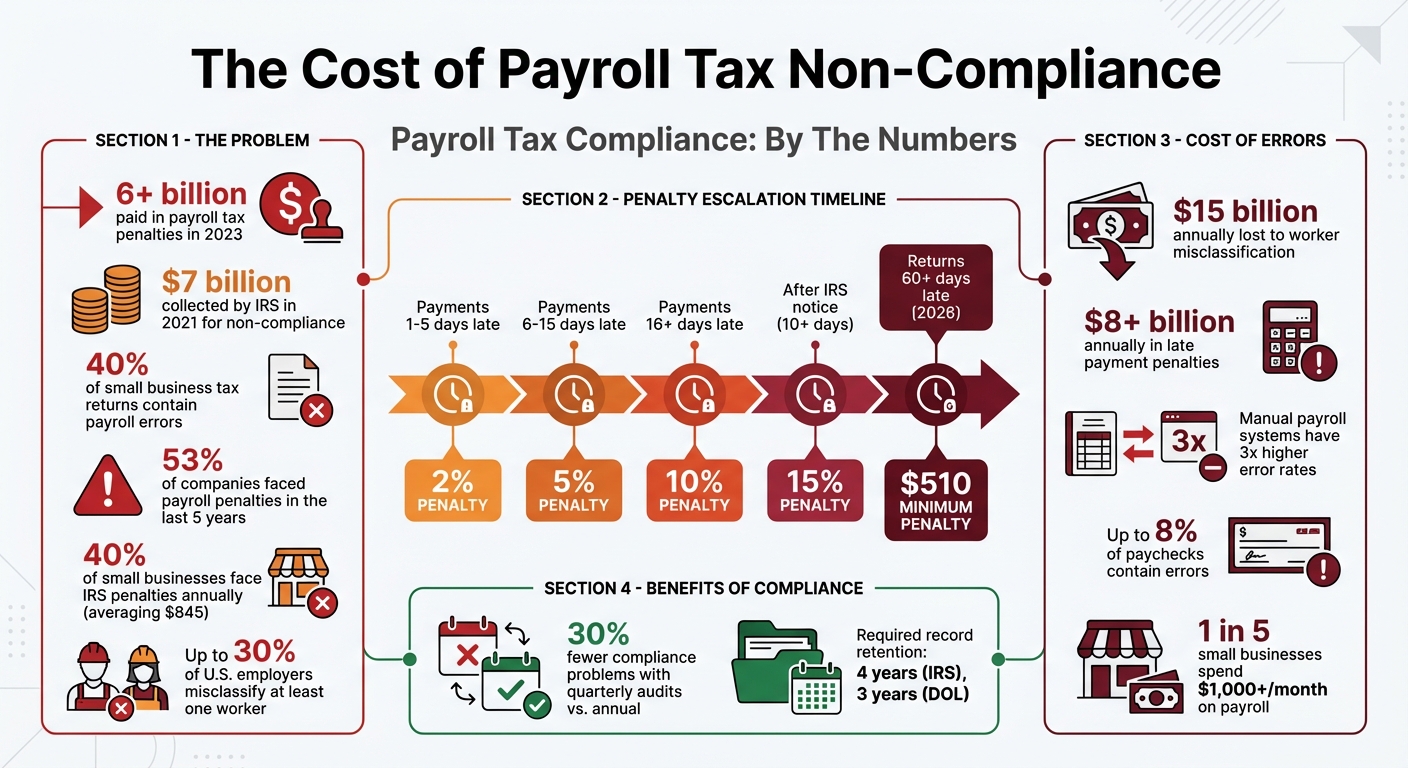

Avoiding payroll tax fines is easier than you think. With businesses paying over $6 billion in penalties in 2023, staying compliant is critical - especially for startups. Here’s a quick guide to help you:

- Conduct quarterly payroll audits to catch errors early, like misclassifications or missed deadlines.

- Organize payroll records for easy access during IRS audits (keep them for at least four years).

- Stick to filing and deposit deadlines to avoid escalating penalties (up to 15% for late payments).

- Classify employees and contractors correctly to prevent costly fines and back taxes.

- Use automation tools to handle calculations, deadlines, and compliance with ease.

- Create a tax compliance calendar to track all key dates for filings and payments.

