Secondary market transactions allow founders, employees, and early investors to sell existing shares to private buyers without issuing new shares or diluting ownership. These transactions provide liquidity without requiring an IPO or acquisition, making them an attractive option for late-stage startups like those in Series C and beyond. Here's a quick summary:

- What They Are: Private resales of existing shares, not tied to raising new capital.

- Why They Matter: Offer liquidity for stakeholders while maintaining the company's cap table.

- Key Trends: The global secondary market grew 45% from 2023 to 2024, reaching $162 billion, with 60%-75% of unicorn startups using these transactions.

- Challenges: Legal complexities, potential valuation impacts, and tax considerations.

Secondary transactions are reshaping how startups manage liquidity, especially as IPO timelines stretch longer. Tools like Lucid Financials are helping streamline the process by improving transparency and simplifying cap table management.

Key Considerations for Secondary Market Transactions in Series C and Beyond

Liquidity Needs and Stakeholder Goals

In Series C and later stages, managing liquidity while maintaining the integrity of the cap table becomes a delicate balancing act. It's important to address the unique liquidity needs of founders, employees, and early investors while keeping broader market trends in mind.

Secondary transactions often cater to three key groups, each with distinct motivations. For founders, secondaries provide an opportunity to diversify their personal finances. This might mean buying a home, supporting their families, or mitigating concentration risk without waiting for an IPO, which could still be years away. As Tom C. Schapira, Founder and CEO of Imagine Capital Group, explains:

"A well-timed secondary sale can provide the means to buy a new home... It also allows founders to enjoy the fruits of their labor while continuing to focus on building the company".

That said, large sell-offs can create negative perceptions in the market, signaling a lack of confidence. To counter this, sales are often limited to 10% of vested holdings and paired with a primary funding round to stabilize valuation.

Early employees face a similar challenge. Liquidity programs, like tender offers, help convert their "paper wealth" into actual cash. This not only rewards employees but also aids in retention. Companies like Stripe and SpaceX are well-known for implementing recurring tender offers to provide liquidity while maintaining control over the cap table.

For early investors and limited partners (LPs), secondary transactions are a way to realize returns and rebalance portfolios. These transactions also help consolidate smaller, early-stage shareholders into larger secondary funds, cleaning up the cap table ahead of an IPO. Between 2023 and 2024, the global secondary market expanded from $112 billion to $162 billion - a 45% increase - showing how these transactions are becoming a standard practice.

Company Approval and Right of First Refusal (ROFR)

The Right of First Refusal (ROFR) gives the company or its investors the option to match the terms of an external buyer, rather than outright blocking a sale. This typically involves a waiting period - often 30 to 45 days - during which the company decides whether to exercise its right. Priority is usually given to the company, followed by major investors on a pro-rata basis, and sometimes other shareholders.

While ROFR is designed to protect the company, it can complicate transactions. External buyers might hesitate to invest time and effort in due diligence if the company could step in at the last moment. To navigate this, selling shareholders should carefully review governing documents and set clear expectations about the waiting period. On the company side, having a transparent and well-documented process is crucial. Providing a consistent disclosure package to eligible participants and assigning ROFR to a trusted investor can streamline the process, ensuring liquidity events proceed smoothly without depleting company cash unnecessarily.

Maintaining Financial Transparency

The private secondary market operates without centralized infrastructure, making transparency a cornerstone for fair pricing and accurate valuations. Inadequate or misleading disclosures can lead to legal issues, while clear and consistent practices reassure investors and demonstrate a high level of operational discipline. Transparency not only fosters trust but also smooths the path for secondary transactions in late-stage companies.

Standardizing disclosure materials is key. This includes providing a company charter, an as-converted cap table, a KPI deck, risk factors, and a modeled liquidation waterfall. It's also important to account for the typical 15–30% discount on common stock compared to preferred stock. For high-demand late-stage companies, this discount may narrow to 5–15%. Dan Gray of Equidam highlights the importance of normalizing liquidity:

"When liquidity is normalized, it ceases to be gossip-worthy and becomes just another part of a professional private-company operating system".

