Payroll tax compliance is critical for businesses, especially startups, to avoid penalties, financial loss, and reputational damage. Here's what you need to know:

- Federal Taxes: Employers must manage federal income tax withholding, Social Security, Medicare (FICA), and Federal Unemployment Tax (FUTA). For 2026, Social Security taxes apply to wages up to $184,500, while FUTA is 6.0% on the first $7,000 of wages (reduced to 0.6% with timely state payments). Employers report taxes quarterly (Form 941) and annually (Form 940).

- State & Local Taxes: State income tax withholding, State Unemployment Insurance (SUI), and local taxes vary by location. Hiring remote workers can trigger new state or local tax obligations, requiring registration before payroll begins.

- Payroll Systems: A reliable system ensures accurate filings, automates tax updates, and supports compliance across jurisdictions. Consider outsourcing payroll if managing it in-house is too complex.

- Ongoing Updates: Tax laws change yearly. Examples for 2026 include a higher Social Security wage base and new Paid Family and Medical Leave programs in states like Minnesota and Delaware.

Key Takeaway: Non-compliance risks include financial penalties, loss of employee trust, and personal liability for unpaid taxes. Use automated tools, stay informed on tax law changes, and ensure accurate filings to protect your business.

Payroll Tax Compliance for Small Businesses: Federal, State, & Local Guidelines

sbb-itb-17e8ec9

Step 1: Know Your Federal Payroll Tax Requirements

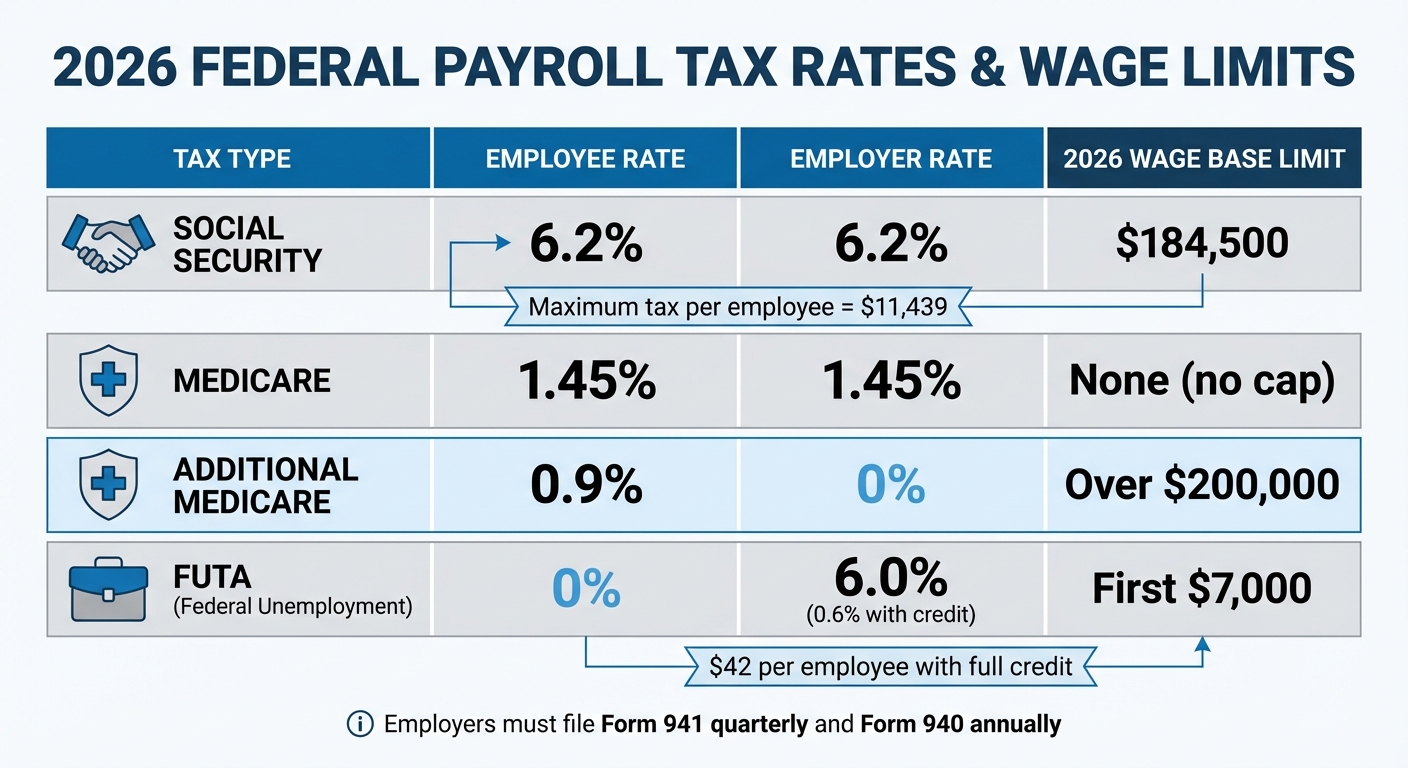

2026 Federal Payroll Tax Rates and Wage Limits Comparison

Understanding federal payroll tax requirements is a must. The IRS mandates that employers withhold and remit three primary types of payroll taxes: federal income tax, Social Security and Medicare taxes (FICA), and Federal Unemployment Tax (FUTA).

Federal Income Tax Withholding

Employers must withhold federal income tax from each paycheck based on the employee's Form W-4, which they complete upon starting their job. If an employee doesn't submit a W-4, the IRS directs employers to treat them as "Single or Married filing separately" without any adjustments.

To calculate the withholding amount, refer to IRS Publication 15-T. For manual payroll systems, use the Wage Bracket Method; if you're using payroll software, the Percentage Method might be more suitable. Supplemental wages, like bonuses or commissions, are taxed at a flat 22%, or 37% if they exceed $1 million.

