If you're deciding between Incentive Stock Options (ISOs) and Non-Qualified Stock Options (NSOs) for your startup, here's the short answer:

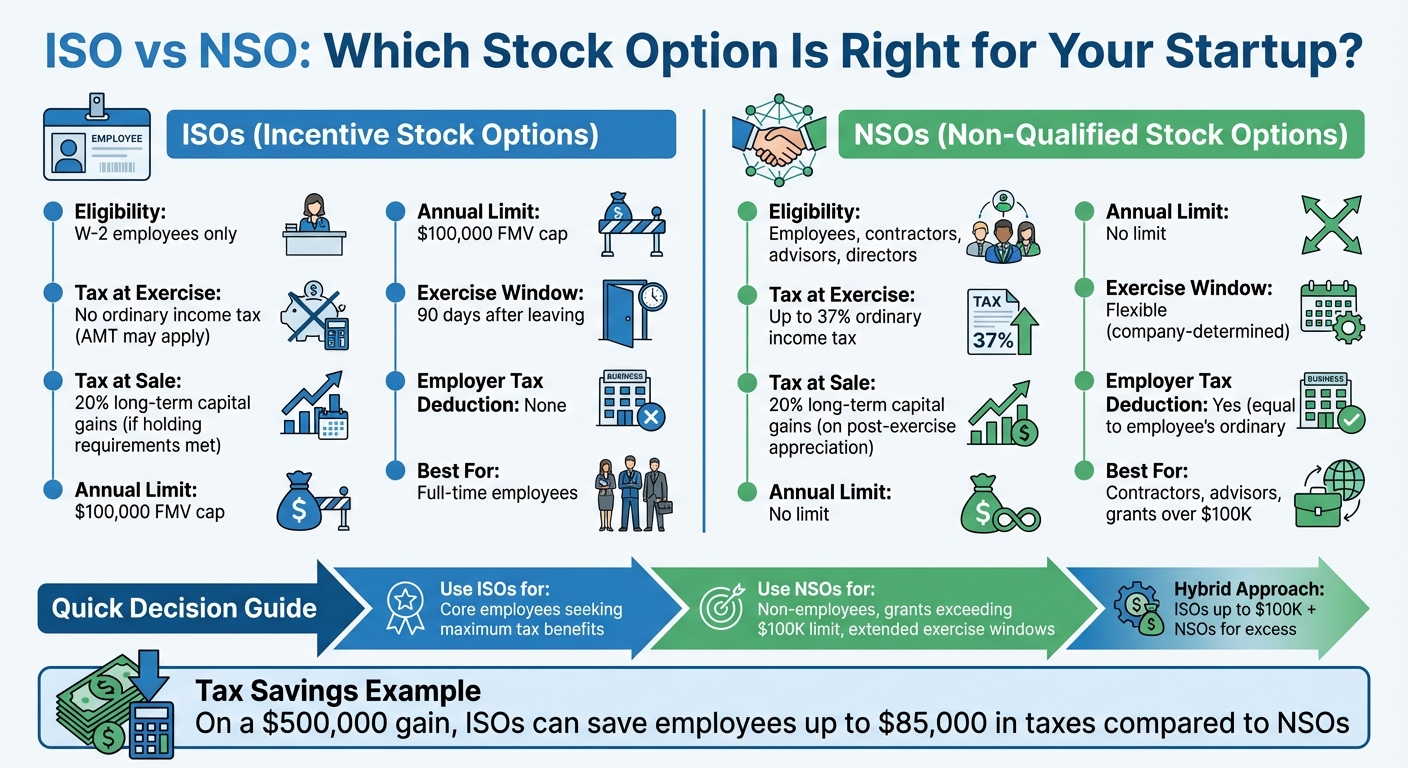

- ISOs are great for full-time employees because of their tax perks. They allow employees to pay lower long-term capital gains tax (20%) if they meet holding requirements. However, they come with strict rules, like a $100,000 annual limit and a 90-day exercise window after leaving the company.

