AI is transforming credit risk analysis for startups by enabling faster, smarter, and more inclusive lending decisions. Unlike older models that rely on limited historical data, AI processes over 1,600 data points in real time, including alternative data sources like education, banking habits, and utility payments. This shift improves loan approval rates, reduces costs, and minimizes credit losses. For example:

- AI-powered tools cut underwriting costs by 50% and reduce credit losses by up to 15x.

- Loan approval rates increased by 27–44%, while maintaining or lowering default rates.

- Processing times dropped from days to minutes, enabling faster decisions.

AI techniques like machine learning, natural language processing (NLP), and real-time data monitoring are key drivers. Startups using these methods can analyze unstructured data, track borrower behavior continuously, and dynamically adjust credit limits. However, compliance with strict regulations and mitigating algorithmic bias remain challenges.

Whiteboard series - How AI and ML are revolutionizing credit risk modeling?

sbb-itb-17e8ec9

AI Methods Used in Credit Risk Models

Startups are reshaping credit scoring by using three key AI techniques: machine learning, natural language processing (NLP), and real-time data monitoring. These approaches address the limitations of traditional scoring models and open up new possibilities for evaluating creditworthiness.

Machine Learning for Credit Scoring

At the heart of modern credit risk models is ensemble learning, which combines multiple algorithms to detect patterns that individual models might overlook. For instance, Upstart relies on Gradient Boosting Machines (XGBoost) to analyze over 1,600 variables, such as employment history, education, and bank transactions. This is a sharp contrast to the narrower focus of FICO models, as AI incorporates a vast array of data points.

A critical step in this process is feature engineering, where raw data is transformed into predictive insights. Credolab, for example, processes around 80,000 raw data points - like device interactions and app usage - into nearly 11 million features. From this, it narrows down to the 30–50 most predictive signals. This method is especially effective for borrowers with limited credit histories, often referred to as "thin-file" borrowers.

To meet regulatory demands for transparency, startups use Explainable AI (XAI) tools like SHAP and LIME. These tools break down credit decisions, making it clear why an application was approved or denied. Michele Tucci, Chief Strategy Officer at Credolab, highlights the importance of transparency:

Logistic regression remains a cornerstone because it delivers a transparent, statistically sound framework that balances predictive power with the explainability demanded by regulators.

Accuracy is key in credit scoring. Metrics like a Gini coefficient above 50% and a Kolmogorov-Smirnov (KS) statistic above 40 are benchmarks for strong model performance. Upstart's AI implementation, for instance, achieved a 73% reduction in losses at comparable approval rates compared to older systems. This advanced machine learning approach lays the groundwork for incorporating unstructured data and real-time updates.

Natural Language Processing and Alternative Data

AI also taps into text-based data to enrich credit evaluations. NLP tools analyze sources like customer reviews, social media, news articles, and professional networks for credit signals. A notable example is LendNova, introduced in January 2026, which processes raw credit bureau text using a language model. This eliminates the need for manual feature engineering. As Kiarash Shamsi, lead author of the research, explains:

LendNova transforms risk modeling by operating directly on raw, jargon-heavy credit bureau text using a language model that learns task-relevant representations without manual feature engineering.

Generative AI further enhances these efforts by refining human judgment. For instance, tools like ChatGPT can analyze and improve loan officers' written assessments, uncovering patterns and signals that humans might miss, especially in descriptions of borrower behavior.

Document processing is another area where AI shines. Agentic AI systems can read and normalize data from PDFs, scanned tax returns, and financial presentations, reconstructing accurate financial statements. This automation not only saves weeks of manual effort but also reduces costs by eliminating the need for specialized data engineers.

The impact is clear. Integrating alternative data using NLP has led to a 20% improvement in risk prediction accuracy and a 20% increase in credit approval rates for first-time borrowers. By 2025, over 65% of lenders had adopted AI-powered models that incorporate non-traditional data sources.