Tools like Lucid Financials can be instrumental in this process. By integrating directly with company systems, Lucid enables real-time, investor-ready reporting. This ensures clean books, precise cap table tracking, and continuous financial visibility. With everyone - buyers, sellers, and the board - operating from the same set of facts, trust is built, reducing information gaps and making secondary transactions more efficient.

sbb-itb-17e8ec9

Understanding the Secondary Market in Venture

How Secondary Market Transactions Work

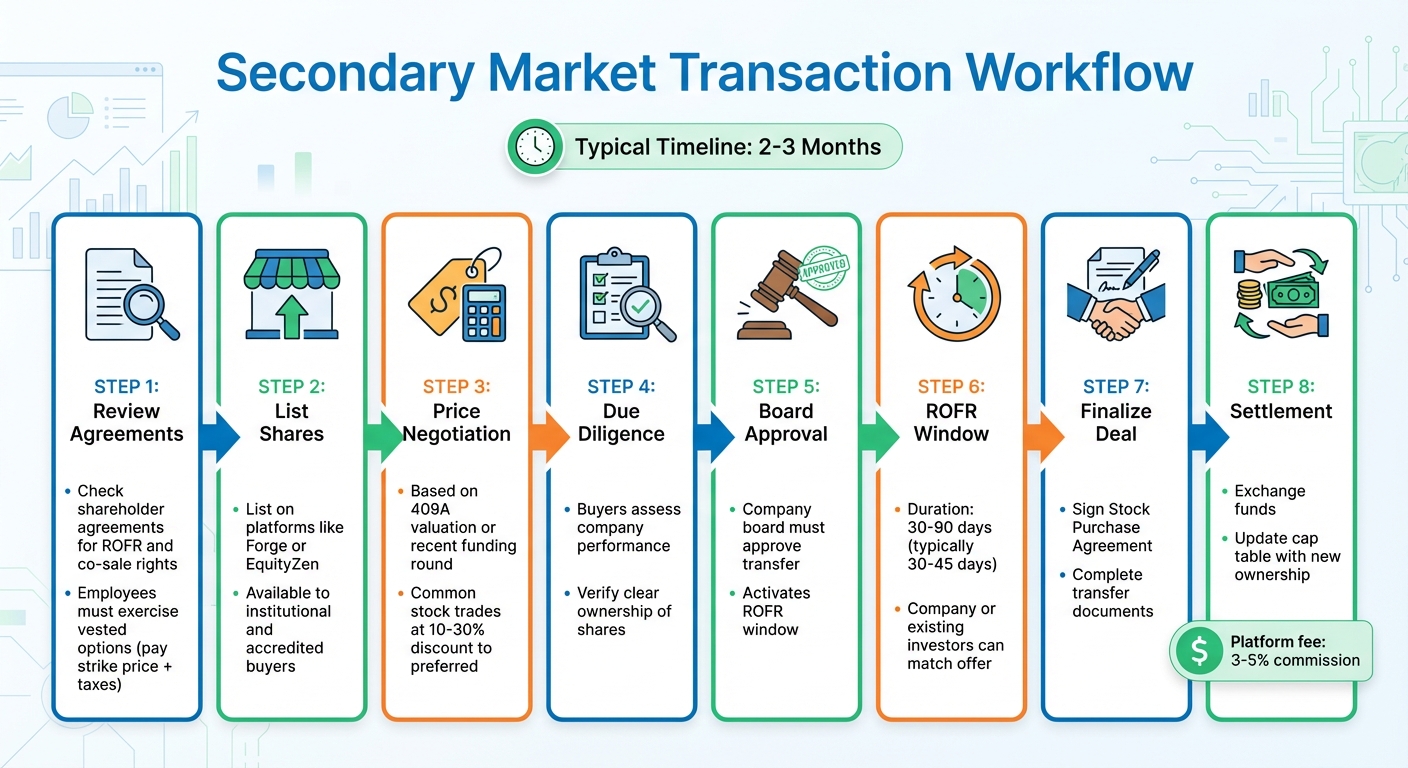

Secondary Market Transaction Workflow: 8-Step Process for Series C+ Startups

Transaction Workflow

Secondary market transactions follow a detailed process that typically spans two to three months. The first step for sellers is to review shareholder agreements for any restrictions on transfers, such as Right of First Refusal (ROFR) or co-sale rights. Employees with vested options often need to exercise them - this means paying the strike price and covering any related taxes - before their shares can be sold.

Once ownership is confirmed, shares are listed on secondary marketplaces like Forge or EquityZen, where institutional and accredited buyers can browse available shares. Pricing discussions generally rely on the latest 409A valuation or the most recent primary funding round. Common stock often trades at a 10% to 30% discount compared to preferred shares. Buyers then conduct due diligence to assess company performance and verify clear ownership of the shares.

