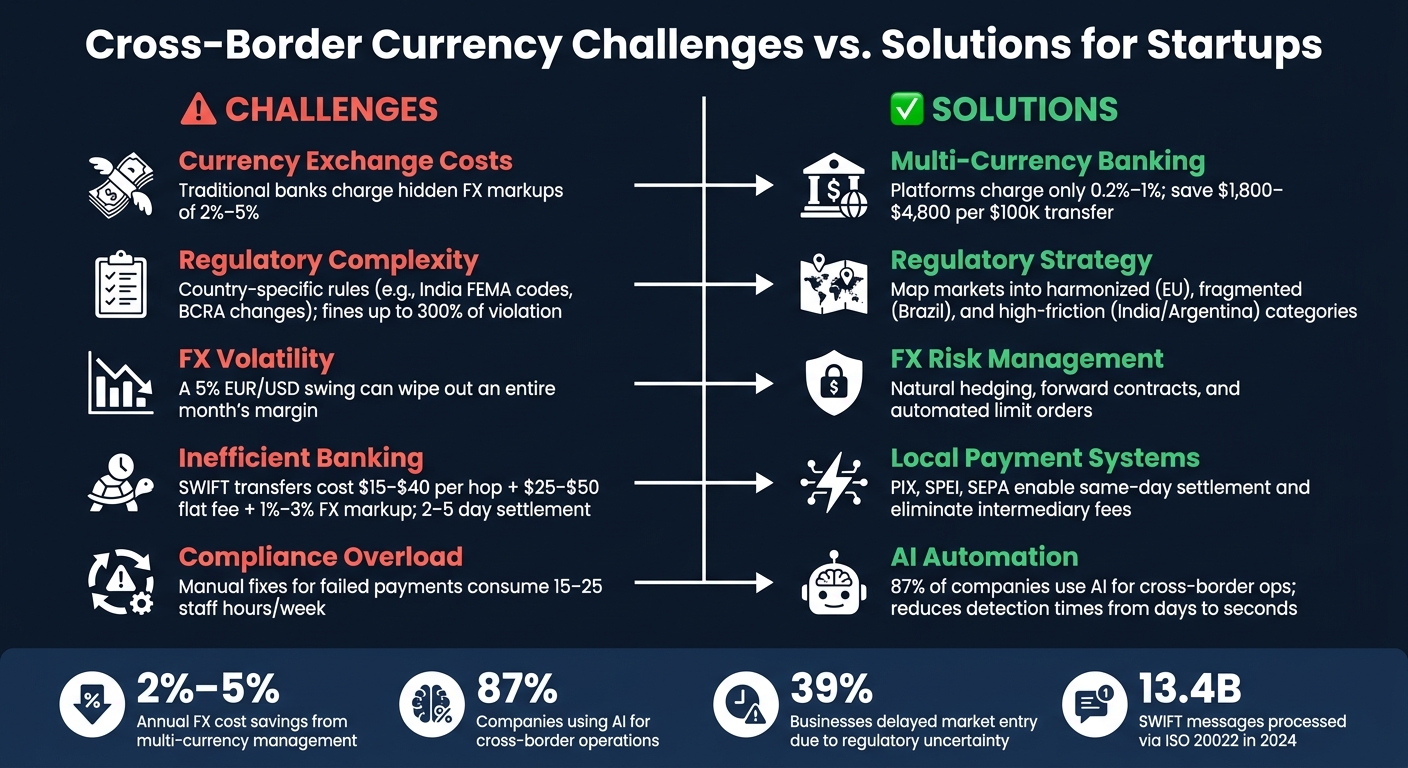

Expanding globally is exciting, but startups face serious challenges when managing cross-border currencies. From hidden fees to regulatory hurdles, these issues can quickly erode profits and complicate operations. Here's a quick breakdown of the key problems and solutions:

- Currency Exchange Costs: Traditional banks charge hidden FX markups (2%-5%), leading to unnecessary expenses.

- Regulatory Complexities: Different countries have unique rules for cross-border payments, like India's strict FEMA codes.

- FX Volatility: Fluctuations in exchange rates can disrupt financial planning and reduce margins.

- Inefficient Banking Systems: Slow, costly international transfers via SWIFT add to operational delays.

- Compliance Overload: Startups often lack resources to meet complex reporting requirements across markets.

Key Solutions:

- Multi-Currency Banking: Set up accounts to hold and transfer funds in different currencies, minimizing conversion costs.

- FX Risk Management: Use natural hedging, forward contracts, and limit orders to stabilize finances.