Social Security and Medicare Taxes (FICA)

FICA taxes fund Social Security and Medicare and are shared equally between the employer and the employee. For 2026, the Social Security tax rate is 6.2% on wages up to $184,500. Once an employee's earnings exceed that threshold, you no longer withhold Social Security taxes for the rest of the year. The maximum Social Security tax payable per employee in 2026 is $11,439.

Medicare tax is 1.45% for both employer and employee, with no cap on wages. Additionally, you must withhold an extra 0.9% Medicare tax on wages exceeding $200,000, though employers aren't required to match this amount.

Employers must report FICA and income tax withholdings quarterly using Form 941. Payments should be made electronically through EFTPS, IRS Direct Pay, or a business tax account. Your deposit schedule - monthly or semi-weekly - depends on your total tax liability during a 12-month lookback period ending on the previous June 30.

Federal Unemployment Tax Act (FUTA)

FUTA is an employer-only tax. The standard rate is 6.0% on the first $7,000 of each employee's annual wages. However, paying state unemployment taxes on time allows you to claim a credit of up to 5.4%, effectively lowering your FUTA rate to 0.6%, or $42 per employee.

FUTA is reported annually on Form 940, but if your liability exceeds $500 in any quarter, you must make a deposit by the end of the following month. Check whether your state is a "credit reduction state", as this could reduce your FUTA credit and increase your effective tax rate.

| Tax Type | Employee Rate | Employer Rate | 2026 Wage Base Limit |

|---|---|---|---|

| Social Security | 6.2% | 6.2% | $184,500 |

| Medicare | 1.45% | 1.45% | None |

| Additional Medicare | 0.9% | 0% | Over $200,000 |

| FUTA | 0% | 6.0% (0.6% with credit) | First $7,000 |

With federal payroll tax rules in hand, the next step is tackling state and local payroll tax obligations.

Step 2: Understand State and Local Payroll Tax Rules

After getting a handle on federal payroll taxes, it's time to dive into state and local requirements. Unlike federal taxes, which are consistent nationwide, state and local payroll taxes vary depending on where your employees physically work.