- Claim payroll tax credits like the R&D Tax Credit to reduce your tax burden.

- Work with financial experts for audits, classification checks, and penalty relief applications.

- Reconcile payroll regularly to ensure accuracy and avoid discrepancies.

Key takeaway: Automating payroll, staying organized, and following deadlines can save your business thousands in fines - and valuable time.

Payroll Tax Compliance Statistics and Penalty Costs for Small Businesses

How to avoid payroll tax penalties with QuickBooks Online Payroll (AutoTax)

sbb-itb-17e8ec9

1. Conduct Quarterly Payroll Audits

Performing quarterly payroll audits is a smart way to catch mistakes before they lead to costly IRS penalties. Did you know that 40% of small business tax returns contain payroll errors? These often stem from simple issues like data entry mistakes or incorrect withholdings. Businesses that take the time to audit their payroll every quarter report 30% fewer compliance problems compared to those that only check once a year.

Avoiding Payroll Tax Penalties

Quarterly audits can help you identify and fix common issues that trigger IRS penalties, including worker misclassification, incorrect tax withholdings, and missed deadlines for filing Forms 941 and 940. These errors can add up quickly - misclassifying employees, for instance, costs U.S. businesses around $15 billion annually in back taxes, penalties, and interest. Catching these problems early can save you from escalating penalties, which start at 2% and can hit 15% of the unpaid amount within just 10 days of an IRS notice.

Practical for Small Teams

If your business has fewer than 100 employees, a thorough review of payroll records is manageable and ensures accuracy. To streamline the process, compare payroll registers with employment contracts, attendance records, and bank statements to find any discrepancies. Double-check that your payroll system uses the latest federal and state tax brackets. Also, separate payroll preparation and approval tasks to minimize fraud risks.

Leveraging Automation for Accuracy

Modern payroll software can make this process even smoother by automatically flagging unusual patterns, like unexpected overtime spikes. Businesses using manual payroll systems experience error rates that are three times higher than those using automated tools. Combining quarterly audits with automated exception reports can drastically reduce errors and compliance headaches.

"A structured payroll audit helps organizations identify these issues early, ensuring employees are paid correctly and tax regulations are followed." - Sarah Mitchell, Author, Payrun

2. Maintain Organized Payroll Records

Prevention of Payroll Tax Fines

Keeping payroll records organized isn’t just a good habit - it’s your first line of defense against payroll tax fines. The IRS relies on these records during audits, and without them, businesses risk hefty penalties. For example, millions in fines could have been avoided with proper documentation. Essential details to include are employee names, TINs, dates of birth, addresses, employment dates, hourly rates, gross wages, and copies of forms like W-4s, W-2s, 1099s, and Form 941. Pairing this meticulous record-keeping with regular audits can help reduce the risk of fines even further.

Ease of Implementation for Startups

The rules for retaining payroll records are fairly straightforward once understood. The IRS mandates keeping employment tax records for at least four years after the tax is due or paid. Meanwhile, the Department of Labor (DOL) requires payroll records to be held for three years, and wage computation records, such as time cards, for two years. To stay on top of this, startups can implement annual updates and detailed checklists covering employee statuses, tax jurisdictions, benefit deductions, and garnishments. Using a separate payroll bank account or subledger also simplifies tracking and prevents funds from getting mixed up. Starting with a well-structured manual system can pave the way for smoother automation later.

Automation and Compliance Support

Cloud-based payroll systems take organization to the next level by making records searchable, secure, and backed up. Integrating time-tracking software with payroll systems minimizes manual entry errors, which, according to the American Payroll Association, affect up to 8% of paychecks. Automated systems also create a clear, timestamped record trail for every payment and filing, making audits much less stressful. Secure digital storage with version control ensures you can track updates to payroll entries, keeping your records ready for any compliance checks.

Potential Cost Savings

Payroll errors can be costly. Around 40% of small businesses face IRS penalties averaging $845 annually due to payroll mistakes. Additionally, one in five small businesses in the U.S. spends over $1,000 a month managing payroll internally. Quarterly reconciliations - comparing ledgers with bank statements and tax returns - are an effective way to catch and prevent errors. Setting internal reminders at least a week before deposit and filing deadlines ensures records are updated and submitted on time. Plus, digital records can shield businesses from penalties that can climb to over $1 million for failing to file W-2 forms.