- Automation Tools: AI-driven platforms simplify compliance, reconciliation, and reporting, saving time and reducing errors.

- Local Payment Systems: Switch to regional systems like SEPA or PIX for faster, cheaper transactions.

- Regulatory Strategy: Map out country-specific compliance requirements and build a structured reporting calendar.

By adopting these strategies and leveraging technology, startups can reduce costs, manage risks, and streamline cross-border operations.

Cross-Border Currency Challenges vs. Solutions for Startups

Key Currency and Exchange Control Challenges

How Exchange Control Laws Differ by Country

When it comes to regulating cross-border money transfers, every country does things its own way, creating hurdles for startups trying to expand globally.

Take India as an example. Under the Foreign Exchange Management Act (FEMA), every cross-border transaction must go through an Authorized Dealer (AD) bank. Payments leaving the country need specific Reserve Bank of India (RBI) purpose codes. For instance, code S0205 is for SaaS subscriptions, while S1002 applies to digital advertising expenses. Using the wrong code can lead to regulatory scrutiny, blocked payments, or even fines as high as 300% of the violation amount.

One common error among Indian startups is using the Liberalised Remittance Scheme (LRS), which is meant for personal remittances (capped at $250,000), to pay for business tools like AWS or Slack. Mani Murugan, Finance & GST Lead at Bizeract, highlights this issue:

"The single biggest compliance mistake at Indian SaaS startups is paying for company tools through the founder's personal credit card under LRS... It is not a corporate expense channel."

Unlike the flexibility seen in some countries, India prohibits practices like notional cash pooling or multilateral netting, which are common in the U.S. In India, every transaction must be settled individually with proper documentation.

How FX Volatility Affects Startup Finances

Currency fluctuations don’t just chip away at profits - they can throw financial planning into chaos. Imagine a startup pricing contracts in euros but reporting in dollars. A 5% swing in the EUR/USD exchange rate could wipe out an entire month’s margin. This challenge is compounded when banks automatically convert incoming foreign payments into the local currency, creating double exposure for both income and vendor payments.

Managing multiple currencies effectively can lower annual FX costs by 2% to 5%. However, traditional tools like spreadsheets often combine multiple currencies into a single figure, making it hard to pinpoint where the real risks lie. This lack of clarity turns cash flow forecasting into guesswork.

Banking and Payment System Inefficiencies

Even with compliance in order, international money transfers remain expensive and slow. SWIFT wire transfers, for example, pass through several correspondent banks, each deducting fees of $15–$40 per hop. Add to that flat wire fees of $25–$50 per transaction and hidden FX markups of 1%–3% above the mid-market rate, and the costs quickly add up. Worse, these markups are often buried in the exchange rate, making them hard to spot.

Failed or rejected cross-border payments add another layer of inefficiency, eating up 15–25 hours of staff time each week for manual fixes. Switching to local payment systems like PIX in Brazil, SPEI in Mexico, or SEPA in Europe can drastically improve efficiency. These systems reduce settlement times from 2–5 business days to same-day processing and eliminate intermediary fees.

As Routefusion aptly points out:

"The transfer fee is the most visible cost and the least useful for comparison, because it tells you nothing about the four layers underneath."

These challenges underline the importance of adopting streamlined, multi-currency payment solutions to minimize inefficiencies and costs.

sbb-itb-17e8ec9

How to Build a Cross-Border Currency Management Framework

Setting Up Multi-Currency Banking

Relying on just a single U.S. bank account won't cut it for cross-border operations. Instead, you need a three-layer banking setup:

- Layer 1: A primary U.S. account for compliance, tax purposes, and FDIC insurance coverage.

- Layer 2: A multi-currency platform to hold, convert, and transfer funds between currencies at rates close to mid-market levels.

- Layer 3: Local receiving and payout accounts to handle payments in regions where global platforms face limitations.

As Jett Fu explains:

"A US bank account is one layer, not the whole strategy. It is one layer."

Costs can vary significantly between these layers. Traditional banks often charge FX markups ranging from 2% to 5%, while multi-currency platforms typically charge between 0.2% and 1%. On a $100,000 transfer, this difference could save a startup anywhere from $1,800 to $4,800 in a single transaction.

To reduce compliance risks, avoid consolidating all your funds in one institution. Once your banking framework is in place, the next step is to tackle FX risk management.

Managing FX Risk With Hedging and Pricing Policies

One of the most effective ways to manage FX risk is through natural hedging. This involves aligning your inflows and outflows in the same currency. For example, if you're earning euros from European customers, use those euros to pay European vendors. This strategy helps you avoid conversion fees and shields your margins from currency fluctuations.

