Late payments hurt startups. They drain cash reserves, disrupt operations, and force businesses to spend time chasing invoices instead of growing. Predictive analytics solves this by using historical data to anticipate payment delays, giving you control over cash flow.

Here’s how it works:

- Analyzing Patterns: Machine learning identifies risks by studying payment histories and customer behavior.

- Risk Scoring: Assigns scores to invoices, prioritizing collections based on likelihood of delay.

- Real-Time Alerts: Flags issues early, triggering automated workflows to address potential delays.

- Improved Outcomes: Companies report up to a 40% reduction in overdue payments and faster cash flow recovery.

Platforms like Lucid Financials integrate these tools seamlessly, helping startups avoid cash crunches and focus on scaling their business.

Understanding Payment Delays and Their Impact on Startups

What Causes Payment Delays

Payment delays can arise from a variety of issues. One of the most common is administrative errors - things like misplaced invoices, misinterpreted payment terms, data entry mistakes, or poorly managed client accounting systems. In fact, manual accounting processes typically have a 2% error rate, and correcting just one mistake can cost a company about $53. When teams are stretched thin, these errors can easily lead to overlooked invoices.

Another major problem is unclear payment terms. If contracts don’t clearly spell out due dates, acceptable payment methods, or penalties for late payments, clients might interpret the terms however they see fit. On top of that, technical issues - like bank delays, manual approval processes, or transfer holds - can further slow things down.

Then there’s willful neglect, where clients intentionally delay payments to use startups as a source of interest-free credit while managing their own cash flow challenges.

Recognizing these causes highlights why ensuring timely payments is so crucial for startups trying to maintain steady cash flow.

How Payment Delays Hurt Startups

The consequences of payment delays go beyond minor inconveniences - they can seriously disrupt a startup’s ability to operate smoothly. These delays create what’s often called "operational drag", where startups are forced to spend valuable resources chasing payments and managing overdue accounts. Unlike larger companies with dedicated collections departments, startups often rely on one or two people to handle finances while juggling other responsibilities. This time drain could instead be spent on growing the business or improving products.

"Late payments from clients can disrupt more than just your cash flow - they can derail your business's operations entirely." - Ashley Nguyen, Content Strategist, Ramp

Late payments also push startups into tough financial positions. They may need to rely on credit, delay important investments, or face higher financing costs, all of which put additional strain on already limited resources. When cash is tied up in unpaid invoices, it prevents startups from funding growth opportunities or making key hires at the right time.

Among CFOs surveyed in 2026, 77.9% identified improving the cash flow cycle as "very or extremely important" to their strategy, with the figure climbing to 93.5% for high-performing companies. This underscores just how critical managing cash flow is to staying competitive and achieving long-term success.