- NSOs are more flexible. They can be granted to contractors, advisors, and non-employees, and they don't have the $100,000 limit. But they trigger ordinary income tax (up to 37%) when exercised, making them less tax-friendly for recipients.

Key Differences:

- Eligibility: ISOs are for employees only; NSOs can go to anyone providing services.

- Tax at Exercise: ISOs avoid regular income tax (but may trigger AMT); NSOs are taxed as ordinary income.

- Employer Tax Deduction: NSOs offer companies a tax deduction, ISOs generally do not.

- Exercise Window After Leaving: ISOs usually require exercise within 90 days; NSOs often allow more time.

Quick Tip: Use ISOs for employees and NSOs for contractors or excess grants beyond the $100,000 ISO limit. A hybrid approach balances tax benefits with flexibility.

Want more details? Keep reading for a deeper dive into how each type works and when to use them.

ISO vs NSO Stock Options Comparison Chart for Startups

NSO & ISO for Beginners in 3 Examples | Startup Stock Options

sbb-itb-17e8ec9

What Are Incentive Stock Options (ISOs)?

Incentive Stock Options (ISOs) are a type of employee stock option that complies with the requirements of Internal Revenue Code Section 422, offering specific tax advantages. While they come with strict rules, the benefits can be substantial. As Matt Secrist, Partner at Taft Law, puts it:

An ISO can only be granted to an employee, so there's like one restriction.

These options are limited to companies structured as C‑corporations or S‑corporations. If your company is an LLC, you’ll need to explore non-qualified stock options (NSOs) instead.

Who Qualifies and What Are the Rules

ISOs are exclusively available to W‑2 employees of the issuing company or its parent or subsidiary. Contractors, consultants, advisors, and non-employee board members are not eligible.

There’s also a $100,000 annual limit: this refers to the maximum value of stock - determined at its fair market value at the time of the grant - that can become exercisable in a single calendar year while maintaining ISO status. Any amount exceeding this limit automatically converts to NSOs. This rule can catch employees off guard, especially when cliff vesting results in a large chunk of shares vesting all at once.

For employees who own 10% or more of the company, ISOs have stricter terms: the exercise price must be at least 110% of the stock’s fair market value, and the options expire after five years. For all other employees, the exercise price must be at least 100% of fair market value, with a maximum term of ten years .

Additionally, ISOs must be granted as part of a written plan approved by shareholders within 12 months of the board adopting it.

How ISOs Are Taxed

One major advantage of ISOs is that exercising them doesn’t trigger ordinary income or payroll taxes on the spread, which means you avoid the 7.65% payroll tax. To get the full tax benefit, though, you need to meet the conditions for a qualifying disposition: holding the shares for at least two years from the grant date and one year from the exercise date. If you sell the shares before meeting these requirements (a disqualifying disposition), the spread at exercise is taxed as ordinary income.

However, there’s a catch: the spread at exercise is considered an Alternative Minimum Tax (AMT) preference item. This means employees should calculate potential AMT liabilities before exercising large amounts of ISOs to avoid unexpected tax bills. If AMT does apply, you might generate a credit that can reduce your tax burden in future years.

Downsides of ISOs

One of the biggest challenges with ISOs is the 90-day post-termination exercise window. If you leave your job, you usually have just three months to exercise your vested ISOs before they either lose their tax benefits or expire altogether.

Pinterest addressed this issue in March 2015 by allowing employees with at least two years of service to convert their ISOs to NSOs upon departure. This change extended the exercise window from 90 days to seven years.

Other limitations include the restriction to employees only, which makes ISOs unsuitable for compensating advisors or contractors - something startups often rely on. Additionally, ISOs are non-transferable except upon death, meaning you can’t gift them or use them as collateral. These restrictions can make ISOs less flexible compared to other types of stock options, leading some startups to explore alternative compensation tools.

What Are Non-Qualified Stock Options (NSOs)?