Real-Time Data Integration and Monitoring

Real-time data integration allows for continuous risk evaluation, in contrast to traditional models that rely on quarterly or monthly updates. AI systems now monitor borrowers minute-by-minute through live data streams. Martini.ai, for example, launched a platform in July 2025 that tracks supply chains and news for 3.5 million firms, generating 600 billion predictions daily. CEO Rajiv Bhat emphasizes the importance of this shift:

Just because assets are illiquid doesn't mean risks are. And we've reached a point where risk needs to be evaluated in real time. Not quarterly. Not monthly. But minute-by-minute.

Using graph neural networks, these systems map relationships across businesses. If one company in a supply chain faces financial trouble, the model immediately adjusts the risk for all connected entities - suppliers, customers, and competitors. Adaptive models further refine predictions by recalibrating as new data - like transaction flows or market events - becomes available, ensuring accuracy even as conditions change.

Cloud-based platforms play a big role in automating these processes. An API-first architecture can handle up to 80% of underwriting, streamlining decision-making. Kolleno’s credit management software, used by companies like 1Password and DNA Payments, provides real-time credit monitoring and alerts. This system has reduced overdue balances by 71% within three to six months.

The time savings are substantial, too. AI-driven systems can cut loan processing times from days or weeks to minutes or hours. These advancements not only improve risk assessment but also make credit decisions faster and more accessible, aligning perfectly with the fast-paced demands of startups.

Case Studies from Startup Implementations

Success Stories from AI-Powered Fintech Startups

Startups in the fintech space are reshaping their lending operations by adopting AI-driven credit risk systems, leading to faster processes, reduced costs, and improved accuracy.

Uplinq, in collaboration with Visa, showcased impressive results in January 2025. Their AI-powered credit decisioning platform enabled financial institutions to cut underwriting operating costs by 50% and reduce credit losses by 15x. By integrating environmental, market, and community data with traditional credit metrics, the platform has supported over $1.4 trillion in underwritten loans. Ron Benegbi, Uplinq's CEO, highlighted:

AI-powered credit decisioning not only broadens access to affordable credit... but also significantly improves lenders' underwriting efficiency and profitability – a true win for all involved.

Marshall Capital Group, an equipment finance company, adopted Uptiq's AI-Powered Agentic Loan Origination System in June 2025. The results were transformative: a 70% reduction in manual workloads, 40% faster decision-making, and a threefold increase in deal volume. In just seven days, the firm transitioned from contract signing to a fully operational digital application. Founder and CEO Bradon Marshall shared:

Uptiq's AI-powered LOS didn't just automate our processes - it unlocked new capacity overnight. We can onboard vendors, process deals, and manage risk faster than ever.

Fora Financial, a small business lender, turned to Ocrolus' AI-driven document automation to streamline costly manual review processes. This implementation cut data extraction times to under 15 minutes, enabling loan decisions within four hours and funding in less than 24 hours. Automated authenticity scoring also reduced bank statement verifications by over 50%. Jesse Goldman, COO of Fora Financial, explained:

Maintaining customer service standards with manual data review at the beginning of the process was proving expensive... The platform eliminates manual keying by credit analysts... and delivers various credit model inputs that were previously unavailable.

An African e-commerce startup leveraged finbots.ai's creditX platform to scale its lending operations dramatically, growing from 1,000 to over 40,000 MSMEs in just six months. This resulted in a 10% drop in gross credit losses, an 8% rise in approvals, and application processing times reduced to under one second.

