is based in a country that has adopted the rule. Then, the fund must report non-resident investors to its local tax authority.

Same fund, two sets of reporting. The trigger depends on who the investors are, where the fund sits, and which tax rules that country follows.

How can a fund tell if a foreign LP triggers ECI withholding?

A fund needs to determine whether its activity rises to the level of a U.S. trade or business.

In most cases, plain-vanilla equity investments don't produce ECI. But that can change. ECI may come up when a fund has operating investments, receives management or consulting fees from portfolio companies, or invests in U.S. real property interests.

This isn't a one-time check. It should be reviewed every year because fund activity and portfolio company activity can shift over time.

If the fund generates ECI, it must withhold tax at 37% for individual foreign partners and 21% for corporations.

What should a VC fund track first to avoid cross-border filing errors?

Start with accurate investor onboarding and documentation. First, figure out each investor’s tax status and collect the right self-certification forms, such as IRS Form W-9 for U.S. persons or the W-8 series for non-U.S. persons.

Keep those records in a centralized, audit-ready system so you can support compliance with FATCA and the Common Reporting Standard.