Licensing is a critical step for FinTech startups aiming to operate in emerging markets. It ensures access to essential financial systems, builds trust with users, and attracts investors. However, licensing requirements vary significantly across regions, often involving high costs and complex processes. Here's what you need to know:

Key Takeaways:

- Trust and Compliance: Proper licensing builds consumer and investor confidence. For instance, Nigeria offers tax perks like a three-year income tax exemption for compliant startups.

- Varied Requirements: Licensing costs range from $30,000 in some markets to over $1.2 million in Nigeria for specific licenses.

- Approval Timelines: Licensing can take 2 months in Rwanda, but up to 8 months in South Africa.

- Regulatory Sandboxes: Countries like Kenya and Rwanda allow startups to test products under supervision before full licensing.

Common Challenges:

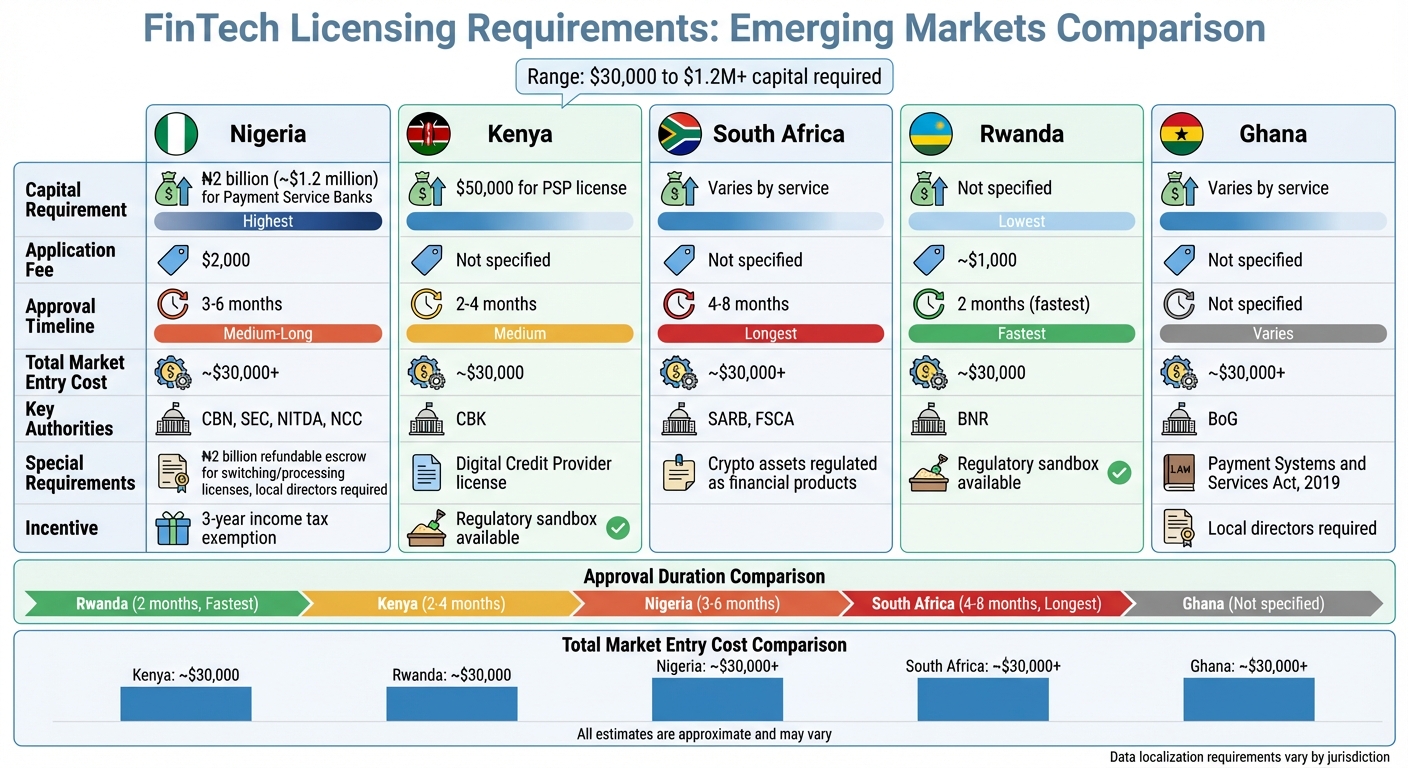

- High Capital Thresholds: Nigeria requires ₦2 billion (~$1.2 million) for Payment Service Banks.