Measured Results from AI-Driven Credit Risk Models

The numbers speak for themselves. Upstart's machine learning platform, which evaluates over 1,600 variables, approved 44% more loans compared to traditional FICO-based models while lowering interest rates by an average of 36%. At the same time, it achieved a 73% reduction in losses at comparable approval rates. By 2024, 80% of loans processed through Upstart's platform were fully automated.

| Metric | Impact of AI Adoption |

|---|---|

| Underwriting Operating Costs | 50% Reduction |

| Manual Workload | 70% Reduction |

| Loan Approval Rates | 44% Increase |

| Credit Losses | 15x Reduction / 73% Fewer Losses |

| Loan Automation Rate | 80% of loans fully automated |

| Decision Speed | From days to under 4 hours (or even seconds) |

These examples highlight a broader trend: startups embracing AI-driven credit risk models are seeing tangible gains in profitability - some reporting a threefold increase in line-of-business profitability - all while extending credit access to underserved borrowers.

Performance Metrics of AI in Credit Risk Analysis

AI vs Traditional Credit Risk Models: Performance Comparison

Comparing AI-Powered and Older Credit Risk Models

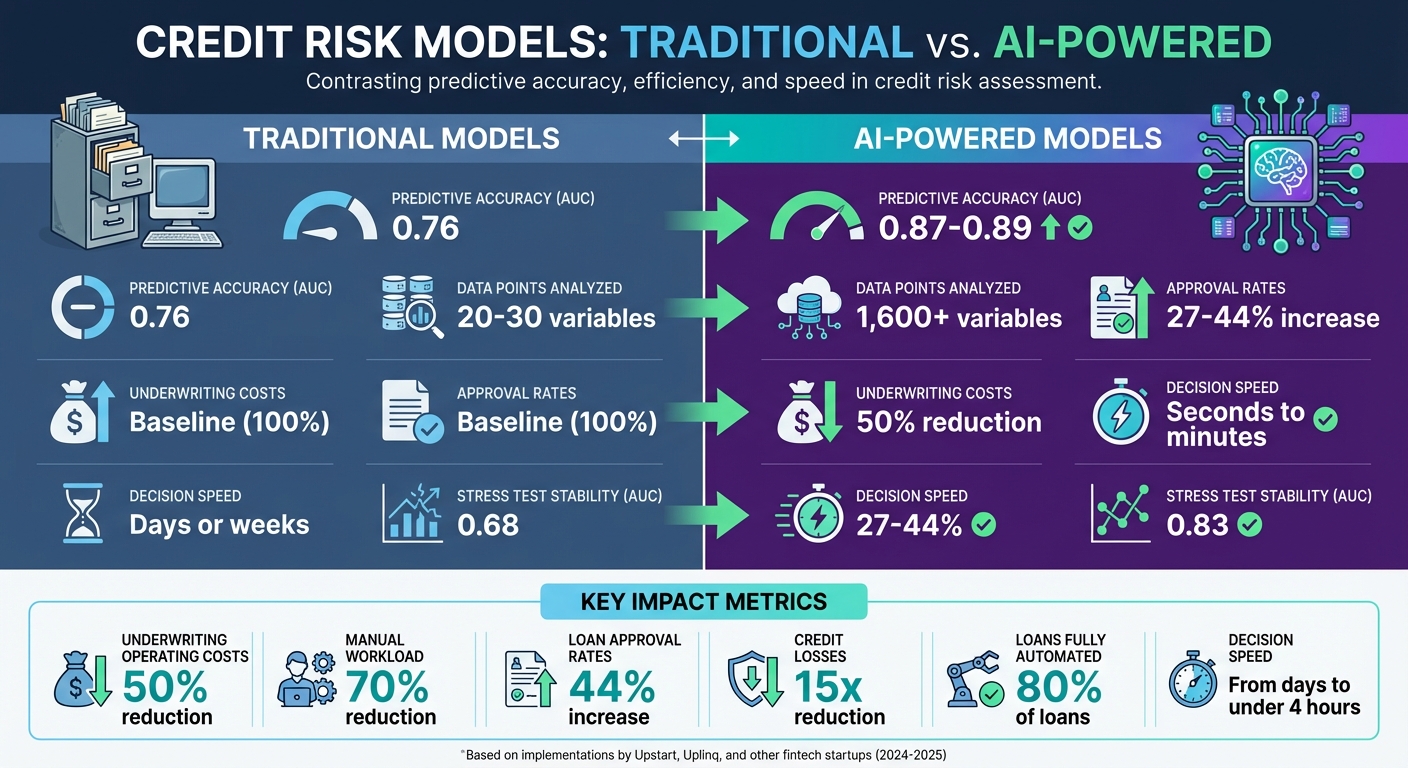

The numbers speak for themselves when comparing AI-driven models to traditional credit risk analysis methods. AI models consistently outperform older approaches, achieving an AUC-ROC (Area Under the Curve - Receiver Operating Characteristic) of 0.87–0.89, compared to just 0.76 for traditional logistic regression models. Even under stress scenarios, such as a simulated 20% income decline, AI models maintain an impressive AUC of 0.83, while traditional models drop significantly to 0.68.

| Metric | Traditional Models | AI-Powered Models |

|---|---|---|

| Predictive Accuracy (AUC) | 0.76 | 0.87–0.89 |

| Data Points Analyzed | 20–30 variables | 1,600+ variables |

| Underwriting Costs | Baseline | 50% reduction |

| Approval Rates | Baseline | 27–44% increase |

| Decision Speed | Days or weeks | Seconds to minutes |

| Stress Test Stability (AUC) | 0.68 | 0.83 |

AI-powered systems also bring operational efficiency to the forefront. They process credit applications in seconds, making it possible to cut underwriting costs by 50%. These advancements aren't just about speed - they pave the way for more effective and inclusive lending practices.

Better Decision-Making and Inclusion