The basic rule is simple: taxes are determined by the location where work is performed. For instance, hiring just one remote worker in a new state can trigger full tax obligations there. This is because most states have a zero-dollar threshold for employment tax nexus. So, if an employee works from home in Oregon, you'll need to register with Oregon's tax agencies and withhold taxes accordingly.

State Income Tax Withholding

Forty-one states and the District of Columbia require employers to withhold state income tax from employee paychecks. The nine states without income tax - Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming - don’t require withholding, which can make payroll simpler for workers in those locations.

For states that do require withholding, you’ll need to register with the state’s Department of Revenue within 15–20 days of hiring your first employee there. Each state has its own withholding tables and forms, much like the federal W-4. Tax rates vary: some states, like Illinois (4.95%) and Indiana (3.05%), have flat rates, while others, such as California (1%–13.3%) and New York (4%–10.9%), use progressive brackets. Reciprocity agreements can also make things easier. For example, an employee living in one state but working in another may only need to pay taxes to their home state, provided they file the right exemption form, like Form VA-4.

State Unemployment Insurance (SUI)

Every state requires employers to pay into State Unemployment Insurance (SUI), which provides benefits to unemployed workers. These rates differ by state and employer. For 2026, new employer rates range from 1.0% in South Carolina to 4.1% in New York.

The wage base - how much of an employee’s earnings are taxable for SUI - also varies. In California and Florida, it’s capped at $7,000, while in Washington, it’s as high as $78,200. Some states, like Oregon, recently raised their wage base; for 2026, Oregon's cap increased from $54,300 to $56,700.

Your SUI rate will change over time, depending on your experience rating, which reflects how many former employees file for unemployment benefits. SUI contributions are reported quarterly, and you’ll need to register with your state’s Department of Labor as soon as you establish nexus in that state.

Local Payroll Taxes

Fewer than 20 states have cities or counties with additional payroll taxes, but where they exist, they add another layer of compliance. These taxes typically fall into three categories:

- Income or earnings taxes: Withheld directly from employee paychecks. For example, Philadelphia taxes between 3.43% and 3.74%, depending on residency status. Other cities, like Detroit, also impose local income taxes.

- Occupational privilege taxes: Often called "head taxes", these are flat fees charged per employee, sometimes split between employer and employee. In Denver, this fee is $5.75 per employee per month.

- Transit taxes: These fund local transportation. For instance, Portland’s TriMet Transit Tax charges employers 0.8237% of wages, while New York’s Metropolitan Commuter Transportation Mobility Tax (MCTMT) ranges from 0.11% to 0.60%, depending on payroll size.

With over 5,000 local tax jurisdictions in the U.S., manually keeping track is nearly impossible. To stay compliant, map out where employees work - including hybrid arrangements - and verify local tax rules using municipal websites or automated tools.

| Local Tax Example | Location | Tax Type | Rate/Amount |

|---|---|---|---|

| MCTMT | NYC Area | Employer-paid Transit Tax | 0.11% – 0.60% |

| Occupational Privilege Tax | Denver, CO | Flat Monthly Fee | $5.75 per employee |

| Wage/Earnings Tax | Philadelphia, PA | Local Income Tax | 3.43% – 3.74% |

| TriMet Transit Tax | Portland, OR | Employer-paid Transit Tax | 0.8237% of wages |

To avoid penalties, start by mapping each employee’s work location and checking whether payroll taxes apply in that state or locality. Aim to register at least 60 days before running your first payroll in a new jurisdiction. This groundwork ensures your payroll system handles withholdings accurately and sets you up for compliance in the next step.

Step 3: Set Up a Payroll System That Supports Compliance

Once you’ve mapped out all your federal, state, and local payroll obligations, the next step is creating a payroll system that keeps you compliant. The right system doesn’t just cut paychecks - it automates tax filings, flags compliance risks, and keeps detailed records for audits. This isn’t just a nice-to-have. Payroll mistakes cost U.S. employers a staggering $7 billion annually in penalties, and more than half of companies have faced payroll penalties in the past five years. Clearly, investing in the right payroll infrastructure is a smart move.