The company’s board must approve the transfer, which activates the ROFR window - usually lasting 30 to 90 days. During this period, the company or existing investors have the option to match the buyer’s offer. If the ROFR is not exercised, the seller and buyer finalize the deal by signing a Stock Purchase Agreement and completing the required transfer documents. Afterward, funds are exchanged, and the company’s cap table is updated to reflect the new ownership. Platforms that facilitate these transactions typically charge a commission of 3% to 5%, with minimum transaction amounts varying by marketplace.

With this process in place, companies in later funding stages, particularly Series C and beyond, are better positioned to handle such transactions.

Prerequisites for Series C and Beyond

Secondary transactions become more feasible at the Series B stage or later, as startups at this point usually show substantial progress and have a valuation that buyers can confidently assess. Companies must be prepared to share essential financial data and operational metrics with institutional buyers, often under a Non-Disclosure Agreement (NDA). A recent 409A valuation or a primary funding round helps establish a fair market value for the shares.

Additionally, companies need governance structures that can handle secondary transactions. This includes formal board approval processes and compliance with shareholder agreements. Many late-stage startups also include transfer restrictions in their bylaws to prevent undesirable investors from joining the cap table. Meeting these conditions helps companies maintain control over their ownership structure while using secondary markets to provide liquidity.

The secondary market has seen tremendous growth over the past decade. Venture secondary deal volume grew from $13 billion in 2012 to $60 billion in 2021. This increase highlights how startups, which now often remain private for 10 years or more, rely on secondary markets as a critical liquidity option rather than just a niche solution.

With the workflow and prerequisites established, let’s turn to the requirements for investors who participate in these transactions.

Accredited Investor Requirements

Participation in secondary market transactions is restricted to accredited investors who meet specific U.S. financial criteria. For individuals, this typically means an annual income of at least $200,000 (or $300,000 with a spouse) or a net worth exceeding $1 million, excluding the value of their primary residence.

Buyers must formally verify their accredited status, which limits the pool of potential investors compared to public markets. This exclusivity has led to a market increasingly dominated by institutional players, such as secondary funds, hedge funds, and late-stage venture capital firms. These entities have the resources and expertise to navigate the complexities of secondary transactions.

Interestingly, the global secondary market for limited and general partnership interests expanded by 45% from 2023 to 2024, growing from $112 billion to $162 billion. This growth underscores the increasing importance of secondary markets as a liquidity tool for both startups and their investors.

Advantages and Disadvantages of Secondary Transactions

Benefits of Secondary Transactions

Secondary transactions provide a quick way to turn private shares into cash. This is particularly helpful for founders, employees, and early investors who often have their wealth tied up in company equity. By selling these shares, they can access liquidity without waiting for the company to go public. For employees, this process can ease frustrations tied to locked-up equity, boosting morale and helping companies keep their top talent.

Another advantage is that these transactions don’t dilute ownership. Instead of issuing new shares, existing ones are simply sold to new investors. Companies can also use these transactions to streamline their cap table by buying out smaller or inactive investors. This makes the company’s structure more appealing to institutional investors. Additionally, secondary transactions can help set a market-driven valuation, which can guide future fundraising efforts.

The numbers show how secondary transactions are gaining traction. In 2025, the global secondary market hit $226 billion in volume - a 41% jump from the previous year. GP-led transactions grew by 51% to $106 billion, while LP-led deals increased by 34% to $120 billion. In February 2026, employees at companies like Clay, Linear, and ElevenLabs participated in tender offers, selling equity at valuations up to 60% higher than their last funding rounds. For instance, Clay’s employee shares were valued at $5 billion, compared to $3 billion in August 2025.

While these transactions offer flexibility and establish market-based pricing, they also come with challenges.

Drawbacks of Secondary Transactions

One downside is that secondary transactions can increase the valuation of common stock under 409A pricing. This raises the strike price for future stock option grants, potentially making equity less appealing to new hires. Additionally, if founders or executives sell large amounts of stock, it could signal reduced confidence in the company’s future. Bringing in new investors through one-off sales might also lead to governance issues, as less-experienced investors may complicate future decision-making.