sbb-itb-17e8ec9

Late Payment Prediction in Business Central | How to Set Up & Use It

How Predictive Analytics Prevents Payment Delays

How Predictive Analytics Prevents Payment Delays: 4-Step Process

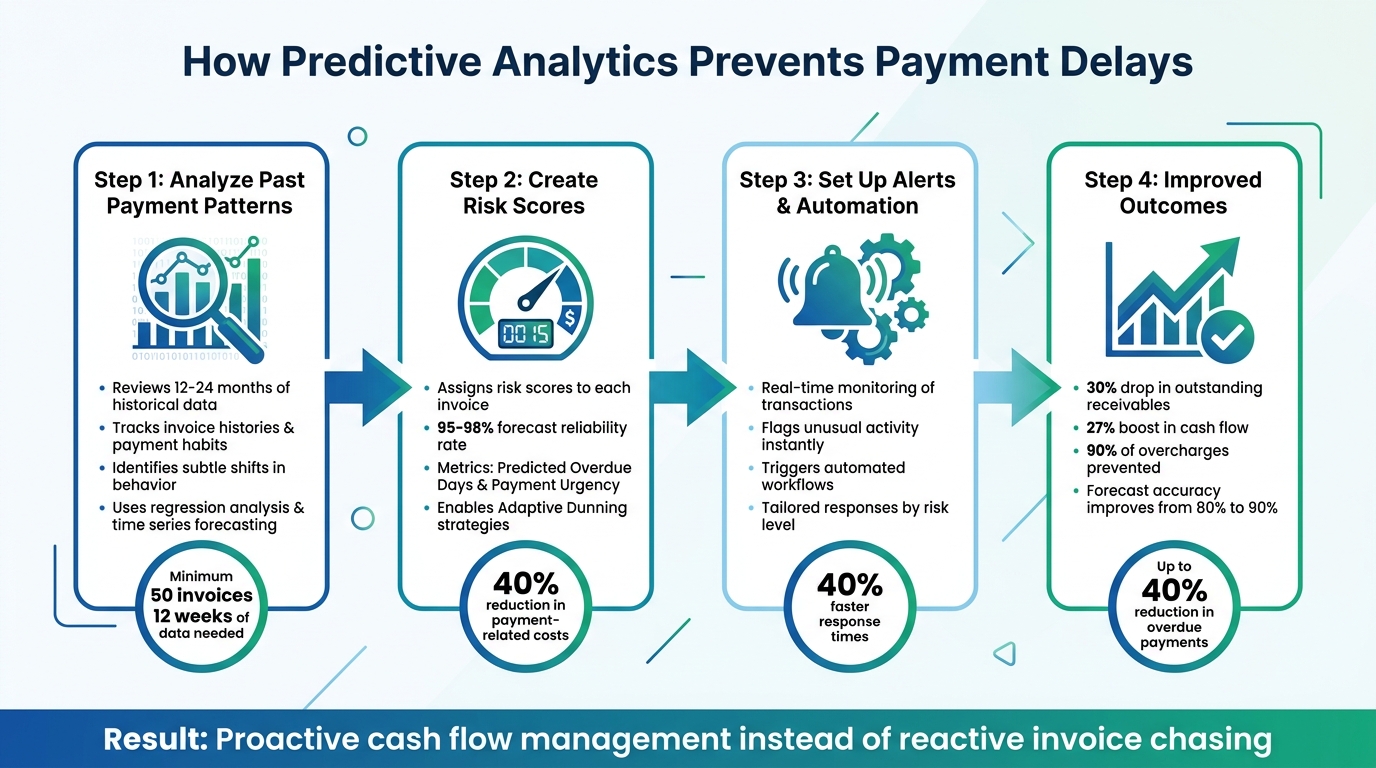

Predictive analytics has become a game-changer for startups dealing with delayed payments. Instead of reacting to overdue invoices, these tools use machine learning to anticipate potential issues, giving businesses the chance to act early and maintain steady cash flow.

Analyzing Past Payment Patterns

Predictive models dig into historical customer data - like invoice histories, payment habits, transaction records, and communication trends - to identify patterns that might signal future delays. For instance, if a typically punctual client starts paying later than usual, the system raises a red flag. These models also catch more subtle shifts, such as changes in the volume of transactions or slight delays in payment timing.

To deliver accurate predictions, these systems need a solid dataset. A minimum of 12 weeks or 50 invoices is often required, though experts suggest collecting 12–24 months of data to account for seasonal variations. Advanced analytics techniques, such as regression analysis and time series forecasting, help predict both individual payment risks and broader seasonal trends. Some systems even use propensity models to estimate the chances of a slightly overdue invoice escalating into a serious delinquency.