- Service-Specific Rules: Different licenses are needed for payment processing, digital wallets, or lending services.

- Data Storage Rules: Some regions mandate local data servers, adding complexity to operations.

Actionable Advice:

- Start licensing early to avoid delays or legal risks.

- Build compliance systems into your operations from the outset.

- Leverage tools like automated AML and KYC systems to streamline processes.

- Engage local legal experts to navigate specific regulatory landscapes.

Licensing isn’t just about meeting regulations - it’s a gateway to scaling your FinTech business effectively in emerging markets.

Fintech in Emerging Markets Coursera Specialization

sbb-itb-17e8ec9

Licensing Requirements in Emerging Markets

FinTech Licensing Requirements Across Emerging Markets: Costs, Timelines & Capital Requirements

Licensing Based on Service Type

In emerging markets, licensing requirements are shaped by the specific FinTech services being provided. For instance, Payment Service Providers (PSPs) handle transaction processing, Electronic Money Issuers (EMIs) enable digital wallets, and Mobile Money Operators (MMOs) manage mobile payment platforms. There are also specialized licenses for infrastructure services like switching and processing.

Some countries have introduced unique categories to address particular needs. For example, Nigeria's Central Bank created the Payment Service Bank (PSB) license for basic banking services, which requires a capital of ₦2 billion (about $1.2 million). Kenya introduced a Digital Credit Provider license aimed specifically at lending platforms. For startups offering multiple services, Nigeria’s Payment Solution Services (PSS) license provides a flexible framework, covering processing, terminal services, and agent network operations under one umbrella.

Cryptocurrency-related services face a mixed regulatory environment. In South Africa, crypto assets are regulated as financial products under the Financial Sector Conduct Authority. In contrast, Nigeria prohibits regulated financial institutions from engaging in crypto-related activities. Some markets, like Kenya and Rwanda, offer regulatory sandboxes, enabling startups to test crypto products before committing to full licensing.

This service-specific licensing approach highlights the diverse regulatory frameworks across these markets.

Main Regulatory Authorities

Regulatory oversight in emerging markets is typically divided among specific authorities. In Nigeria, the Central Bank of Nigeria (CBN) governs payments and digital banking, while the Securities and Exchange Commission (SEC) oversees crowdfunding and crypto assets classified as securities. South Africa splits responsibilities between the South African Reserve Bank (SARB) and the Financial Sector Conduct Authority (FSCA). Kenya’s Central Bank (CBK) manages PSPs and digital credit providers, while Ghana’s Bank of Ghana (BoG) regulates EMIs and PSPs under the Payment Systems and Services Act, 2019.

Other countries have their own unique setups. Egypt’s Financial Regulatory Authority (FRA) enforces strict anti-money laundering (AML) controls. Rwanda’s National Bank (BNR) is known for its relatively fast licensing process, with approvals taking about two months. In Nigeria, FinTech companies must also work with the National Information Technology Development Agency (NITDA) for cybersecurity compliance and the Nigerian Communications Commission (NCC) for telecom-related services.

These regulatory structures reflect the broader diversity in how licensing is managed across regions.

How Licensing Rules Differ by Region

Licensing rules in emerging markets vary widely, particularly regarding capital requirements and application processes. For example, Kenya requires a minimum capital of $50,000 for a PSP license, while Nigeria sets the bar much higher at ₦2 billion for Payment Service Banks and Mobile Money Operators. Application fees also differ, ranging from around $1,000 in Rwanda to $2,000 in Nigeria, with total market entry costs - including legal and consultancy fees - often reaching $30,000 per market.