3. Follow Filing and Deposit Deadlines

Avoiding Payroll Tax Penalties

Keeping up with payroll tax deadlines is just as important as maintaining accurate records. Missing these deadlines can lead to hefty IRS penalties. In 2021 alone, businesses paid nearly $7 billion in fines for non-compliance. Penalties escalate quickly: payments that are 1–5 days late incur a 2% fee, 6–15 days late result in a 5% fee, and delays beyond 15 days rack up a 10% fee. If you miss the deadline after the IRS sends its first notice (over 10 days late), the penalty jumps to 15%. For returns filed 60+ days late in 2026, the minimum penalty will be $510 or 100% of the unpaid tax, whichever is less.

"Trust fund taxes are not the employer's money - they belong to the government and must be deposited before other obligations." - Slava Akulov, Founder of Jupid

Simplified Guidelines for Startups

Understanding your deposit schedule is key. Businesses with a tax liability under $50,000 are monthly depositors and must pay by the 15th of the following month. Those with liabilities of $50,000 or more are semi-weekly depositors, with stricter deadlines: for paydays on Wednesday through Friday, deposits are due the following Wednesday; for paydays on Saturday through Tuesday, they’re due the following Friday. New employers typically begin as monthly depositors unless they exceed the $100,000 threshold on any single day, which requires a next-day deposit. To avoid delays, enroll in the Electronic Federal Tax Payment System (EFTPS) early, as setup can take 5–7 business days.

Automation Tools for Compliance

Automated payroll systems can make compliance much easier. These platforms calculate tax liabilities and schedule deposits automatically, reducing the risk of human error. Many include compliance dashboards with alerts for upcoming deadlines and missing details. Additionally, electronic filers of Form 941 get a three-day extension, offering extra time to ensure accuracy. Modern payroll software often includes tax geolocation tools, which apply the correct federal, state, and local tax rates based on where employees work, further minimizing errors. Integration with accounting software ensures that tax liabilities are recorded directly in your ledger, streamlining processes and avoiding duplication.

Reducing Costs Through Timely Payments

Late or improper tax payments cost small businesses over $8 billion annually in penalties. To avoid this, consider maintaining a separate payroll account to prevent accidental fund use. Unpaid taxes accrue daily interest at a rate of approximately 8–9% annually as of late 2025. If your business receives its first penalty within a 36-month period, you may qualify for First-Time Penalty Abatement (FPA), which can eliminate the fine entirely. Keep an eye on large payroll events, like bonuses or commissions, that could push your liability over the $100,000 threshold and trigger next-day deposit requirements.

4. Classify Employees and Contractors Correctly

Prevention of Payroll Tax Fines

Getting worker classification right is a cornerstone of payroll compliance. Misclassifying employees as independent contractors can lead to hefty fines and other financial headaches. Why? Because when you label an employee as a contractor, you skip employer payroll taxes, benefits, and workers' compensation. This oversight compounds with every paycheck, creating a snowball effect of non-compliance. The penalties aren’t minor either - they can include 1.5% of all wages paid, 40% of the employee's share of FICA, and 100% of the employer's share of FICA taxes. And here’s a staggering stat: up to 30% of U.S. employers misclassify at least one worker, and nearly 40% of small businesses face payroll tax fines every year.

Here’s a real-world example: In March 2026, a Florida construction company misclassified 15 drywall installers as independent contractors. After a Department of Labor audit, the company ended up owing $287,000 in back taxes, penalties, and interest - plus an additional $142,000 in unpaid workers' compensation premiums. That’s a total liability of $429,000.

To determine worker status, the IRS uses a three-factor test:

- Behavioral Control: Who decides how, when, and where the work is done?

- Financial Control: Who handles business aspects like equipment and expenses?

- Relationship Type: Does the relationship include benefits, exclusivity, or a long-term commitment?

And remember, even a signed Independent Contractor Agreement won’t protect you if the actual working relationship points to employee status.

Ease of Implementation for Startups

For startups, staying compliant starts with good habits. Before paying any contractor, require a completed Form W-9 to collect their Taxpayer Identification Number for year-end reporting. For employees, collect Form W-4 during onboarding and issue a W-2 annually. For contractors earning over $2,000 in 2026, issue a Form 1099-NEC. If you’re unsure about a worker’s status, you can file IRS Form SS-8 to get an official determination.