These transactions can also be expensive and time-consuming. Legal and operational costs are high, and Right of First Refusal (ROFR) delays - ranging from 30 to 90 days - can create uncertainty, causing buyers or sellers to back out. Selling shares at a discount, often 10% to 30% below the last funding round, can set a negative tone for future fundraising. Additionally, tax complications add another layer of risk. For example, ISO holders could face disqualifying dispositions, and transactions must comply with SEC rules like Rule 144.

"Secondary sales typically impact the 409A price of common stock... making the upside potential much smaller [for future employees]." - OnlyCFO

Comparison Table: Benefits vs. Drawbacks

| Aspect | Benefits | Drawbacks |

|---|---|---|

| Shareholder Liquidity | Converts private shares to cash without waiting for an IPO | – |

| Company Capital | Doesn’t affect the company’s cash position | No new funds are raised for the business |

| Dilution | No dilution; ownership is transferred | Can introduce less-desirable investors to the cap table |

| Valuation | Helps establish a market-driven valuation | Can inflate 409A valuations, increasing stock option strike prices |

| Employee Retention | Provides liquidity, aiding in talent retention during long private periods | Large founder sales may signal waning confidence in the company |

| Administrative Complexity | – | High legal costs and potential delays from ROFR processes |

| Tax Treatment | May qualify for QSBS exclusion of up to $10 million in gains | Risk of triggering disqualifying dispositions and facing complex tax scenarios |

These factors highlight the trade-offs involved in secondary transactions, offering insight into both their potential and their risks in today’s market.

Trends and the Future of Secondary Markets

Institutional Investors and Platform Growth

The secondary market has evolved significantly from its early, informal days. By 2024, private secondary transactions hit $152 billion, marking a 39% growth compared to the previous year. Fast forward to January 2026, monthly bid and ask volumes soared to $38.11 billion, nearly doubling December 2025’s $19.36 billion. This rapid expansion highlights a major shift: in 2024, 71% of all exit dollars came from secondary transactions rather than traditional IPOs or M&A deals. This shift underscores how secondary markets have become a primary source of liquidity in late-stage funding rounds.

Institutional players are increasingly treating secondaries as a permanent part of their portfolios. For example, StepStone Group raised $3.3 billion for what became the largest venture capital secondary fund ever in 2024/2025, designed to meet the growing need for liquidity in a sluggish IPO market. Other major firms like BlackRock and Coller Capital have launched multi-billion-dollar funds focused on secondaries. Meanwhile, evergreen funds from Hamilton Lane and StepStone now offer accredited retail investors access to pre-IPO portfolios with quarterly liquidity windows. Regulatory changes are also shaping the landscape: in June 2025, the UK's Financial Conduct Authority introduced PISCES, a framework for controlled, time-limited share trading, with the London Stock Exchange as the first approved operator.

"Venture capital liquidity solutions have become a structural requirement. The market has evolved, not just in how capital is deployed, but in how and when it returns." - Ruben Dominguez, Author

These developments are redefining exit strategies, paving the way for longer private lifespans in the startup world.

Longer Private Timelines for Startups

Startups are staying private far longer than they did a decade ago. The annual recurring revenue (ARR) needed for a successful IPO has climbed from $80 million in 2008 to about $250 million in 2026. For European venture portfolios, the median time to exit now exceeds 11 years. With IPO opportunities limited and M&A activity selective, secondary markets have become the primary outlet for liquidity. They allow founders, employees, and early investors to cash out without waiting for a full exit.

This trend has fueled a surge in secondary market activity. By 2024, venture secondaries made up 29% of all venture deal activity, compared to just 16% in 2020. High-profile companies like Stripe and Revolut have embraced this shift, running large-scale tender offers in 2024 and 2025 to provide liquidity for employees and early investors. For example, Revolut’s 2025 secondary sale attracted participation from firms like Giano Capital. Similarly, SpaceX and OpenAI, which are eyeing public markets in 2026, continue to rely on structured secondary sales to manage their combined $2.3 trillion private market valuation.

"Extended private company timelines mean that once the IPO market jump-starts, a robust backlog of eligible startups will be ready to sustain the exit momentum." - Emily Zheng, Senior Analyst, PitchBook

Interestingly, AI startups are bucking the trend of lengthy private timelines. While most startups take 5–7 years to reach secondary liquidity, AI companies like Cursor and Perplexity have done so in just 3 years. In the first half of 2025, AI startups accounted for 35% of total listed secondary volume, with AI/ML secondary trading volume growing an astonishing 1,104% between 2023 and 2025.