For more predictable or larger currency exposures, forward contracts are a smart option. These contracts allow you to lock in today's exchange rate for a future payment. For instance, if you need to pay a UK contractor £50,000 in 90 days, a forward contract can protect you from a potential rise in the pound's value.

Additionally, report metrics like ARR (Annual Recurring Revenue) and NRR (Net Revenue Retention) in both functional and reporting currencies. This approach ensures that exchange rate changes don’t distort your performance figures. As Ray Rike of Benchmarkit points out:

"Constant-currency ARR reporting isn't optional for global SaaS companies; it's the only way investors can fairly evaluate growth."

For currencies prone to volatility, automated limit orders can help you trade only when rates hit your desired target.

With these strategies in place, you can move on to establishing operational controls for your currency transactions.

Operational Controls for Currency Transactions

To strengthen your cross-border currency management, start by ensuring clear visibility of all inflows and outflows in their original currencies before any conversions. Combining everything into a single USD figure can obscure where your currency risks are accumulating.

Automation is key for streamlining reconciliation. Tools like API-driven sub-ledgers or Virtual Account Numbers (VANs) allow you to separate funds by customer, entity, or workflow, creating clean audit trails without manual intervention. Platforms that integrate with accounting software like NetSuite or Xero can make this process even smoother.

Additionally, pairing banking redundancy with role-based spend governance - where specific roles define who can initiate, approve, and execute payments - ensures operational security and audit readiness.

Modern financial platforms, such as Lucid Financials, bring all these elements together. By combining multi-currency banking, automated reconciliation, and strict spend controls, startups can gain real-time financial insights, maintain investor-ready reporting, and ensure smooth, compliant cross-border operations.

Mercury vs Wise: Best Cross‑Border Payments for Startups

Regulatory Reporting and Compliance for Cross-Border Transactions

Once your banking and FX risk framework is set, the next priority is compliance. Each market you enter has its own set of rules, deadlines, and thresholds. Missing any of these can lead to costly consequences.

How to Map Exchange Control Laws in Your Target Markets

Regulations vary widely from one market to another. For example, the EU uses a passporting model, allowing one license to cover more than 27 countries. In contrast, India requires a local subsidiary with a net worth of at least INR 15 crore (around $1.6M USD), which is 4.5 times higher than the EU's EMI requirement. Brazil adjusts capital requirements based on transaction volume, while Argentina's central bank (BCRA) can change foreign exchange rules with little notice.

"Launching a payment business in a single country is a licensing exercise. Launching one across borders is a regulatory strategy problem." - 2payapp

To navigate these complexities, group your target markets into categories: harmonized regions like the EU, fragmented markets like Brazil, and high-friction markets such as India or Argentina. Then, determine if local incorporation is required, if foreign ownership is restricted, and what the capital requirements are. Also, identify specific reporting thresholds. For instance, in the US, the Travel Rule applies at $3,000, while cash transaction reports are mandatory at $10,000. Meanwhile, the EU imposes no minimum threshold for crypto-assets.

A real-world example highlights the importance of licensing strategy. In early 2025, a Singapore-based fintech handling SGD 500M annually attempted to enter the EU through Spain. The application process took 10 months, during which competitors licensed in Lithuania and Ireland expanded into Spain and captured market share. The fintech eventually filed in Ireland, where approval took about six months, but the delay cost them an estimated €2–3M in lost revenue. The lesson? Prioritize licensing speed over proximity to your first client.

This initial mapping lays the groundwork for creating a structured reporting calendar and an efficient data management system.

Building a Reporting Calendar and Data Structure

Compliance hinges on having a solid data structure that aligns with regulatory requirements. Proper data mapping ensures that you meet thresholds without room for error. Using ISO 20022 messaging standards can help, as these provide detailed data fields for originator and beneficiary information, making it easier to comply with Travel Rule requirements and minimizing false positives in sanctions screenings. In 2024, SWIFT processed 13.4 billion messages using this format. Additionally, integrating Legal Entity Identifiers (LEIs) into your system aids in accurately identifying counterparties during sanctions checks.

Create a tiered reporting calendar to streamline compliance:

- Daily: Track operational liquidity and invoice-level details.

- Weekly: Generate rolling forecasts (usually over 13 weeks) to assess working capital.

- Monthly/Quarterly: Conduct strategic reviews and prepare regulatory filings.

"If you wait for bank statements to understand your liquidity, you are already behind the market." - Monica De Salazar

For startups that can't afford a full-time compliance officer, hiring fractional Chief Compliance Officers (CCOs) or Money Laundering Reporting Officers (MLROs) can be a practical solution. These roles, often required for sponsor bank approval in the US, UK, and Canada, come with personal liability but can save costs for early-stage businesses.

