AI is transforming fraud detection in digital payments by analyzing vast amounts of data in milliseconds to identify suspicious activity. Here's how it works:

- Real-Time Analysis: AI evaluates transaction details, user behavior, and device data within 200 milliseconds to detect anomalies.

- Behavioral Modeling: AI learns individual customer habits, flagging unusual patterns like sudden spending spikes or transactions from unexpected locations.

- Risk Scoring: It assigns a fraud likelihood score, enabling businesses to approve, flag, or block transactions instantly.

Advanced techniques like machine learning, deep learning, and consortium-based intelligence enhance detection accuracy. These tools reduce false positives, prevent fraud before it escalates, and ensure smooth payment experiences. Businesses can implement AI by starting small, testing in "shadow mode", and gradually expanding its application while ensuring data security and compliance.

AI fraud detection is fast, precise, and scalable, making it an essential tool for combating the growing threat of digital payment fraud.

Fraud Detection with AI: Ensemble of AI Models Improve Precision & Speed

sbb-itb-17e8ec9

How AI Detects Fraud in Real-Time

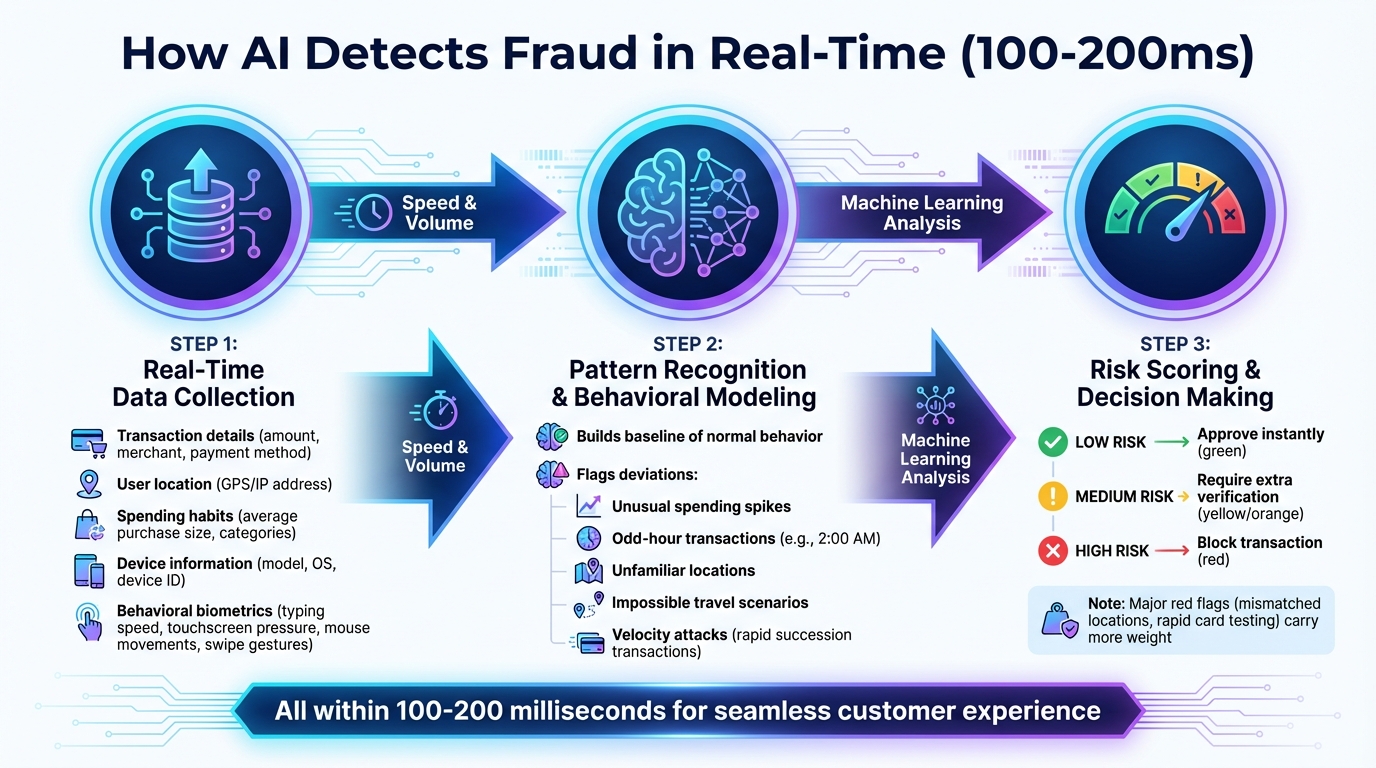

How AI Detects Fraud in Digital Payments in 3 Steps

AI fraud detection works in a matter of milliseconds, analyzing hundreds of data points as a customer waits for their payment to process. Payment systems typically have just 100–200 milliseconds to gather data, assess fraud risk, route the transaction, and secure authorization. Within this tiny window, AI determines whether to approve, flag, or decline a transaction - all while ensuring the process feels seamless for the customer. Let’s break this down into three key steps: data collection, pattern recognition, and risk assessment.