Non-Qualified Stock Options (NSOs) are a type of stock option that doesn’t meet the IRS requirements under Section 422 to qualify as Incentive Stock Options (ISOs). Essentially, NSOs are the fallback option when stock options don’t align with Section 422 guidelines. While ISOs come with specific tax perks, NSOs are more versatile and can be granted to a wider range of individuals. This makes them particularly useful for compensating non-employees. As Matt Secrist, Partner at Taft Law, puts it:

NSOs are by far the most flexible type of stock options. You can grant it to an employee and non-employee, like an independent contractor.

Like ISOs, NSOs allow the holder to purchase company shares at a predetermined strike price.

Who Can Receive NSOs

Unlike ISOs, which are limited to W-2 employees, NSOs can be issued to almost anyone providing services to a company. This includes:

- Full-time and part-time employees

- Independent contractors

- Consultants

- Strategic advisors

- Non-employee board members

Another key difference? NSOs don’t have the $100,000 annual limit on the value of shares that can become exercisable, a restriction that applies to ISOs.

This broad eligibility makes NSOs especially appealing for startups. For instance, if a startup is working with contractors, advisors, or using an Employer of Record (EOR) service to hire international talent, NSOs are the go-to option. Since workers employed through an EOR are technically not the startup’s employees, ISOs wouldn’t apply. This flexibility in eligibility also ties directly to the way NSOs are taxed.

How NSOs Are Taxed

The tax treatment of NSOs differs significantly from ISOs. While ISOs defer taxation, NSOs trigger a tax event immediately upon exercise. Here’s how it works:

- When an NSO is exercised, the spread - the difference between the fair market value at exercise and the strike price - is taxed as ordinary income.

- Employees report this spread as ordinary income on their W-2 and are subject to a 7.65% payroll tax.

- Non-employees, such as contractors, receive a 1099 and are responsible for managing quarterly tax payments.

The federal ordinary income tax rate for NSO exercises can go as high as 37%. Companies are required to withhold taxes at a minimum rate of 22% for income up to $1 million, and 37% for amounts exceeding that. Jordan Long, Marketing Lead at ESO Fund, explains:

NSOs are taxed as ordinary income when exercised, based on the difference between strike price and fair market value. They're flexible and can be granted to non-employees but usually create higher immediate taxes than ISOs.

It’s also crucial to ensure the strike price is set at or above the fair market value determined by a 409A valuation at the time of grant. Failing to meet this requirement can result in a 20% excise tax penalty and additional interest charges under Section 409A.

After the exercise, any further gains on the shares are subject to capital gains tax. The rate depends on the holding period - short-term gains are taxed at ordinary income rates, while long-term gains (for shares held over a year) are taxed at a top rate of 20%.

Benefits of NSOs

While NSOs may have higher upfront tax obligations, their structure offers several practical perks:

- No AMT concerns. NSOs don’t trigger the Alternative Minimum Tax (AMT), which can sometimes catch ISO holders by surprise. This makes the tax liability more predictable.

- Longer exercise windows. Unlike ISOs, which typically require exercise within 90 days of leaving a company to retain tax benefits, NSOs often allow for extended exercise windows. This gives individuals more time to decide without the stress of a tight deadline.

- Tax deductions for companies. When an NSO is exercised, the company gets a tax deduction equal to the amount of ordinary income reported by the recipient. This can be particularly helpful for startups looking to offset their tax burden, as ISOs don’t offer this benefit.

NSOs may not carry the same tax advantages as ISOs, but their flexibility and broader applicability make them a valuable tool for companies, especially when working with non-employees.

Main Differences Between ISOs and NSOs

ISOs and NSOs both give employees the chance to buy company stock at a set price, but they differ in terms of who qualifies, how they're taxed, and administrative rules.

Eligibility is one of the clearest distinctions. ISOs are only available to W-2 employees of the company or its parent/subsidiaries. On the other hand, NSOs can be offered to a broader group, including employees, independent contractors, consultants, advisors, and non-employee board members. This flexibility makes NSOs particularly appealing for startups that rely on contributions from both employees and non-employees.