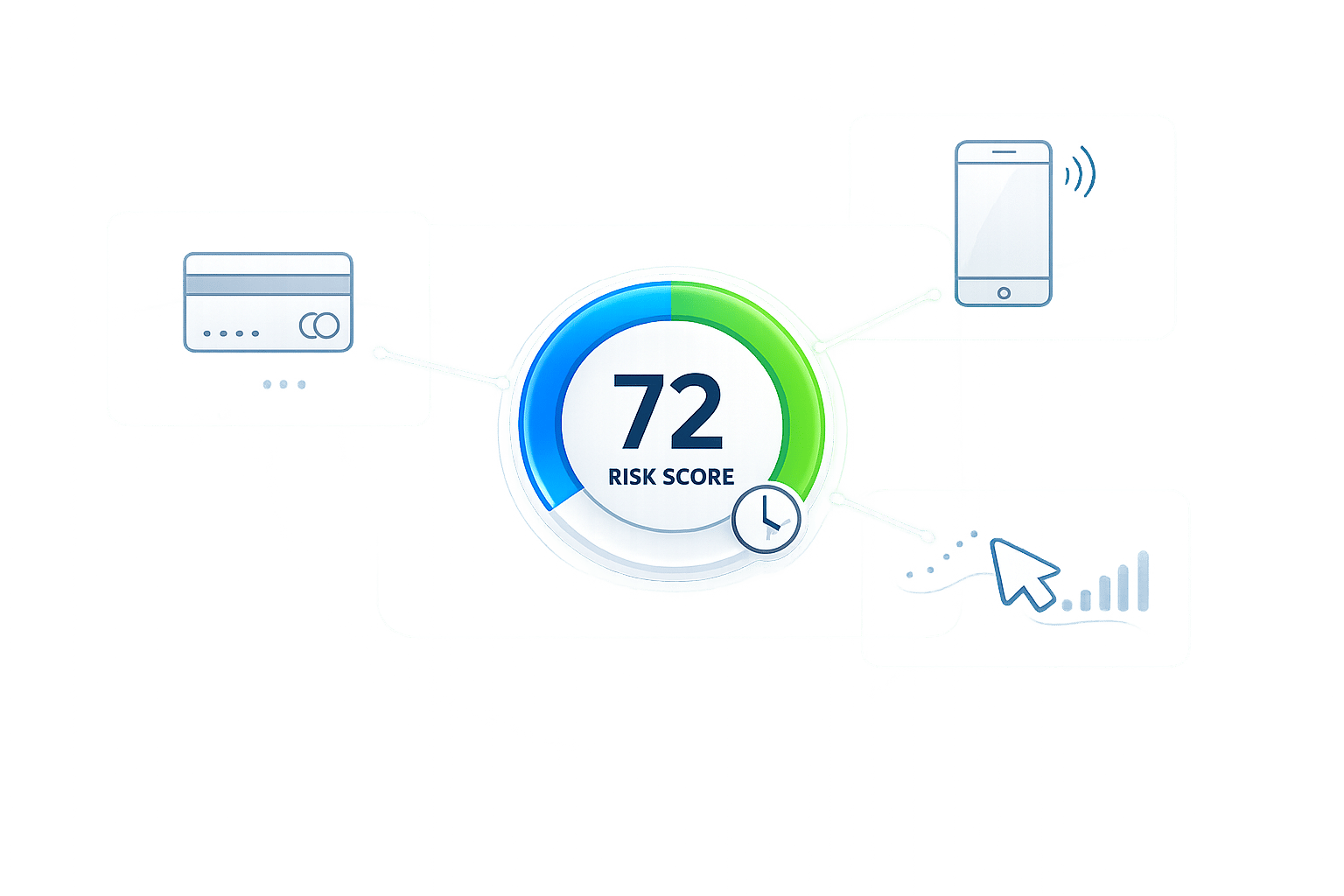

Creating Risk Scores for Invoices

Once patterns are identified, the next step is assigning risk scores to invoices. These scores are based on both internal payment histories and external factors, helping teams prioritize their collection efforts. Predictive models can achieve forecast reliability rates of 95–98%, which can reduce payment-related costs by around 40%.

Metrics like "Predicted Overdue Days" and "Payment Urgency" scores help create actionable to-do lists for collections teams. One study found that using these methods led to a 30% drop in outstanding receivables and a 27% boost in cash flow. These risk scores also enable "Adaptive Dunning", a strategy that tailors collection efforts to each customer. For example, a low-risk client might receive a friendly reminder for a minor delay, while a high-risk account could be escalated for immediate follow-up.

Setting Up Alerts and Automated Workflows

Real-time alerts are where predictive analytics truly shines. These systems continuously monitor transactions and flag unusual activity - such as unexpected payment amounts, sudden vendor changes, or deviations from a customer’s typical behavior. When risk thresholds are crossed, automated workflows spring into action. These might include sending a polite reminder for an initial delay, offering flexible payment options to a reliable client facing temporary challenges, or escalating chronic late payments for further intervention.

Businesses using predictive analytics report faster response times - up to 40% quicker when dealing with payment disruptions. Additionally, AI implementations can prevent about 90% of overcharges from impacting financial results. Predictive tools also enhance forecasting accuracy, improving it from roughly 80% to 90%. Modern platforms integrate seamlessly with ERP systems, offering live dashboards that replace outdated spreadsheets. This real-time visibility lets you see which invoices need immediate attention, which customers are at risk of paying late, and when to expect cash inflows. For startups, this proactive approach is key to ensuring steady cash flow and fueling growth.

Lucid Financials uses predictive analytics to provide real-time insights and proactive cash flow management, keeping you ahead of payment delays so you can concentrate on growing your business.

How to Implement Predictive Analytics for Payment Management

Connecting Predictive Analytics to Your Financial System

Start by collecting 12–24 months of clean historical data, including payment dates, customer profiles, communication histories, and transaction patterns. This data helps capture seasonal trends and lays the foundation for accurate predictions. Make sure to clean the data thoroughly - removing duplicates and fixing inconsistencies - since errors can undermine the accuracy of your models.

The technical setup usually involves three key steps: evaluating your current accounts receivable software for integration points, establishing secure data pipelines, and validating the predictive models using historical data. To ensure a smooth transition, consider a phased rollout. Test the system on a small segment of your customer base first to evaluate its accuracy before scaling it up.

Platforms like Lucid Financials simplify this process by integrating predictive analytics directly into their systems. They sync with your existing financial data, providing real-time insights without requiring complex manual configurations. Once your system is connected, the focus shifts to tailoring collection strategies based on the identified risk levels.