Real-Time Data Collection and Analysis

As soon as a transaction begins, AI systems gather a detailed profile. This includes transaction details (like the amount, merchant, and payment method), user location (via GPS or IP address), spending habits (such as average purchase size and preferred categories), and device information (model, operating system, and unique device ID). On top of that, advanced systems track behavioral biometrics - things like typing speed, touchscreen pressure, mouse movements, and swipe gestures - to differentiate between legitimate users and potential fraudsters, including bots or unauthorized individuals.

Pattern Recognition and Behavioral Modeling

AI builds a baseline of normal behavior for each customer by studying their typical spending habits, usual transaction times, and common locations. Any deviation from this baseline - like an unusual spending spike, a transaction at an odd hour (say, 2:00 AM), or a purchase from an unfamiliar location - raises a red flag. The system also looks for impossible travel scenarios, such as a card being used in two far-apart locations within a short timeframe, and "velocity" attacks, where multiple small transactions occur in rapid succession. These anomalies feed directly into the next step: risk scoring.

Risk Scoring for Decision Making

AI condenses all the collected signals into a single risk score that reflects the likelihood of fraud. Not all data points are treated equally - major red flags, like mismatched locations or rapid card testing, carry more weight than smaller irregularities. Businesses set thresholds based on these scores to automate decisions: low-risk transactions are approved instantly, medium-risk ones may require extra verification (like multi-factor authentication), and high-risk transactions are blocked outright. This system allows legitimate transactions to go through smoothly while stopping fraudulent attempts before any money changes hands.

Advanced AI Techniques in Fraud Prevention

Real-time detection is crucial in combating fraud, but the most advanced AI systems don't stop there - they evolve with every transaction. By continuously learning and adapting to new tactics, these systems create a smarter, more dynamic defense against fraudsters.

Machine Learning and Continuous Adaptation

Machine learning models thrive on feedback. They use data from confirmed transactions, such as those flagged by card networks and issuers, to refine their understanding of fraudulent activity. This feedback loop ensures the system stays sharp. To address model drift - where older data no longer reflects current fraud tactics - automated pipelines frequently retrain, tune, and evaluate models. Some payment processors have even tripled their model update speed to stay ahead of emerging threats.

Advanced techniques like feature engineering and embeddings allow models to recognize patterns across different contexts. For instance, if a fraud pattern emerges in Brazil, the system can detect similar activity in the U.S. without needing explicit retraining. Unsupervised learning plays a pivotal role by analyzing untagged data to uncover new, previously unseen fraud patterns. Additionally, integrating deep learning and neural networks has shown to boost fraud detection accuracy by over 20% annually compared to traditional methods.

These adaptive systems are further strengthened by shared insights through consortium-based intelligence.

Consortium-Based Intelligence

Fraudsters rarely target just one business - they often attack multiple organizations simultaneously. Consortium-based intelligence addresses this by enabling collaboration across financial institutions, payment processors, and merchants. For example, Visa's "Visa Protect" suite analyzed billions of transactions in 2023, preventing $40 billion in fraudulent activity. This shared approach ensures even smaller merchants can benefit from the security insights of larger enterprises, identifying fraudulent IPs or devices before they can strike.

The technology powering this collaboration is federated learning, which allows organizations to improve fraud detection models without compromising customer privacy. Instead of sharing raw data, institutions share model updates, enabling collective learning while safeguarding sensitive information. In 2023, the U.S. Treasury's Office of Payment Integrity used AI-driven pattern recognition to recover over $375 million in potentially fraudulent federal payments in just one year.

While consortium-based intelligence broadens the scope of insight, deep learning tackles the most intricate fraud scenarios.

Deep Learning for Complex Fraud Scenarios

Deep learning shines in detecting fraud in card-not-present (CNP) transactions, where traditional security measures like chip readers aren't applicable. Tools like Recurrent Neural Networks (RNNs) analyze transaction sequences to spot unusual spending patterns that might seem normal individually but raise red flags when viewed as a whole. Similarly, Graph Neural Networks (GNNs) map relationships between customers, merchants, IP addresses, and accounts, uncovering hidden fraud rings that reuse stolen credentials across multiple cards.

American Express has demonstrated the power of deep learning by deploying Long Short-Term Memory (LSTM) models, improving fraud detection accuracy by 6%. These models enhance traditional behavioral checks, capturing subtle account takeover attempts that might bypass password-based security. In 2023, Sift reported a staggering 427% increase in blocked account takeovers thanks to its AI-powered tools.