Tax treatment is another major difference. ISOs come with tax advantages: they usually avoid regular income tax at the time of exercise (though the spread between the strike price and the fair market value might trigger the Alternative Minimum Tax). If the required holding periods are met, ISOs are taxed at the lower long-term capital gains rate, which can be as low as 20%. In contrast, NSOs are taxed at ordinary income rates - up to 37% - on the spread at exercise. Companies also benefit differently: while NSOs allow a tax deduction equal to the employee's ordinary income at exercise, ISOs generally don’t provide a deduction unless the employee makes a disqualifying disposition.

Administrative requirements set the two apart as well. ISOs must be granted under a formal plan approved by both the board and shareholders within 12 months of adoption. NSOs, on the other hand, typically require only board approval. ISOs also have a $100,000 annual limit on the fair market value of shares that can become exercisable in a given year, with any excess automatically treated as NSOs.

Another difference lies in the post-termination exercise window. To maintain ISO tax benefits, employees usually need to exercise their options within 90 days of leaving the company. NSOs, however, follow exercise rules set by the company's plan, which are often more flexible.

These distinctions play an important role in how companies manage costs and use stock options to retain talent. The table below provides a quick comparison of ISOs and NSOs.

ISOs vs NSOs: Side-by-Side Comparison

| Feature | Incentive Stock Options (ISO) | Non-Qualified Stock Options (NSO) |

|---|---|---|

| Eligible Recipients | W-2 employees only | Employees, contractors, advisors, directors |

| Tax at Grant | None | None |

| Tax at Exercise | Typically no regular income tax (AMT may apply on the spread) | Ordinary income tax (plus payroll taxes on the spread) |

| Tax at Sale | Long-term capital gains on the entire gain (if requirements met) | Capital gains on post-exercise appreciation only |

| Top Tax Rate | Approximately 20% (long-term capital gains) | Up to 37% (ordinary income) |

| Holding Period | 2 years from grant and 1 year from exercise | 1 year from exercise (for long-term capital gains treatment) |

| Employer Tax Deduction | None (unless a disqualifying disposition occurs) | Equal to the employee's ordinary income at exercise |

| Annual Limit | $100,000 FMV of shares becoming exercisable per year | No limit |

| Exercise Window After Leaving | Typically 90 days to retain ISO status | Determined by the company plan; often more flexible |

| Shareholder Approval | Required within 12 months of plan adoption | Board approval is typically sufficient |

| Employer Withholding | None required at exercise | Withholding for income and payroll taxes is required |

| IRS Reporting | Reported on Form 3921 | Reported on W-2 for employees or 1099 for contractors |

When ISOs Make Sense for Your Startup

Incentive Stock Options (ISOs) are a smart choice if you're looking to attract and retain top talent while offering them meaningful tax benefits. They are particularly effective for early-stage startups, where the strike price is low and the potential upside is high.

Using ISOs to Retain Employees

ISOs come with tax perks that encourage employees to stick around. When set up correctly, they allow employees to pay long-term capital gains tax rates - usually 0%, 15%, or 20% - on their gains instead of being taxed at ordinary income rates, which can climb as high as 37%. For example, on a 10,000-share grant with a $10 spread, employees could save over $20,000 compared to Non-Qualified Stock Options (NSOs).

"ISOs are often considered the gold standard of stock option grants because of their preferential tax treatment." - ICanPitch Blog

The 90-day exercise window also acts as a retention tool. Employees often stay with the company to maintain the favorable tax advantages. For those at pre-IPO companies, the need to secure large sums to exercise options without immediate liquidity further incentivizes them to remain until an exit event.

Early exercise options provide another advantage. Employees can purchase unvested shares when the fair market value is close to the strike price and file an 83(b) election. This locks in a low valuation for tax purposes and starts the clock on the capital gains holding period. Exercising early also reduces potential exposure to the Alternative Minimum Tax, giving employees a better chance to build wealth.

ISOs aren't just about keeping employees - they can also help your startup manage its finances more effectively.

Reducing the Need for 409A Valuations

For early-stage startups, ISOs can minimize the frequency and cost of 409A valuations. Since ISOs must be granted at fair market value, you’ll need a new 409A valuation before each grant cycle. However, by planning your grants strategically - perhaps once or twice a year - you can avoid frequent revaluations.