Approval timelines can vary significantly. Rwanda offers one of the fastest processes, taking about two months, while Kenya typically requires 2–4 months, Nigeria 3–6 months, and South Africa 4–8 months. Beyond licensing fees, Nigeria imposes additional requirements, such as a ₦2 billion refundable escrow payment to the Central Bank for switching and processing licenses. Most markets require local incorporation, and some - like Ghana and Nigeria - mandate having local directors or board members before granting licenses.

Data storage regulations add another layer of complexity, with some jurisdictions requiring that servers be physically located within their borders. These varied requirements highlight the need for a tailored approach when navigating licensing in different regions.

Licensing Frameworks by Region

Asia-Pacific: Digital Banking and Sandbox Programs

Singapore's Monetary Authority of Singapore (MAS) manages FinTech regulations through the Payment Services Act, Securities and Futures Act, and Financial Advisers Act. The country offers two types of digital banking licenses, including the Digital Full Bank (DFB) license, which allows for a full range of banking services. In Hong Kong, the Securities and Futures Commission (SFC) oversees digital assets, while the Hong Kong Monetary Authority (HKMA) manages virtual banking licenses.

Regulatory sandboxes play a key role in the region, offering startups a chance to test new products under temporary regulatory exemptions. This approach helps these companies refine their business models before fully entering the market.

MENA: Licensing in the Middle East

In the Middle East, digital banking adoption is widespread, with 90% of UAE residents now using digital banking channels. Saudi Arabia's Saudi Central Bank (SAMA) introduced licensing guidelines for digital-only banks in 2020, prioritizing technology and cybersecurity requirements over traditional branch-based operations. By June 2021, SAMA granted a digital banking license to STC Pay, which committed SAR 2.5 billion ($666.7 million) in capital, along with an additional $213 million.

In the UAE, startups can operate in offshore financial free zones like Dubai International Financial Centre (DIFC), regulated by the Dubai Financial Services Authority (DFSA), or Abu Dhabi Global Market (ADGM), regulated by the Financial Services Regulatory Authority (FSRA). Alternatively, they can operate on the mainland under the Central Bank of the UAE (CBUAE). The DFSA offers an Innovation Testing Licence (ITL), which allows startups a 12-month testing period with restrictions on client numbers and transaction values. In April 2024, the CBUAE introduced a Sandbox Conditions Regulation with a three-stage application process - Preliminary, Evaluation, and Decision. This framework allows innovators to test their products without full licensing, though it excludes activities like deposit-taking, insurance, and acting as a principal in certain financial products.

The UAE's 2024 Open Finance Regulation marks a shift in FinTech by requiring traditional banks and insurers to share customer data with licensed Open Finance Providers through standardized APIs. This addresses long-standing data access issues that have hindered innovation. Meanwhile, regional neobank Hala Bank secured digital banking licenses from both SAMA and the ADGM's FSRA, enabling cross-border operations. These frameworks provide a strong foundation for managing compliance across multiple jurisdictions.

Managing Cross-Border Payment Compliance

As startups expand internationally, maintaining compliance with cross-border payment regulations becomes essential. Cross-border sandboxes simplify this process by enabling reciprocal licensing arrangements, which make entering global markets easier.

"Cross-border sandboxes can allow fintech firms to benefit from streamlined licensing and reciprocal license arrangements, reducing the regulatory burden on firms looking to scale." - World Bank

To meet compliance standards, startups must ensure strict customer consent protocols and data localization measures. For instance, the UAE's Open Finance framework mandates data access through a centralized API Hub, secured with digital certificates and a Trust Framework. It explicitly bans methods like data scraping or reverse engineering. Collaborative efforts between regulators also prevent companies denied licensing in one jurisdiction from exploiting weaker oversight elsewhere. Incorporating "privacy by design" principles - such as automated consent management and revocation - further supports adherence to emerging IT governance standards.

Building Compliance Systems That Scale

Designing Products with Compliance in Mind

Startups that embed compliance into their product design from the very beginning set themselves up for fewer headaches down the road. By addressing regulatory requirements early, they can avoid expensive overhauls later. As Brandon Smith of FinTech Weekly explains:

"The ones that incorporate compliance in their technology and culture at the outset have a higher chance of success".