A capable payroll system should do more than basic math. It needs to handle compliance across all 50 states and local jurisdictions with precise address-based geolocation - using ZIP codes alone isn’t enough, as they can cross tax borders. It should also automatically update tax tables (like the 2026 Social Security wage base of $184,500) and manage filings for key forms like 941 and 940, as well as state withholding, SUI, and local taxes. Automating these filings and payments is crucial since late deposits can lead to IRS penalties ranging from 2% for deposits made 1–5 days late to as much as 15% if they’re not deposited within 10 days of an IRS notice.

What to Look for in a Payroll System

When evaluating payroll systems, make sure it can handle multi-state tax complexities, including reciprocity agreements. For example, if an employee lives in New Jersey but works in Pennsylvania, the system should automatically account for the reciprocity agreement and withhold taxes only for New Jersey, provided the correct exemption form is on file. It should also flag nexus triggers that might require you to register with new state tax agencies.

Another must-have is integrated labor law tracking. This ensures compliance with state-specific rules like minimum wage increases, overtime laws, and final paycheck deadlines. With 19 states raising minimum wages in 2026 and new Paid Family and Medical Leave programs rolling out in Delaware and Minnesota, staying up-to-date is non-negotiable. Strong security features are equally important - look for SOC-2 compliance and audit trail capabilities to safeguard sensitive data like Social Security numbers and maintain detailed logs of any changes.

Lastly, seamless integration with your accounting software and HR systems can save time and reduce errors. Features like employee self-service portals, where workers can update their information and access W-2s, cut down on administrative tasks and improve data accuracy. For startups, tools like Lucid Financials (https://lucid.now) offer a streamlined solution, combining AI-powered bookkeeping and tax services with Slack integration, starting at $150/month.

Once you’ve set up your system, the next decision is whether to manage payroll in-house or outsource it for added peace of mind.

In-House vs. Outsourced Payroll: What to Consider

Deciding between in-house and outsourced payroll depends on your priorities. Managing payroll internally gives you more control and can save money upfront, but it also means your team bears the full responsibility for staying compliant. With over 11,000 tax jurisdictions in the U.S. and 40% of small businesses experiencing payroll issues each year, the risks of manual processes are high. A single payroll error can cost $291 per affected employee, and one mistake could prompt 25% of employees to consider leaving their job.

Outsourcing payroll shifts much of that compliance burden to a third-party provider. Professional Employer Organizations (PEOs) offer co-employment arrangements, sharing legal responsibility for payroll and taxes. Employer of Record (EOR) services go a step further, becoming the legal employer and taking on nearly all compliance risks. For startups scaling quickly, outsourcing can often be more cost-effective than building an internal payroll team. Considering payroll typically accounts for 50–70% of a company’s operating expenses, outsourcing allows your team to focus on growth.

Here’s a quick comparison of the options:

| Model | Best For | Compliance Responsibility | Cost Level |

|---|---|---|---|

| Payroll Software | Companies with in-house expertise and existing legal entities | Employer handles all compliance; software is a tool | Lowest |

| PEO (Professional Employer Org) | SMBs seeking shared risk and access to large-group benefits | Co-employment; shared compliance responsibility | Moderate |

| EOR (Employer of Record) | Rapid expansion into new states or countries without legal entities | EOR assumes most compliance responsibilities | Highest |

For companies operating in multiple states, it might make sense to adopt the strictest state’s rules - like California’s overtime laws or New York City’s pay transparency requirements - as a baseline to simplify compliance. No matter which route you choose, the goal is the same: accurate payroll, timely filings, and solid record-keeping to keep your business running smoothly.