"The machine handles pattern recognition; the human handles context and ethics." - Krishna Kandi, Senior Software Engineer, Convoke

Benefits of AI-Driven Fraud Detection

AI's capabilities in real-time detection and adaptive learning bring practical advantages, especially for startups and growing businesses. Fraud can wreak havoc on revenue, but by leveraging AI, companies can protect themselves without the need for large, resource-heavy security teams. Here's how AI's speed, precision, and proactive monitoring create a strong shield against fraud.

Accuracy and Speed

AI systems can analyze transactions and deliver risk scores in less than 50 milliseconds - a speed no human reviewer or traditional rule-based system can match. This is crucial for maintaining the instant checkout experiences customers expect. By combining real-time activity with historical behavior, AI ensures decisions are both fast and precise.

The benefits of AI's speed go beyond customer satisfaction. Leading payment processors using AI maintain 99.9% uptime, meaning less than five minutes of downtime per year. For businesses handling thousands of transactions daily, this level of reliability directly safeguards revenue. Unlike manual methods that require scaling up staff as transaction volume increases, AI adapts automatically, offering high security without straining budgets.

Reduction in False Positives

False positives - legitimate transactions mistakenly flagged as fraud - cost U.S. retailers billions annually, often exceeding the actual losses caused by fraud. Traditional systems rely on rigid rules like "block transactions over $500", which inadvertently penalize legitimate customers making large purchases. AI, on the other hand, uses probability scores to make smarter decisions.

Major card networks have seen over a 30% reduction in false declines thanks to AI, all while improving fraud detection rates. AI leverages behavioral biometrics, such as typing speed, mouse movements, and touchscreen pressure, to verify identity seamlessly. For transactions flagged as moderately risky, AI can prompt additional verification steps - like multi-factor authentication - rather than outright declining the purchase. This approach maintains security while preserving sales.

"A model that generates a false positive by flagging a legitimate user's vacation purchase isn't necessarily a bad model; it's a model that was starved of context." - Jim Allen Wallace, Redis

Early Threat Prevention

AI doesn't just minimize errors - it actively prevents threats before they escalate. By learning each user's typical spending habits, login locations, and device usage, AI establishes behavioral baselines. Any deviation from these norms signals potential fraud. This proactive defense is critical, especially when 1 in every 120 online transactions worldwide is currently at risk of fraud.

For startups and small teams, AI's automated workflows handle routine monitoring, surfacing only high-risk cases for human review. This reduces the need for constant manual oversight. In North America, every $1 lost to fraud costs financial firms $4.41 when factoring in fees, fines, and operational expenses. By catching fraud early, AI not only blocks the initial threat but also prevents the ripple effects of additional costs.

| Feature | Rules-Based Detection | AI-Driven Detection |

|---|---|---|

| Speed | Slow; limited by human review capacity | Real-time; sub-50ms processing |

| Adaptability | Requires manual updates for new threats | Continuously learns from new data |

| False Positives | High; often blocks legitimate customers | Lower; uses context to improve accuracy |

| Scalability | Difficult to manage as volume grows | Scales easily with minimal overhead |

| Discovery | Only catches known patterns | Detects "zero-day" attacks and unknown patterns |

Implementing AI Fraud Detection for Your Business

AI has proven its value in detecting fraud with speed and precision. The challenge now is to seamlessly integrate these systems into your business operations. Fortunately, with a solid data foundation and a phased rollout, you can implement AI fraud detection without needing a massive tech team.

Key Data Requirements for AI Systems

For AI fraud detection to work effectively, the system needs accurate and relevant data. Transactional data - such as payment amounts, currency, merchant details, timestamps, and purchase frequency - is crucial. Device and context data also play a vital role, capturing details like IP addresses, geolocation, device IDs, and operating systems to understand where and how transactions happen.

Adding behavioral biometric data - patterns like typing speed, swipe gestures, navigation paths, and app usage - helps build a detailed customer profile. Historical data, including a customer’s six-month transaction history, past chargebacks, and usual login locations, allows AI to establish what "normal" behavior looks like. Network intelligence further strengthens fraud detection. For example, 90% of cards on the Stripe network have been used at least twice, enabling the system to flag cards tied to suspicious activity across merchants.

"AI isn't just a magic black box. It is a tool that has to be pointed in the direction it needs to go. Even the best fraud detection AI can only be as good as the data you give it." - Harris Nghiem, PayCompass

Steps to Integrate AI Tools

Start small. Deploy the AI model on a single high-risk product line, like digital gift cards, for 30 days to evaluate its performance before expanding further. Running the system in shadow mode initially lets the AI score transactions without affecting them, allowing you to compare its decisions against your existing rules. Feed confirmed fraud and legitimate transactions back into the model to keep it sharp and prevent it from drifting over time.