When designing these systems, it's smart to keep them technology-neutral so they can adapt to different regulatory environments. This is especially important in regions like Africa and Asia, where rules around data storage, licensing, and capital adequacy can vary widely. For instance, while fintechs in the EU can take advantage of PSD2 passporting rights to operate across all member states, this approach doesn’t work in regions with more localized requirements, like Nigeria or Kenya.

Beyond meeting legal obligations, a strong compliance foundation can also boost investor confidence during due diligence. This early integration of compliance helps establish clear roles and governance structures, creating a strong framework for future growth.

Assigning Compliance Responsibilities

Clear accountability is key to staying on top of regulatory requirements. Startups should assign dedicated compliance roles early in their journey. Positions like Chief Information Security Officer (CISO) and Money Laundering Reporting Officer (MLRO) are essential. The MLRO, in particular, needs the authority to take decisive actions, such as halting customer onboarding, freezing suspicious transactions, and escalating issues to the board or regulators. In some markets, like Ghana, appointing local directors is also a licensing requirement.

Compliance shouldn’t operate in isolation. Boards should receive quarterly reports on anti-money laundering (AML) and counter-terrorism financing (CFT) activities and conduct annual risk assessments at the enterprise level. For fintechs operating in multiple countries, a tri-hub governance model can be highly effective. This involves creating group-level policies and security systems in a global hub - such as London or Dubai - while tailoring data controls and settlement operations to meet local requirements. This approach balances global consistency with the flexibility needed to meet diverse regulatory demands.

By assigning clear roles and establishing strong governance, startups can lay the groundwork for technology to take their compliance efforts to the next level.

Using Technology to Manage Compliance

Technology can turn compliance from a challenge into an advantage. Automating AML and KYC processes allows startups to expand internationally without needing to scale up their compliance teams at the same rate. Tools powered by artificial intelligence can offer real-time fraud detection and transaction monitoring, while blockchain ensures secure and transparent records that simplify audits and foster trust with regulators.

Collaborating with RegTech providers can help startups keep up with ever-changing global regulations. For instance, platforms like Lucid Financials offer real-time financial data and Slack-integrated reporting, enabling founders to maintain clean, audit-ready records across jurisdictions. Additionally, implementing systems that perform daily three-way reconciliations - between internal ledgers, bank statements, and processor reports - can help exceed local compliance requirements and streamline international expansion.

Common Licensing Mistakes and Risks

When You Actually Need a License

Licensing isn’t just a bureaucratic hurdle - it’s a foundational element that can shape your product strategy, pricing, and partnerships right from the start. Unfortunately, many founders treat it as an afterthought. In some regions, such as Kenya or Nigeria, licensing is required before you even begin operations, covering activities like marketing and fundraising. The capital thresholds can be steep, ranging from $50,000 in Kenya to over ₦2 billion in Nigeria. Delaying licensing until revenue starts flowing can leave you underfunded and vulnerable to legal risks, especially if you’re operating across multiple jurisdictions.

To avoid these pitfalls, it’s important to factor in capital reserves and unexpected legal costs when setting your initial fundraising goals. Compliance systems should also be established early. Applications often fail because startups lack the necessary protocols or security standards, and fixing these issues later can be far more expensive.

Consequences of Incorrect Service Classification

In early 2025, Paystack reportedly faced a ₦250 million fine from the Central Bank of Nigeria for allegedly offering services through its "Zap" product that exceeded the scope of its license. This misstep led to strategic setbacks, increased regulatory scrutiny, and a loss of investor confidence. Mosun Oke from Tope Adebayo LP emphasizes:

"In Nigeria's increasingly scrutinized and regulated fintech landscape, having a license is no longer enough; it is about understanding what that license permits".

The risks of misclassification go beyond fines. Regulatory authorities in Nigeria have been cracking down hard on non-compliant operators. In 2023, the Central Bank of Nigeria imposed ₦1.3 billion (about $800,000) in fines on unlicensed companies, while the Securities and Exchange Commission shut down 12 unregistered investment platforms and seized ₦500 million (around $300,000) in assets. Additionally, the Federal Competition and Consumer Protection Commission removed 88 non-compliant loan apps from the Google Play Store.