Step 4: Stay Updated on Payroll Tax Law Changes

Once your payroll system is set up, keeping up with changing tax laws becomes a key responsibility. Payroll tax laws shift often - federal wage bases increase, states roll out new Paid Family and Medical Leave (PFML) programs, and local jurisdictions tweak their rates. The stakes are high: under the Trust Fund Recovery Penalty (TFRP), the IRS can hold founders and officers personally liable for 100% of unpaid payroll withholdings. These unpaid taxes are treated as money owed to employees' future benefits. As Wolf Tax explains:

"The IRS uses the Trust Fund Recovery Penalty (TFRP) to pierce the corporate veil. They view payroll taxes as money you 'stole' from your employees' future Social Security and Medicare benefits".

This risk is even greater for startups with remote teams. For instance, in 2026, 19 states raised their minimum wages, Minnesota and Delaware introduced PFML programs, and the Social Security wage base jumped by $8,400 compared to 2025. Missing these updates can lead to incorrect withholdings, which might attract IRS scrutiny.

How to Track Federal and State Updates

To stay informed, use a mix of official resources and automated tools. For federal updates, check the IRS Draft Forms page toward the end of 2025 for changes to Forms W-4 and W-2. At the state level, sign up for newsletters from labor agencies like Minnesota DEED or Maryland DOL to get updates on contribution rates and new programs. Many payroll platforms also help by automatically updating tax tables and sending alerts when laws change.

For startups managing multi-state teams, tools like the Symmetry Tax Engine can simplify compliance. This tax engine calculates payroll taxes across federal, state, and over 7,000 local jurisdictions using address-level geocoding for precise results. If you outsource payroll, confirm in writing that your vendor has updated their systems to reflect new laws. As Infiniti HR points out:

"The IRS doesn't care if your vendor was slow. You're responsible for compliance regardless".

By combining these strategies, you can stay ahead of shifting requirements and avoid compliance issues.

Annual Tax Rate and Limit Adjustments

Payroll-related limits typically reset every January 1, so it's essential to update your system at the start of each year. For 2026, the maximum Social Security tax for both employees and employers is approximately $11,439. FUTA rates generally remain at 0.6%, but in states with unpaid federal unemployment loans - like California, which is projected to have a $22.9 billion balance by the end of 2026 - a 1.2% FUTA credit reduction applies. This effectively raises the rate to 1.8% on the first $7,000 of each employee's wages.

State-specific taxes also change annually. For example, California's State Disability Insurance (SDI) rate for 2026 is 1.3%, and it now applies to all wages with no cap. Platforms like Lucid Financials can make this easier by using AI to track adjustments and notify you of upcoming changes through Slack. If you manage payroll in-house, be sure to test both common and edge-case scenarios whenever new tax tables are released. This ensures your system is ready for any updates and keeps your payroll accurate.

Step 5: Create a Payroll Tax Compliance Checklist

Managing payroll tax compliance is an ongoing responsibility that requires consistent attention throughout the year. As Patriot Software explains:

"Payroll compliance isn't a once-per-year task you can easily check off. Remaining compliant is a big job. You must make sure your business is compliant with all payroll laws year-round".

To stay on top of things, break federal and state requirements into manageable tasks that you can monitor monthly, quarterly, and annually.

Federal Compliance Checklist Items

Start by collecting Form W-4 and Form I-9 for every new hire. Each pay period, withhold federal income tax, Social Security (6.2%), and Medicare (1.45%) taxes, and match the FICA contributions. For the Federal Unemployment Tax (FUTA), pay on the first $7,000 of each employee's annual earnings. While the standard FUTA rate is 6.0%, timely state unemployment payments can reduce it to 0.6%.

Stick to your assigned deposit schedule to avoid penalties. File Form 941 quarterly (due April 30, July 31, October 31, and January 31) to report wages and taxes withheld. At the end of the year, file Form 940 for FUTA and issue W-2s to employees and the Social Security Administration by January 31. For independent contractors paid $600 or more, provide Form 1099-NEC. Be aware that late W-2 filings can result in penalties ranging from $60 per form (for up to 30 days late) to $310 per form (if filed after August 1).