AI models do more than just accelerate processes; they enhance decision-making in ways that broaden access to credit. By analyzing over 1,600 data points - including factors like education, employment history, and banking behavior - AI identifies creditworthy borrowers who might otherwise be overlooked by traditional systems.

This capability is especially vital for the 45 million Americans who lack sufficient credit history for conventional scoring methods. By incorporating alternative data, AI enables startups to extend credit to "credit invisible" populations. Additionally, fairness audits using tools such as SHAP ensure that these systems provide equitable treatment across different demographic groups, addressing concerns about bias and fairness.

Challenges and Future Directions in Startup AI Risk Systems

Regulatory Compliance and Bias Mitigation

For startups implementing AI credit models, navigating strict regulations and addressing algorithmic opacity remain daunting tasks. One major issue is the black box problem - regulators demand that credit decisions be both explainable and verifiable. The Consumer Financial Protection Bureau (CFPB) has made it clear that vague, checkbox-style adverse action notices are no longer acceptable. As CFPB Director Rohit Chopra emphasized:

Creditors must list specific denial reasons, even when models appear complex

.

Another hurdle is outdated legacy systems, which often slow down AI decision-making processes and compromise data accuracy. To mitigate these risks, startups must prioritize automated tracking and version control to ensure that training data respects privacy regulations. However, AI systems also risk perpetuating historical biases, potentially leading to discriminatory outcomes based on factors like race, gender, or location.

The regulatory environment has become even more stringent in 2026. The Financial Services AI Risk Management Framework, introduced in February 2026, outlines 230 control objectives spanning governance, data handling, and model development. Startups must also comply with regulations like the EU AI Act (which classifies lending as high-risk), GDPR, and the CFPB's Personal Financial Data Rights Rule. Amy S. Mushahwar and Chloe Rippe from Lowenstein Sandler LLP summed up the evolving landscape:

The defining question for 2026 would no longer be whether artificial intelligence (AI) is being used responsibly but whether organizations truly understand and govern the systems they have already built

.

Establishing a compliant AI credit system isn't cheap. A fully scalable system with governance and bias detection frameworks can cost between $120,000 and $350,000+. Even a minimum viable product (MVP) for early-stage testing typically requires $35,000 to $85,000.