Using AI to Automate Compliance and Reporting

Managing compliance manually - across various bank portals and spreadsheets - is time-consuming and prone to errors. AI-driven tools can solve these inefficiencies by automating compliance processes and reducing detection times from days to seconds.

AI platforms can classify transactions, flag FX exposure breaches instantly, and generate statutory filings with minimal manual input. For example, in India, AI tools are used to reconcile software export inflows with outward remittance patterns, meeting quarterly requirements set by the Reserve Bank of India. They can also manage "No-Permanent Establishment" declarations from vendors, which are critical for avoiding higher withholding tax rates on cross-border SaaS payments.

The numbers back this up: 87% of companies now use AI in some capacity for cross-border operations, and 39% of businesses have delayed market entry due to regulatory uncertainty. While AI won't replace compliance expertise, it eliminates the repetitive tasks that slow down the process.

"As trade becomes more fragmented and unpredictable, businesses are realizing they can't wait for certainty to return. They're using technology and automation to stay compliant, manage risk, and keep moving forward." - Craig Reed, GM of Cross-Border, Avalara

Take Lucid Financials as an example. Their AI platform provides real-time financial data, ensuring startups are always prepared for compliance deadlines or investor requests. This allows founders to focus on scaling their business instead of scrambling to meet regulatory demands.

Conclusion: Turning Cross-Border Currency Challenges Into Manageable Processes

Recap of Key Challenges and Solutions

Managing cross-border currencies comes with a range of hurdles that can escalate if ignored. From unpredictable FX volatility to outdated banking systems and ever-changing regulations, these issues can eat away at your margins.

The key to tackling these challenges lies in a structured approach. Tools like multi-currency accounts and forward contracts help minimize conversion hassles and shield profits from currency fluctuations. Meanwhile, tiered reporting calendars keep compliance deadlines on track, avoiding last-minute scrambles.

Dave Huggett, Founder of Lucid Foreign Exchange, highlights a common pitfall in the industry:

"I realized that half the problem with the industry is that there is a huge over-focus on 'getting the absolute best rate.' This leads businesses and individuals to hold off or rush their transaction, without thinking about the fundamentals." - Dave Huggett

The takeaway? Focus on security, timing, and structure. Chasing marginal rate improvements while overlooking compliance or risk management can expose startups to unnecessary dangers.

These challenges don’t just call for better strategies - they also demand cutting-edge technology.

How AI-Driven Financial Systems Help Startups

Adding AI into the mix takes these strategies to the next level. Traditional methods - like juggling spreadsheets, logging into multiple banking portals, or manually tracking compliance - simply don’t scale as startups grow. Expanding into new markets increases the number of transactions and FX risks, making manual processes impractical.

AI-powered financial platforms step in to bridge this gap. For instance, Lucid Financials integrates directly with tools like Slack, providing founders with real-time financial insights, on-demand investor-ready reports, and automated bookkeeping. By handling tasks like reconciliation, forecasting, and reporting, AI frees up founders to focus on strategic growth instead of reactive problem-solving.

When paired with a structured framework, AI simplifies the complex world of cross-border currency management, turning it into a manageable process for global startups.

FAQs

When should a startup open multi-currency accounts?

Startups that deal with frequent international payments, earn revenue in multiple currencies, or require greater control over cross-border transactions should think about opening multi-currency accounts. These accounts can simplify operations and help minimize the challenges of managing exchange rates and transaction fees.

How do I choose between natural hedging and forward contracts?

When deciding between natural hedging and forward contracts, the choice hinges on how predictable your cash flow is and your approach to managing risk.

- Natural hedging involves balancing revenues and expenses in the same currency. This approach reduces foreign exchange (FX) risk without incurring additional costs, making it a cost-effective option.

- Forward contracts, on the other hand, allow you to lock in exchange rates for future transactions. This provides certainty, especially if you have predictable payments or receipts in foreign currencies.

You don’t have to choose one exclusively - combining both methods can be a smart move. The right mix depends on your financial forecasts and how much risk you're comfortable taking on.

What data is needed to automate cross-border compliance reporting?

To streamline cross-border compliance reporting, you'll need to gather some essential data. This includes transaction details, information about the parties involved, the purpose of the transaction, and the source of funds. Additionally, you'll need to track exchange rates and collect key compliance documents, such as business registration papers, identity verification records, and tax documentation. Having accurate and complete data not only makes the process smoother but also ensures you meet regulatory standards effectively.