Once federal compliance is addressed, shift your focus to state and local requirements.

State Compliance Checklist Items

Even having one remote worker in a new state creates a tax obligation, known as employment tax nexus, which kicks in immediately. To meet these requirements, register with three key agencies: the State Department of Revenue (for income tax), the State Department of Labor (for unemployment insurance), and a workers' compensation provider. If your business is incorporated in one state but employs workers in another, you’ll need to "foreign qualify" with the Secretary of State before registering for payroll taxes.

Plan ahead by registering for state taxes at least 60 days before running payroll in a new state. Confirm rates and details like State Unemployment Insurance (SUI) rates, taxable wage bases, and Paid Family and Medical Leave (PFML) contributions. File quarterly state income tax withholding returns and annual SUI reports according to each state's deadlines. Additionally, report new hires to the relevant state agency within 20 days to avoid penalties. For companies with employees in multiple states, quarterly audits can help ensure registrations, tax rates, and work locations are accurate. To simplify compliance, you might adopt the strictest state's standards (e.g., California’s overtime rules) as a baseline for all employees.

Integrating these tasks into your payroll system can make ongoing compliance easier. Tools like Lucid Financials offer features such as real-time alerts, automated reminders, and centralized tracking to help you stay organized.

Conclusion

The steps outlined in this guide lay the groundwork for staying on top of payroll tax responsibilities. With over 5,000 local tax jurisdictions across the U.S., plus federal and state requirements, maintaining compliance requires constant vigilance. Adding team members often means registering in new tax jurisdictions, further increasing complexity .

Mistakes in payroll taxes - whether through late filings or manual errors - can lead to severe penalties, which can hit startups especially hard . The IRS's Trust Fund Recovery Penalty even allows for personal liability for unpaid withholdings, creating significant risks for founders. As Jaime Watkins, Content Specialist at Playroll, aptly states:

"The margin for error has never been smaller, and the penalties have never been larger".

Treating payroll as part of your startup's strategic infrastructure is what sets scalable businesses apart from those bogged down by compliance issues. By automating tax calculations, organizing documentation, and conducting regular audits, payroll can shift from being a recurring headache to a system that supports growth. Staying ahead of legal updates - like the 19 state minimum wage increases scheduled for January 1, 2026 - is also critical.

Tools like Lucid Financials simplify this process by combining AI-driven automation with expert guidance. Whether it's multi-state tax registrations, real-time compliance updates, or automated filings for forms like 941, 940, W‑2s, and 1099s, Lucid takes care of the heavy lifting. With features like Slack-based support, clean books within seven days, and investor-ready reporting always available, you can focus on growing your business while knowing your payroll taxes are accurate, on time, and audit-ready.

Implementing these practices today will help you stay compliant and create a strong foundation for your startup's future.

FAQs

When do I need to register for payroll taxes in a new state?

When you hire employees or start operations in a new state, it’s essential to register for payroll taxes right away. Reach out to the state’s withholding, unemployment insurance, and local tax agencies to identify the taxes that apply and secure the necessary account numbers. Make sure everything is set up before processing payroll to remain compliant and steer clear of any penalties.

How do I handle payroll taxes for hybrid and remote employees?

To handle payroll taxes for hybrid and remote employees, start by pinpointing where each employee performs their work, as tax responsibilities typically depend on their work location. You'll need to register with the correct state tax agencies, withhold and remit taxes according to those locations, and keep detailed records of work locations. Be mindful of reciprocity agreements and nexus rules, which can affect tax obligations across state lines. Tools like Lucid Financials can help streamline the complexities of managing payroll taxes in multiple states.

What payroll records should I keep in case of an audit?

Keeping payroll records is essential for any business. These records include tax forms, payment confirmations, employee details (like Social Security numbers), and wage records. The IRS mandates that payroll tax records be stored for at least 4 years, while records related to retirement plan contributions should be kept for 6 years. Maintaining these documents not only ensures compliance with federal and state regulations but also safeguards your business in case of audits.