These challenges are pushing startups to innovate rapidly, setting the stage for new trends in the AI credit space.

Trends in 2026

As startups work to overcome compliance and bias issues, several emerging trends are reshaping the landscape. Explainable AI (XAI), once a competitive edge, has become a regulatory necessity. Tools like SHAP and LIME are now standard for generating audit-ready explanations of AI decisions. Another innovation is machine unlearning, which allows specific data to be erased from trained models without requiring a full retrain - an important safeguard when dealing with improperly sourced data.

Real-time risk pricing is also gaining momentum. This approach enables credit limits and interest rates to adjust dynamically based on borrower behavior and economic conditions. Meanwhile, new tools like LendNova, launched in early 2026, leverage Large Language Models to process raw credit bureau data directly, eliminating the need for manual feature engineering. Privacy-enhancing technologies, such as differential privacy, synthetic data, and homomorphic encryption, are becoming essential for balancing data utility with stringent privacy laws.

The potential for growth in this space is immense. AI in banking is forecasted to surpass $64 billion by 2030, with an annual growth rate of 32%. However, challenges remain - 65% of lenders report difficulties in obtaining AI-ready data, even though 89% recognize AI as critical to the lending process. Startups that can navigate these complexities while maintaining a focus on governance, transparency, and fairness stand to gain significantly in this rapidly evolving market.

Conclusion

AI has reshaped how startups tackle credit risk analysis, bringing clear benefits like improved approval rates, reduced costs, and better loss control. It has also opened doors for underserved borrowers by enabling more inclusive credit access. Fintech companies using AI-driven credit scoring and real-time decision-making have seen faster evaluations, better scalability, and more tailored credit terms.

Keeping up with industry advancements is critical. Experts forecast that by 2026, generative AI for document analysis, agentic AI safeguards, and AI-driven climate risk assessments will become more prominent. Startups that delay adopting AI risk losing out on smarter credit strategies and enhanced loss reduction opportunities.

However, credit risk analysis is just one piece of the puzzle. To ensure long-term growth, startups need modern financial systems. Platforms like Lucid Financials are stepping in to fill this gap by combining AI-powered bookkeeping, tax services, and CFO support. With tools like Slack integration, Lucid Financials provides investor-ready reports in just seven days, allowing founders to focus on scaling their ventures.

For startups, the real question isn’t whether to embrace AI but how quickly they can integrate it into both credit decision-making and financial operations. Those who act now - while also implementing strong governance and decision-making frameworks - will gain a competitive edge in approval speed, pricing accuracy, and risk management.

FAQs

What data does AI use to score borrowers without a credit history?

AI leverages alternative data sources to evaluate borrowers who lack a traditional credit history. This includes information like utility payments, rent records, telecom activity, online behavior, social media usage, and behavioral trends. By analyzing these factors, AI can provide a more complete picture of someone's creditworthiness, even when conventional credit data isn't available.

How do lenders explain AI credit decisions to regulators and applicants?

Lenders are turning to explainable AI (XAI) techniques to shed light on how input data impacts credit decisions. These approaches aim to make the decision-making process more transparent by identifying the key factors that influence outcomes. This not only helps lenders stay compliant with regulations but also builds trust with applicants. For example, agencies like the CFPB (Consumer Financial Protection Bureau) stress the importance of using interpretable algorithms to ensure decisions can be clearly explained. By following these regulatory guidelines, lenders can make AI-based credit decisions easier to understand and justify for both regulators and consumers.

What does it cost to build an AI credit risk model that meets compliance rules?

Building an AI credit risk model that meets regulatory requirements can be a costly endeavor, influenced by several factors such as the model's complexity, the variety of data sources involved, and the specific regulatory standards it must adhere to. Although precise costs aren't outlined, these projects often demand a substantial investment in cutting-edge technology, robust data management systems, and compliance frameworks. The final expense can differ significantly depending on the project's scope and the unique needs of the model.