When in doubt, it’s safer to classify workers as employees. The cost of over-classifying is far less than the potential penalties for under-classifying. By streamlining these processes, you can reduce manual errors and integrate seamlessly into modern payroll systems.

Automation and Compliance Support

Modern payroll platforms take the guesswork out of compliance. They can automate the collection of W-4s for employees and W-9s for contractors, ensuring the right forms are used from the start. Some systems even use AI to flag high-risk contractor relationships. For instance, Lucid Financials has built-in worker classification tools that calculate tax withholding for W-2 employees (covering federal income tax, 6.2% Social Security, and 1.45% Medicare). It also alerts you to potential misclassification risks before they escalate into costly audits. Its compliance dashboard tracks submitted forms and flags any missing documentation in real time.

Potential Cost Savings

Let’s break down the numbers: in 2026, hiring a $100,000/year worker as a W-2 employee costs about $127,070. This includes employer FICA, unemployment taxes, and benefits - roughly 21% more than hiring a contractor. Tempted to save by misclassifying? Think twice. The financial consequences can far outweigh the short-term savings.

If you’ve already misclassified a worker and want to fix it, the IRS offers a way out through the Voluntary Classification Settlement Program (VCSP). By participating, you could reclassify the worker with reduced penalties - potentially paying just 10% of the employment tax liability for the most recent year before an audit.

5. Build Compliance Checks into Payroll Workflows

Prevention of Payroll Tax Fines

Adding compliance checks directly into payroll workflows is a smart way to strengthen financial processes for startups. These checks can help catch issues like missing tax IDs, invalid addresses, or incorrect access codes before submitting anything to the IRS. And the stakes? They’re high. In 2021 alone, the IRS collected nearly $7 billion in penalties from businesses that didn’t meet payroll tax requirements. On top of that, over half of companies (53%) have faced payroll penalties for non-compliance in the last five years.

Some common checks include verifying whether workers are correctly classified as W-2 employees or 1099 contractors, applying the right federal, state, and local tax rates based on work locations, and keeping track of filing deadlines for Form 941 (quarterly) and Form 940 (annual). It’s also crucial to review wage and hour calculations to ensure compliance with the Fair Labor Standards Act (FLSA) and any state-specific rules, like California’s requirement for daily overtime after 8 hours.

Ease of Implementation for Startups

The good news? Startups can integrate these checks without completely overhauling their current workflows, thanks to automation. Payroll software can sync directly with HR systems, enabling seamless data sharing between platforms. Automated reminders for deposit schedules and filing deadlines provide an extra layer of security against last-minute errors.

Another helpful practice is keeping payroll tax funds in a separate bank account to avoid accidentally spending them on other business expenses. Conducting quarterly internal audits to double-check employee classifications and wage calculations can also help catch issues early - before the IRS sends any notices. These simple steps can fit naturally into existing processes, especially when paired with the benefits of automation.

Automation and Compliance Support

Automation takes a lot of the hassle out of managing compliance. Tools like compliance dashboards offer real-time alerts for missing or invalid data. Payroll systems with automated tax table updates ensure you’re always applying the latest federal, state, and local tax laws.

For instance, Lucid Financials provides a compliance dashboard that flags problems - like missing tax IDs or invalid addresses - before payroll is finalized. It also automates the generation and e-filing of forms like W-2s, 1099s, 940, and 941, reducing the risk of reporting errors. Plus, its integration with Slack makes it easy to get real-time answers and produce detailed, investor-ready reports.

Potential Cost Savings

Incorporating automated compliance checks doesn’t just save time - it can save a lot of money, too. Non-compliance penalties reached $2.8 billion in 2024. The IRS imposes tiered penalties for late payroll tax deposits, starting at 2% for payments that are 1–5 days late and climbing to 15% after an official notice is sent. Even worse, business owners can be held personally liable for failing to withhold taxes, potentially doubling the tax bill if deemed a "willful failure".