These regulatory actions can lead to frozen accounts, seized assets, or even full operational shutdowns. The stakes are high: in 2023, 70% of venture capitalists prioritized regulatory compliance when assessing Nigerian fintechs, and 60% of Nigerian consumers avoided platforms with unclear licensing statuses. These numbers highlight the importance of staying vigilant with regulatory requirements.

Keeping Up with Regulatory Changes

Emerging markets are known for their rapidly changing regulatory landscapes. To stay ahead, it’s crucial to conduct regular audits and ensure that your product roadmap aligns with your license permissions. Even small changes to your offerings could breach the scope of your license.

Building relationships with regulators early can save time and headaches later. Pre-filing consultations, for example, can help you avoid delays when launching new products. Local legal experts are also invaluable - they understand regional nuances and can help navigate application processes that range from two months in Rwanda to as long as eight months in South Africa.

Stay on top of central bank circulars and commission guidelines. In Nigeria, 65% of license applications were delayed or rejected in 2024 due to errors in documentation or capital requirements. Regulatory sandboxes, like the CBN Regulatory Sandbox, can also be a useful tool. These programs allow startups to test innovative products under regulatory oversight for 6–12 months before committing to a full license. Data shows that compliant startups in emerging markets can grow their revenue up to 25% faster than those that fail to meet regulatory standards.

Conclusion

Main Lessons for FinTech Startups

Getting the right licensing isn’t just a formality - it’s a cornerstone for building trust with investors and customers alike. Without it, fintech startups face major roadblocks in scaling operations, gaining consumer confidence, and attracting investment. Regulators, especially in emerging markets, are now holding fintechs to the same strict AML (Anti-Money Laundering) and KYC (Know Your Customer) standards that banks have followed for years. As Brandon Smith from FinTech Weekly aptly notes:

"The era of fintechs enjoying comparative freedom of operation compared to banks is ending."

To stay ahead, make licensing part of your product roadmap. Plan for capital reserves, account for varying approval timelines, and budget for legal expertise. Regulatory sandboxes can also be a game-changer, letting you test your product in a controlled, compliant environment. These steps highlight the need for a seamless connection between product development and regulatory adherence.

Your Next Steps for Compliance

Navigating licensing frameworks and compliance challenges requires a proactive approach. Here’s how to set yourself up for success.

First, bring in experts who understand the local regulatory landscape. Build strong connections with regulators early by participating in pre-filing consultations and public discussions on new laws. Don’t delay setting up automated systems for AML, KYC, and transaction monitoring - waiting until you scale can lead to higher costs and complications.

Use tools like Lucid Financials to maintain clear financial oversight. These platforms simplify audit readiness, provide real-time reporting, and ensure you meet capital adequacy requirements for license applications and renewals. With features like Slack integration and access to experienced professionals, you can focus on growing your business while staying compliant with evolving regulations.

FAQs

Which license do I need for my FinTech product?

The type of license you’ll need hinges on the services your product offers and the regulations in your target market. Common options include licenses such as Electronic Money Institution (EMI), Payment Institution (PI), or specialized ones like Mobile Money Operator licenses.

In many emerging markets, some FinTech companies choose to collaborate with licensed providers. This allows them to operate legally while concentrating on scaling their business. It’s always a smart move to consult local experts to navigate regulations and meet licensing requirements effectively.

How long does licensing take in my target country?

Licensing timelines can differ significantly depending on the type of license and the regulatory process in your chosen country. The process might take as little as 3 months or stretch out to 18 months. Make sure to dive into your country’s specific requirements so you can plan your timeline effectively.

What should I budget for licensing and compliance?

Planning for expenses is crucial when pursuing licenses or meeting regulatory requirements. You’ll need to account for application fees, compliance and legal expenses, and capital requirements. Beyond these, there are ongoing costs like staffing, audits, and technology upkeep. It’s important to remember that these expenses often go beyond the initial fees and can differ depending on the jurisdiction and type of license. Make sure you're ready to handle both upfront and recurring costs to stay compliant.