409A valuations can be a significant expense. Pre-revenue startups typically spend between $2,000 and $5,000 for a valuation, while Series B or later-stage companies might pay between $10,000 and $25,000. By aligning ISO grants with major milestones, such as fundraising rounds, you can control these costs while still offering competitive equity packages to your team.

When NSOs Make Sense for Your Startup

ISOs might offer appealing tax perks, but NSOs provide the kind of flexibility startups often need when granting equity. They’re especially useful when working with a diverse team or when equity needs to extend beyond the restrictions ISOs impose.

Granting Options to Contractors and Advisors

One of the standout features of NSOs is their ability to be granted to non-employees, such as contractors, consultants, advisors, and board members. For startups that lean heavily on external contributors, this is a game-changer. NSOs allow you to align these contributors’ interests with the company’s success through equity compensation.

"NSOs are by far the most flexible type of stock options. You can grant it to an employee and non-employee, like an independent contractor. An ISO can only be granted to an employee, so there's like one restriction."

– Matt Secrist, Partner, Taft Law

If your startup operates as an LLC or partnership instead of a C-corporation, NSOs are often your only option since ISOs aren’t permitted for non-C-corp entities.

This flexibility makes NSOs a practical solution when managing grants that exceed ISO limits.

Going Beyond the $100,000 ISO Limit

Under IRC Section 422(d), ISOs have a cap: only $100,000 worth (based on fair market value at the grant date) can become exercisable for the first time in a calendar year per employee. Any amount above this threshold automatically shifts to NSO treatment. For example, if you grant a VP of Engineering $250,000 in options vesting over four years with a one-year cliff, the first $100,000 qualifies as ISOs, while the remaining $150,000 is treated as NSOs.

Many startups use NSOs for larger grants or adopt a hybrid approach - maximizing ISOs up to the $100,000 limit and assigning NSOs for the excess. This strategy helps create a well-rounded equity compensation plan.

Beyond accommodating larger grants, NSOs also come with financial perks.

Taking Advantage of Tax Deductions

One major financial upside of NSOs is the tax deduction companies can claim when employees exercise them. The deduction equals the spread - the difference between the fair market value at exercise and the strike price - which matches the amount the employee reports as ordinary income. ISOs don’t offer this benefit unless there’s a disqualifying disposition. For example, if an employee exercises NSOs with a $50,000 spread, your company receives a $50,000 deduction, saving $10,500 in taxes at a 21% rate.

"From a tax perspective, this deduction often makes NSOs more attractive to companies than ISOs."

– EquityList

While managing tax withholding on NSO exercises - including ordinary income and payroll taxes - can add complexity, the corporate tax savings can be a compelling advantage for cash-flow positive companies.

Which Option Is Right for Your Startup?

Choosing the right equity structure for your startup depends on your team composition, growth stage, and financial goals. Many startups find that a combination of ISOs and NSOs works best. ISOs are ideal for full-time employees, offering tax advantages that reward and retain talent. On the other hand, NSOs provide the flexibility to compensate contractors, advisors, and handle option grants that exceed the $100,000 annual ISO limit.

For C-corporations with traditional employee structures, ISOs can save employees a significant amount in taxes - up to $85,000 on a $500,000 gain compared to NSOs. However, if your startup works with consultants, operates as an LLC, or needs to offer extended exercise windows beyond the standard 90 days, NSOs are often the better choice. For senior executives, a hybrid approach - using ISOs for the first $100,000 and NSOs for the excess - can balance compliance with tax efficiency.

Let’s take a closer look at how startups can combine ISOs and NSOs effectively.

Using Both ISOs and NSOs Together

A popular strategy for startups is to grant ISOs to employees and NSOs to non-employees like contractors, advisors, and board members. This approach allows you to offer tax-advantaged equity to your core team while compensating external contributors who don’t qualify for ISOs. For larger grants, you can allocate ISOs up to the $100,000 limit and use NSOs for the remainder. This ensures compliance with IRS rules while optimizing tax benefits for employees.