How Financial Tools Like Lucid Financials Enable Transparency

As secondary transactions become more frequent and complex, maintaining financial transparency is more important than ever. Accurate cap tables and clean financial records are now essential for late-stage startups navigating recurring liquidity events. Modern platforms are stepping in to simplify these processes.

Lucid Financials is one such platform, combining bookkeeping, tax services, and CFO support into a single AI-powered solution. For startups conducting tender offers or direct secondary sales, Lucid automates cap table updates and ensures financial statements reflect the latest ownership structures. The platform creates investor-grade forecasts and board-ready reports with just one click, streamlining the due diligence process for buyers.

Lucid also integrates with Slack to provide real-time updates on runway, spending, and performance metrics - key for pricing secondary sales and managing liquidation waterfalls. With detailed books delivered in just seven days and continuous financial tracking, Lucid equips startups with the tools they need to thrive in the fast-paced secondary market of 2026. As secondary windows become standardized and recurring, having a platform like Lucid isn’t just helpful - it’s a strategic advantage.

Conclusion

Secondary market transactions have grown from occasional side deals into a central part of late-stage startup financing. They provide much-needed liquidity for founders, employees, and early investors, especially as companies remain private for 8–12 years and the IPO market remains selective. The steady growth in secondary markets highlights their importance in today’s financial ecosystem.

For successful secondary transactions, preparation and transparency are critical steps:

- Review shareholder agreements: Understand rights of first refusal and transfer restrictions early on.

- Identify preferred buyers: Maintain cap table integrity by working with trusted buyers.

- Standardize disclosures: Provide consistent information like key performance indicators, as-converted cap tables, and audited financials.

- Align 409A appraisals: Coordinate schedules to avoid unexpected tax issues for future employee grants.

These practices help maximize the benefits of secondary transactions.

"Secondary sales are a fantastic tool for turning equity into outcomes without rushing toward an IPO or raising money you don't need." - Chris Nash

Financial transparency underpins every successful transaction. Buyers now expect enterprise-grade reporting, real-time cap table accuracy, and investor-ready forecasts. This is where technology plays a pivotal role. For example, Lucid Financials simplifies the process by combining bookkeeping, tax services, and CFO support into one AI-powered platform. With features like clean books in seven days, one-click board reports, and Slack-integrated runway tracking, Lucid ensures you're always ready for due diligence and pricing discussions.

As secondary liquidity windows become a recurring feature rather than a one-time event, having the right systems in place is more important than ever. Companies like Stripe and SpaceX have set the standard by running semiannual liquidity programs with rigorous financial controls and transparent processes. By focusing on strong governance, clear communication, and modern financial tools, late-stage startups can effectively manage liquidity, build trust, and stay agile in today’s dynamic financial landscape.

FAQs

How do secondaries affect my 409A and future option strike prices?

Secondary transactions can influence your 409A valuation and the strike prices for stock options, particularly if shares are sold at prices exceeding the current 409A value. However, the extent of this impact hinges on whether the sale price accurately represents the fair market value (FMV) or is driven by liquidity demands. If substantial secondary sales occur and they are deemed material events or significantly shift the company’s perceived value, a new 409A valuation may be necessary.

What can a company do to make ROFR less likely to derail a sale?

To minimize the chances of a Right of First Refusal (ROFR) complicating a sale, companies can take a few proactive steps. One approach is to narrow the scope and duration of the ROFR agreement, ensuring it’s limited to specific circumstances or a set timeframe. Another option is to negotiate a waiver clause, which can provide flexibility in certain situations.

It’s also important to implement clear, time-bound procedures for exercising the right, helping to prevent delays. Additionally, focusing on efficient decision-making and maintaining open communication throughout the sale process can significantly reduce the risk of unnecessary setbacks.

What tax issues should founders and employees watch for in a secondary?

In secondary market transactions, founders and employees need to keep an eye on potential tax pitfalls. One major concern is having gains classified as compensation, which can lead to higher tax rates. To avoid this, careful planning and structuring are essential.

Another critical aspect is ensuring compliance with Qualified Small Business Stock (QSBS) rules. Following these rules can help unlock tax benefits, such as exclusions or favorable capital gains treatment.

Working with a tax advisor is highly recommended. They can help navigate the complexities, reduce liabilities, and ensure you’re taking full advantage of any available tax benefits.