For high-value transactions, such as those over $10,000, require a human analyst to review before taking action. To ensure a smooth checkout experience, your infrastructure should support real-time processing, with risk scores generated in under 50 milliseconds. Many businesses aim for ultra-low latency, often under 10 milliseconds, to handle transactions efficiently.

| Integration Step | Actions |

|---|---|

| Data Collection | Aggregate logs from payment gateways; label historical fraud cases |

| Infrastructure | Set up live data streams; ensure scalability for traffic spikes |

| Feature Engineering | Define attributes like device fingerprint hashes and login intervals |

| Testing | Operate in shadow mode to measure precision, false positives, and latency |

| Deployment | Gradually shift traffic once AI outperforms current systems |

| Maintenance | Schedule automated retraining every 7–10 days to adapt to new tactics |

Ensuring Data Security and Privacy

Protecting customer data is critical. Ensure compliance with regulations such as PCI-DSS, GDPR (for European customers), and CCPA (for California residents). Sensitive data should always be encrypted, both in transit and at rest. Multi-factor authentication is another key layer of protection against unauthorized access.

To build trust and meet regulatory standards, use explainable AI tools that present decisions in simple, understandable terms. This transparency also allows you to audit decisions months later by implementing feature governance and versioning.

Watch for potential bias in your AI models. Avoid including protected attributes and conduct regular penetration testing to identify vulnerabilities. AI should be part of a broader defense strategy that includes encryption, behavioral biometrics, and continuous monitoring.

Conclusion

AI is reshaping the way businesses tackle payment fraud. Traditional rule-based systems struggle to keep up with modern threats like deepfakes, synthetic identities, and bot networks. In contrast, AI-powered fraud detection works at incredible speed, analyzing millions of transactions in milliseconds and spotting subtle behavioral patterns that would elude human detection.

The financial toll of fraud is immense. Beyond direct losses, false declines cost businesses approximately $118 per incident due to lost revenue and additional operational expenses. AI helps address both issues. It not only detects more fraud but also slashes false positive rates from 10–20% to under 2%.

For startups and high-growth companies, AI brings operational efficiency without the need to significantly expand fraud analyst teams. Modern AI systems can handle up to 50,000 transactions per second, all while maintaining decision latencies below 100ms. This ensures a smooth and uninterrupted checkout experience.

Adaptability is crucial in this space. As Data Scientist Raghav Sharma puts it:

"The real advantage lies in building systems that can learn, explain themselves, and improve safely over time. That is how modern payment platforms win the race that begins every time a transaction is made".

By regularly retraining AI models, businesses can stay ahead of evolving fraud tactics and prevent concept drift.

While AI excels at processing high volumes of transactions and identifying patterns, human expertise is still necessary for handling complex cases. AI can manage routine tasks efficiently, freeing fraud analysts to focus on intricate investigations and strategic risk management. This collaboration between AI and human oversight ensures both efficiency and compliance with regulatory standards.

FAQs

What data does AI use to detect payment fraud?

AI detects payment fraud by examining transaction patterns, user behavior, device specifics, geolocation, biometric data, and contextual details. By doing so, it identifies unusual or suspicious activities in real time, helping to block fraudulent transactions efficiently.

How does AI decide whether to approve or block a transaction?

AI reviews transactions by examining patterns and user behavior in real-time through machine learning. It spots irregularities such as unexpected spending, unfamiliar locations, or new devices, then assigns a risk score to each transaction. Transactions with higher risk scores might be flagged or declined, while those with lower scores are approved. Over time, the system refines its accuracy by learning from new data, which helps detect fraud more quickly and minimizes false alarms.

How can a business roll out AI fraud detection safely?

To implement AI fraud detection effectively and safely, businesses should take a structured approach. Begin by integrating advanced algorithms capable of analyzing large datasets in real time. These algorithms can identify patterns and anomalies that signal potential fraud. But technology alone isn’t enough - compliance with data privacy standards is critical to ensure sensitive information is handled responsibly.

Layered security measures, such as behavioral analytics and geolocation tracking, add extra protection by detecting unusual activities or access attempts. Start with accurate and clean data, as flawed datasets can compromise the system’s effectiveness. Regularly update AI models to stay ahead of evolving fraud tactics, which are constantly changing.

Human oversight is a key component. While AI can process massive amounts of data, human judgment ensures that decisions are fair and contextually appropriate. A phased rollout and thorough testing of the system allow businesses to identify and address potential issues early. Finally, strict adherence to regulations ensures the implementation aligns with legal and ethical standards, building trust with both customers and stakeholders.