6. Use Automation Tools Like Lucid Financials

Prevention of Payroll Tax Fines

Automation tools take payroll compliance to the next level by simplifying complex processes. They handle pay calculations, tax withholdings, fund transfers, and even submit essential forms like the quarterly 941 and annual 940 automatically. Many platforms also feature real-time compliance dashboards that flag errors immediately, reducing the chance of costly mistakes. Considering businesses faced over $6 billion in payroll tax penalties in 2023 alone, these tools are invaluable. They also assist in verifying worker classifications, which can help avoid audits related to misclassification.

Ease of Implementation for Startups

Getting started with automation tools is simple, even for startups. Many platforms offer self-service onboarding, allowing employees to input their own W-4 and I-9 forms, ensuring accurate data from the beginning. Lucid Financials, for instance, integrates seamlessly with Slack to provide real-time support and keeps payroll records well-organized - essential for IRS reviews. This efficiency lets founders focus on growing their businesses rather than drowning in administrative tasks.

Automation and Compliance Support

Automation tools are constantly updated to reflect changes in federal, state, and local tax laws, eliminating errors caused by outdated information. Kathy Yakal from PCMag emphasizes the importance of such tools, stating:

"The IRS doesn't forgive payroll mistakes, but the right software can help you steer clear of them entirely."

Features like automated reminders for filing deadlines and quarterly payroll reviews ensure that small errors are caught early, reducing the likelihood of receiving IRS notices. This approach complements a broader strategy of regular audits and timely filings, strengthening overall payroll compliance.

Potential Cost Savings

By cutting down on manual errors, automation tools help businesses avoid hefty penalties and liability issues. For example, the Trust Fund Recovery Penalty for willfully unpaid taxes can equal 100% of the unpaid amount, potentially doubling the tax bill. In extreme cases, this could lead to criminal charges, fines up to $10,000, or even imprisonment for up to five years. With pricing starting at $150 per month, Lucid Financials offers an affordable solution for startups, making reliable payroll compliance within reach for even the smallest companies.

7. Create a Tax Compliance Calendar

Prevention of Payroll Tax Fines

A tax compliance calendar pulls together all federal, state, and local tax deadlines in one place, helping you avoid costly oversights. For example, quarterly Form 941 filings are due on specific dates: April 30, July 31, October 31, and January 31. Other key deadlines include annual Form 940 reports and year-end W-2 distributions. Missing these deadlines can be expensive - businesses collectively pay about $7 billion annually in payroll tax fines to the IRS. By using a tax compliance calendar alongside other tools, you ensure all deadlines are clearly visible and manageable.

Startups, in particular, face additional tax deadlines that are easy to overlook. For instance, the Delaware franchise tax is due every year on March 1, with a hefty $200 late penalty and 1.5% monthly interest for delays. Another critical deadline is the 83(b) election, which must be filed within 30 days of a stock transfer. Missing this deadline can lead to significant future tax burdens. Just like quarterly audits or automated payroll systems, a tax compliance calendar is an essential tool for avoiding these pitfalls.

Ease of Implementation for Startups

Creating a tax compliance calendar doesn’t have to be complicated. Start with IRS Publication 509 (Tax Calendars) to identify federal deadlines, then add state-specific dates based on where your business operates. Make sure to distinguish between deposit schedules and filing deadlines to minimize confusion. Also, remember that filing extensions, such as Form 7004, only extend the filing date - not the payment due date. Taxes must still be paid by the original deadline to avoid penalties and interest.

Automation and Compliance Support

Once your calendar is set up, automation can take it to the next level. Modern tools actively monitor deadlines, syncing with your bookkeeping and payroll systems to catch errors before they become problems. For example, they can flag missing quarterly filings or discrepancies in wage totals before the IRS sends a notice. These tools can also track revenue by state to create jurisdiction-specific calendars, automatically monitor contractor payments, and generate 1099-NEC forms by January. Staying ahead of these requirements helps avoid severe penalties, including personal liability for willful noncompliance.

8. Take Advantage of Payroll Tax Credits and Incentives

Prevention of Payroll Tax Fines

Payroll tax credits aren't just a way to save money - they also help ensure compliance. For example, claiming the R&D payroll tax credit requires strict documentation, which creates a clear record of your business activities for the IRS. This can be a lifesaver during an audit, reducing the chances of penalties from misclassified expenses or incorrect filings. To claim the R&D credit offset, you need to file Form 6765 with your original, timely filed income tax return. Missing this step means you won't be able to apply the credit to payroll taxes for that year. Beyond saving money, this documentation fits into larger compliance strategies, keeping your business on solid ground.