Adjusting Collection Strategies Based on Risk

When your system assigns risk scores to customers, use them to customize your approach to collections. For instance, low-risk clients - those with about a 20% likelihood of paying late - might only need automated, friendly email reminders. On the other hand, high-risk clients with a roughly 70% chance of delays may require stricter measures, such as upfront deposits or revised payment terms.

Automated "nudge ladders" can streamline your outreach. Start with a polite email reminder before the due date, escalate to an SMS after the payment deadline, and send a formal notice if the delay continues. To maintain positive relationships with reliable customers, reserve escalated actions for cases where the risk exceeds 60%. Always include an "I've already paid" link in your communications to let customers exit the sequence quickly if they've settled their accounts.

AI tools can also help refine your messaging. For example, tone-checking ensures early reminders remain empathetic. Additionally, offering incentives like a 2% discount for payments made within five days can encourage prompt payments. This tailored, data-driven approach strengthens your overall payment management strategy.

Tracking Results with Key Metrics

Once you've adjusted your collection strategies, it's essential to track their effectiveness. Key metrics like Days Sales Outstanding (DSO) provide a clear picture of your cash flow health. Other important measures include Time-to-First-Action and Collection Cycle Duration, which offer insights into the efficiency of your collection process.

Segmented dashboards can help you identify which strategies are working best, while A/B testing - comparing AI-driven workflows to manual processes - quantifies the impact of predictive analytics. For example, a precision-engineering company reduced its DSO from 58 to 33 days in just one quarter, cutting overdue balances significantly and saving valuable time.

Finally, regularly reviewing cases where predictions fell short can help refine your risk indicators and account for seasonal variations. This continuous improvement ensures your predictive analytics system remains effective over time.

Conclusion

Predictive analytics is transforming payment management by shifting the focus from reactive responses to proactive strategies. By analyzing historical data, assigning risk scores, and automating customized collection workflows, startups can pinpoint at-risk invoices before they become overdue. Companies leveraging AI-driven payment analytics have reported a 40% reduction in uncontrollable payment costs and forecast accuracy rates between 95% and 98% on large datasets.

Moving away from rigid aging buckets to dynamic, behavior-driven AI allows for personalized outreach that ensures timely payments while fostering stronger customer relationships. Bridgett Crank, Billing & Payroll Manager, highlighted this shift's impact:

"We've reduced outstanding receivables by 30% by matching collection strategies to customer patterns rather than using rigid rules. The impact on both cash flow and customer relationships has been remarkable".

For resource-constrained startups, predictive analytics helps prioritize high-risk accounts while automating workflows for low-risk ones. This not only streamlines liquidity management but also offers real-time visibility into cash flow - critical for maintaining runway and making informed growth decisions.

Lucid Financials takes this a step further by embedding predictive analytics into its AI-powered platform. With features like real-time dashboards, automated reconciliation, and Slack-based support, the platform delivers actionable insights without the hassle of complex manual setups. It ensures accurate books within seven days and produces investor-ready reports, keeping your financials up-to-date and ready for scaling. This seamless integration showcases how AI tools simplify cash flow management and empower startups to stay in control.

As Amrit Mohanty from Optimus.tech puts it:

"The question isn't whether predictive analytics improves payment cost management; research confirms it decisively does, but rather how quickly individual organizations can adopt and deploy these capabilities to secure their competitive position".

For startups aiming to grow, the time to act is now.

FAQs

What data do I need to predict late payments accurately?

To predict late payments effectively, you'll need access to historical payment data along with details like customer profiles, transaction histories, payment behaviors, amounts, timing, and other customer-specific traits. By analyzing these factors, machine learning can detect patterns and provide forecasts for future payment trends. This enables businesses to tackle potential delays head-on and maintain healthier cash flow.

How do invoice risk scores change my collections process?

Invoice risk scores help businesses collect payments more effectively by predicting how likely it is that a payment will be late or missed. These scores are built using historical data and customer behavior patterns. With this insight, businesses can prioritize which customers to contact first, use their resources more efficiently, and tackle potential payment problems before they escalate. This proactive approach transforms collections from a reactive scramble into a well-planned strategy. The result? Fewer overdue payments, improved cash flow, and more accurate financial planning - essential advantages for startups working with limited cash reserves.

How soon should I expect DSO and cash flow to improve?

You can start seeing better Days Sales Outstanding (DSO) and improved cash flow in as little as 15 to 20 days after adopting AI-driven strategies. Mid-market B2B companies have reported similar success by using automation and predictive analytics to simplify payment workflows and tackle delays before they become an issue.