NSOs also have some strategic advantages. For instance, they allow startups to offer extended post-termination exercise windows beyond the standard 90 days, which is increasingly seen as a more employee-friendly option. Additionally, if your startup is profitable or nearing profitability, the corporate tax deduction from NSO exercises - equal to the employee’s ordinary income - can provide a financial benefit that ISOs don’t offer.

Given the complexity of these decisions, having expert guidance is essential.

Getting Help with Equity and Tax Planning from Lucid Financials

Managing equity compensation can be overwhelming, with intricate tax rules, 409A valuations, and compliance requirements. That’s where Lucid Financials comes in. Their platform combines AI-powered insights with expert financial guidance to help startups tackle challenges like structuring hybrid ISO/NSO grants, tracking the $100,000 ISO limit, or assessing potential AMT exposure for employees. With seamless Slack integration, Lucid delivers real-time insights and investor-ready reports, covering everything from NSO tax withholding to compliance with Section 422 and Section 409A.

Conclusion

Deciding between ISOs and NSOs doesn’t have to be an either-or choice for most startups. ISOs are often favored for their tax benefits - potentially reducing federal tax rates by up to 17 percentage points - and are particularly suited for full-time employees. On the other hand, NSOs offer the flexibility needed to compensate contractors and advisors while also providing valuable corporate tax deductions. By strategically combining ISOs and NSOs, startups can strike a balance between tax advantages and workforce needs.

However, ISOs come with strict rules. If these aren’t followed, employees could face steep tax liabilities, including potential AMT exposure, which might result in six-figure tax bills on paper gains. In contrast, NSOs trigger ordinary income tax at the time of exercise. As Stansbury Weaver aptly notes:

Done right, options present a huge opportunity. Done wrong, they're a fiasco.

Effectively managing equity compensation involves juggling multiple factors: tracking vesting schedules, keeping 409A valuations current, and modeling AMT scenarios. At the same time, companies must balance employee tax benefits with corporate deductions. Mismanagement in this area can lead to avoidable tax bills that run into tens of thousands of dollars. Clearly, getting this right is critical.

Navigating these complexities often requires expert help. Whether structuring initial option grants or implementing a mixed ISO/NSO strategy for a growing team, having professionals who understand tax rules and compliance can significantly reduce costs and prevent penalties. Lucid Financials combines AI-driven insights with seasoned financial advisors to help you make informed decisions, ensuring your equity compensation strategy aligns with both your team’s needs and your growth objectives.

FAQs

Can a startup switch an employee’s ISOs to NSOs later?

Yes, a startup can change an employee’s Incentive Stock Options (ISOs) to Non-Qualified Stock Options (NSOs), but it’s not a simple process. It usually involves canceling the original grant, issuing new options, and updating the stock plan, which requires approval from both the board and shareholders. Since ISOs and NSOs are subject to different tax rules and regulations, any modifications must be handled with precision to ensure compliance with legal and tax requirements.

How do I estimate AMT risk before exercising ISOs?

To gauge your potential Alternative Minimum Tax (AMT) risk when exercising Incentive Stock Options (ISOs), start by calculating the difference between the fair market value (FMV) of the stock at the time of exercise and your strike price. This difference, known as the "preference item", plays a key role in determining whether you might owe AMT.

Next, compare your projected income - including the preference item - to the AMT exemption thresholds. For 2026, these amounts are $90,100 for single filers and $140,200 for married couples filing jointly. If your income exceeds these thresholds, you could be subject to AMT.

Because AMT calculations can get tricky, it’s a good idea to consult a tax professional. They can provide tailored advice based on your financial situation and help you navigate this complex tax scenario.

What’s the best post-termination exercise window to offer?

The best post-termination exercise window varies based on the type of stock option. For Incentive Stock Options (ISOs), the standard is a 90-day window to preserve their tax advantages. Extending beyond this timeframe automatically changes them into Non-Qualified Stock Options (NSOs). On the other hand, NSOs tend to offer more flexibility, often exceeding the 90-day limit, depending on the company's policies.

Startups generally adhere to the 90-day rule for ISOs to retain their tax benefits, while NSOs can accommodate longer exercise periods without impacting their tax treatment.