Potential Cost Savings

If you're running a startup, the Qualified Small Business (QSB) R&D Tax Credit offers a big opportunity. It allows you to offset up to $500,000 annually against the employer portion of Social Security and Medicare taxes, even if you don’t owe income taxes. To qualify, your business must have less than $5 million in gross receipts for the current year and must be no more than five years old since generating its first revenue. The process involves calculating expenses on Form 6765 and applying the credit quarterly using Form 8974, which is attached to Form 941. If you don’t use the full credit, the remaining amount carries forward indefinitely to future quarters.

Ease of Implementation for Startups

Startups without a long history of R&D spending can simplify the process by using the Alternative Simplified Credit (ASC) method. This method calculates 14% of qualified research expenses that exceed 50% of your average spending over the past three years. Additionally, businesses in the food and beverage industry can take advantage of a FICA tax credit for employer-paid taxes on employee tips by filing Form 8846. Keeping thorough payroll and project records is key to supporting your claims, especially if the IRS comes knocking.

Automation and Compliance Support

Automation tools can make this process even easier. For example, some platforms can automatically track the time your developers and engineers spend on specific projects, generating audit-ready evidence for R&D claims without the hassle of manual spreadsheets. Tools like Lucid Financials take it a step further by combining time tracking with real-time updates on tax regulations. They also use AI to identify eligible credits based on your business activities and monitor deadlines, ensuring you file Form 6765 with your annual return and Form 8974 quarterly. This eliminates the guesswork and reduces the risk of overlooking credits that could save your business up to $500,000. On top of that, these credits can help offset penalties and strengthen your overall compliance efforts.

9. Work with Expert Financial Services

Expert financial services can play a key role in helping businesses avoid payroll tax fines. They complement tools like regular audits and automation, offering specialized support to keep your payroll processes compliant and efficient.

Prevention of Payroll Tax Fines

Working with financial experts helps you stay ahead of potential compliance issues. They perform proactive audits and real-time checks to catch errors before they turn into penalties. Many providers serve as Registered Reporting Agents with the IRS, taking care of tax form preparation and filings, even as tax laws evolve. They also utilize tools like Tax Compliance Dashboards to identify mistakes - such as missing tax IDs or incorrect employee addresses - before submissions are made.

Ease of Implementation for Startups

"Smaller businesses are at much greater risk of running afoul of the IRS because they tend to manage payroll through manual processes and disconnected software" – Paycor

Startup teams, often stretched thin, can benefit significantly from expert financial services. These professionals manage complex tasks like multi-state tax withholding for remote employees and conduct regular checks on worker classifications. For startups, this means fewer administrative headaches and more time to focus on scaling. Additionally, periodic reviews from your provider ensure everything stays on track.

This setup works hand-in-hand with automation tools, creating a seamless system for maintaining compliance.

Automation and Compliance Support

Modern financial services combine the power of AI-driven automation with expert oversight. For example, Lucid Financials integrates with platforms like Slack, offering instant updates on payroll obligations. Its general ledger integration ensures payroll data and tax liabilities are always in sync with your accounting software, reducing the chance of mismatched records.

Potential Cost Savings

Expert financial services can save you money by preventing errors that could lead to hefty fines. If mistakes do occur, these professionals can assist in applying for programs like "First-Time Penalty Reduction" or "Reasonable Cause Relief", potentially reducing or even eliminating penalties. Beyond compliance, their streamlined approach can make your operations more efficient, saving time and resources in the long run.

10. Perform Regular Reconciliation and Review

Prevention of Payroll Tax Fines

Regular reconciliation is your best defense against payroll errors like withholding missteps, data entry mistakes, or worker misclassifications. By comparing your payroll registers with financial statements, bank records, and tax filings (like Forms 941 and 940), you can catch and fix issues before they lead to fines. Doing this monthly or quarterly ensures tax deposits are accurate and on time, helping you avoid penalties that range from 2% to 15% for late payments. In fact, businesses that conduct quarterly audits experience 30% fewer compliance problems compared to those that only review annually.

This process also ensures that tax deposits are submitted correctly, reducing the risk of "Failure to Deposit" penalties. It’s worth noting that in 2021, the IRS collected almost $7 billion from businesses unable to meet their payroll tax obligations.

Ease of Implementation for Startups

For startups with fewer than 100 employees, reconciling payroll is both manageable and highly beneficial. Start by gathering key documents like signed employment contracts, payroll registers, tax filings, and attendance logs. From there, verify employee master data, including legal names, tax identification numbers, and worker classifications. Cross-check gross pay against contracts and match hours worked with attendance records, paying close attention to overtime rates.

To further reduce errors, implement separation of duties - assign one person to prepare payroll and another to approve it. This simple step significantly lowers the risk of both fraud and oversight mistakes. Additionally, use variance analysis to spot irregularities in payroll expenses. For example, unexplained changes could point to phantom employees, unauthorized pay hikes, or duplicate payments. Adding automation to this process can also cut down on manual errors and make compliance easier.

Automation and Compliance Support

Modern payroll platforms can take your reconciliation efforts to the next level. Automated exception reports flag unusual transactions, like unexpected overtime spikes or odd deduction patterns. Tax Compliance Dashboards are another powerful tool, providing alerts for missing tax IDs, invalid addresses, or incorrect local tax rates based on geolocation. For example, Lucid Financials integrates seamlessly with your accounting software, syncing payroll data and tax liabilities directly through general ledger integration. This eliminates the need for manual cross-checking, which is prone to error rates three times higher than automated processes.

Potential Cost Savings

Around 40% of small businesses face IRS penalties each year, with fines averaging $845. Regular reconciliation can help you avoid these costs by catching and fixing errors early. It may even qualify you for "Reasonable Cause Relief" or the IRS's "First-Time Penalty Reduction" program. Beyond avoiding penalties, reconciliation saves time. Small business owners currently spend between 1 and 11 hours each month on manual payroll tasks. Automating this process not only reduces errors but also gives you back valuable hours to focus on growing your business.

Conclusion

Staying on top of payroll tax compliance isn’t just about avoiding fines - it’s about safeguarding your startup’s financial health and protecting personal assets. In 2023 alone, penalties for non-compliance exceeded $6 billion, compounded by growing interest rates and the risk of personal liability. Clearly, this is an area where a proactive approach is non-negotiable.

Tactics like regular audits, meticulous record-keeping, accurate worker classification, and embracing automation can make all the difference. Tools like Lucid Financials simplify this process by seamlessly integrating with your accounting systems. With features like real-time Slack support, AI-driven compliance dashboards, and audit-ready records, Lucid Financials ensures your books are clean in just seven days and always investor-ready. Plus, its early detection of discrepancies helps you avoid those dreaded last-minute surprises or IRS notices.

Getting payroll right doesn’t just keep the IRS at bay - it strengthens team trust, reassures investors, and frees up precious time to focus on scaling your business, building your product, and acquiring customers. A solid compliance foundation sets the stage for growth.

FAQs

How do I know if I’m a monthly or semi-weekly payroll tax depositor?

Your payroll tax deposit schedule is determined by your total tax liability during the IRS lookback period (for example, July 1, 2024, to June 30, 2025, for the year 2026).

- Monthly Depositor: If your total liability is $50,000 or less, you fall under the monthly depositor schedule.

- Semi-Weekly Depositor: If your liability exceeds $50,000, you must deposit on a semi-weekly basis.

There’s one more rule to keep in mind: if your federal employment taxes hit $100,000 in a single day, you’re required to deposit the entire amount by the next business day.

What payroll records should I keep in case of an IRS audit?

To get ready for an IRS audit, make sure to keep payroll records such as tax forms, payment receipts, employee information (like Social Security numbers), and wage details. The IRS mandates that these documents be retained for at least four years. Keeping these records well-organized and stored securely not only ensures compliance but also makes it easier to respond to any audit-related questions.

What should I do if I already missed a payroll tax deadline?

If you’ve missed a payroll tax deadline, it’s important to act fast to limit penalties and interest. Start by contacting the IRS right away to report the issue and arrange a payment plan. Make the missed deposit as soon as possible to help reduce fines. To avoid similar problems in the future, take a close look at your payroll processes - automation tools or regular audits can help keep things on track. If the delay happened due to circumstances beyond your control, you might even qualify for penalty relief.