Deciding between equity and debt can make or break your startup's future. Here's the core idea: equity gives you cash without repayment but reduces your ownership and control over time. Debt keeps your ownership intact but comes with fixed repayment obligations that could strain your cash flow.

Key Takeaways:

- Equity: No monthly payments, but you give up a share of future profits and decision-making power. Founders often lose over 70% ownership by later funding rounds.

- Debt: Retain full ownership, but you must meet fixed repayments. Interest payments are tax-deductible, lowering the cost slightly.

Quick Overview:

- Choose equity if you're early-stage, lack steady revenue, or need funding for high-risk growth.

- Opt for debt if you have predictable cash flow and need funds for proven strategies or scaling.

The best approach? Combine both - use equity for uncertainty and debt for predictable growth. Keep reading for a deeper dive into how these choices impact your business.

1. Equity Dilution

Explicit Costs

Equity financing doesn’t come with interest rates or monthly payments, but it permanently slices into your future profits and the overall value of your company. While debt has clear costs like principal and interest, equity introduces an "implicit cost" - every percentage of equity you sell reduces your ownership, even if your company’s value skyrockets later.

The earlier you raise equity, the steeper the price. For example, raising $1.5 million at a $3 million valuation means giving up a much larger ownership stake than raising the same amount at a $30 million valuation.

Liam Fairbairn, Director of Startup Banking at Silicon Valley Bank, puts it plainly: "The money you raise early on will be the most expensive money you ever take".

One analysis showed that raising $1.5 million at a $3 million valuation cost a founder $4 million more in ownership value at exit compared to using non-dilutive debt.

Equity also lacks the tax perks of debt. While interest payments on debt are tax-deductible, equity dividends and profit sharing don’t offer similar benefits. And if you ever want to buy out equity investors, it’s likely to cost far more than their initial investment.

The high cost of equity becomes even more pronounced over time as dilution stacks up with each funding round.

Long-Term Ownership Impact

Dilution adds up quickly. Founders typically lose 20% ownership during seed rounds, another 20% in Series A, 15% in Series B, and 10–15% in Series C or D. By Series B, founders often hold less than 30% of their company, while investors collectively control over 55%.

On top of that, startups usually set aside 10–20% of equity for employee stock option pools. Senior hires like a VP of Engineering might receive 1–2%, further reducing founder ownership.

These numbers emphasize the importance of aligning your funding strategy with your company’s growth stage and trajectory.

Stage-Specific Viability

Equity financing makes the most sense for startups that lack cash flow or collateral - key requirements for traditional loans. Take Amazon in 1995: the company raised $8 million in equity despite generating $20,000 in weekly sales. At the time, the internet was still unproven, making debt financing too risky for building the infrastructure Amazon needed.

Equity is also a go-to choice when you’re betting big on unproven technologies or entering uncertain markets. For instance, Trade Republic raised a $900 million Series C at a $5.3 billion valuation in 2021 to fund its rapid expansion across Europe. Debt wouldn’t have supported such aggressive scaling.

Viktor Ilijev, Chief Pitcherman at Viktori, explains: "Equity can be fuel, but only if you're already built like a racecar. If you're still tuning the engine, debt gives you space to get it right before scaling".

Control and Flexibility

Selling equity doesn’t just reduce your share of future profits - it also chips away at your decision-making power. Unlike debt, which comes with fixed repayment terms, equity often means giving investors significant control. This can include board seats, veto rights on major decisions, and influence over future funding rounds. In some cases, founders are even pushed out of leadership or forced into premature exits.

Christopher Helm, CEO of Helm & Nagel GmbH, cautions: "What I see too often: founders raise early, get diluted fast, and end up with 10 people on their cap table and no leverage".

Be wary of clauses like advanced pro-rata rights, which let investors increase their stake in future rounds and can discourage new investors. Before signing any agreements, use tools like Carta or AngelCalc to model how dilution will play out over multiple funding rounds.

While equity financing offers flexibility - there’s no mandatory repayment and risk is shared - it comes with the trade-off of giving up significant control and a large slice of your company’s future value.

sbb-itb-17e8ec9

2. Debt Financing

Explicit Costs

Debt financing comes with upfront costs that are easy to calculate: interest payments, arrangement fees, and sometimes early repayment penalties. Unlike equity, where the cost is tied to future profits, debt's expenses are clear from the start. For instance, borrowing $40,000 at a 10% interest rate means you'll pay $4,000 annually in interest.

One advantage of debt is the tax-deductibility of interest payments. This "tax shield" reduces your taxable income, making debt appear cheaper compared to equity, where you share profits indefinitely.

Before committing to a loan, it's essential to stress-test your financial forecasts. What happens if your revenue drops by 30% - can you still cover the payments? Also, don’t overlook hidden costs like arrangement fees or personal guarantees. These factors can significantly influence both your short-term cash flow and long-term ownership structure.

Long-Term Ownership Impact

One major perk of debt financing is that you retain full ownership of your company. There’s no need to sell shares, so your stake remains intact. Once the loan is repaid, your obligation ends.

Take Tesla, for example. In 2014, the company issued $2 billion in convertible notes to fund its growth, postponing share dilution until a specific stock price was reached. Similarly, Netflix used long-term bonds in 2018 and 2019 to finance its content library, maintaining shareholder value while managing cash flow. Another case is Cloud86, which secured $1.2 million in debt from re:cap to fund customer acquisition while keeping full ownership.

However, debt does create a fixed obligation. Missing payments can lead to asset seizure or even bankruptcy. Equity investors, on the other hand, share the risk - if the business fails, there’s no repayment.

Stage-Specific Viability

Debt financing is most effective when your business has predictable cash flow. Early-stage startups, especially those without revenue, often struggle to secure loans because lenders need assurance of regular payments. Debt is better suited for growth-stage companies with steady revenue or tangible assets to offer as collateral.

Jared Sorensen, CEO and finance expert, explains: "Use equity to fund uncertainty and potential, and use debt to fund certainty and execution".

Debt works well for investments with clear returns, like buying equipment, financing confirmed inventory orders, or scaling a proven sales team. Equity, on the other hand, is better reserved for high-risk initiatives such as research and development or entering untested markets. This approach allows businesses to leverage predictable cash flow while minimizing the ownership dilution tied to equity financing.

Control and Flexibility

Debt financing allows you to maintain full control over your business decisions, as lenders don’t typically demand board seats or voting rights. However, this autonomy isn’t without limits. Loan agreements often include covenants - conditions like maintaining specific debt-to-equity ratios or minimum cash balances. Failing to meet these requirements can lead to immediate repayment demands.

Be sure to review all covenants carefully before signing. Some venture debt deals may include warrants, which give lenders the option to buy a small equity stake at a predetermined price. While this introduces minor dilution, it’s usually far less than what you’d face in a full equity round. These features highlight the trade-offs between debt financing and equity dilution, helping you make an informed choice.

Equity Financing vs. Debt Financing: Which is Better for Your Business?

Pros and Cons

Equity vs Debt Financing: Cost, Ownership, and Control Comparison

When deciding between equity and debt to shape your capital structure, it’s important to weigh the advantages and disadvantages of each option. The choice boils down to what aligns best with your startup’s stage and objectives, as both routes impact cash flow, ownership, and control differently.

Here’s a breakdown of how equity dilution and debt financing compare across key factors:

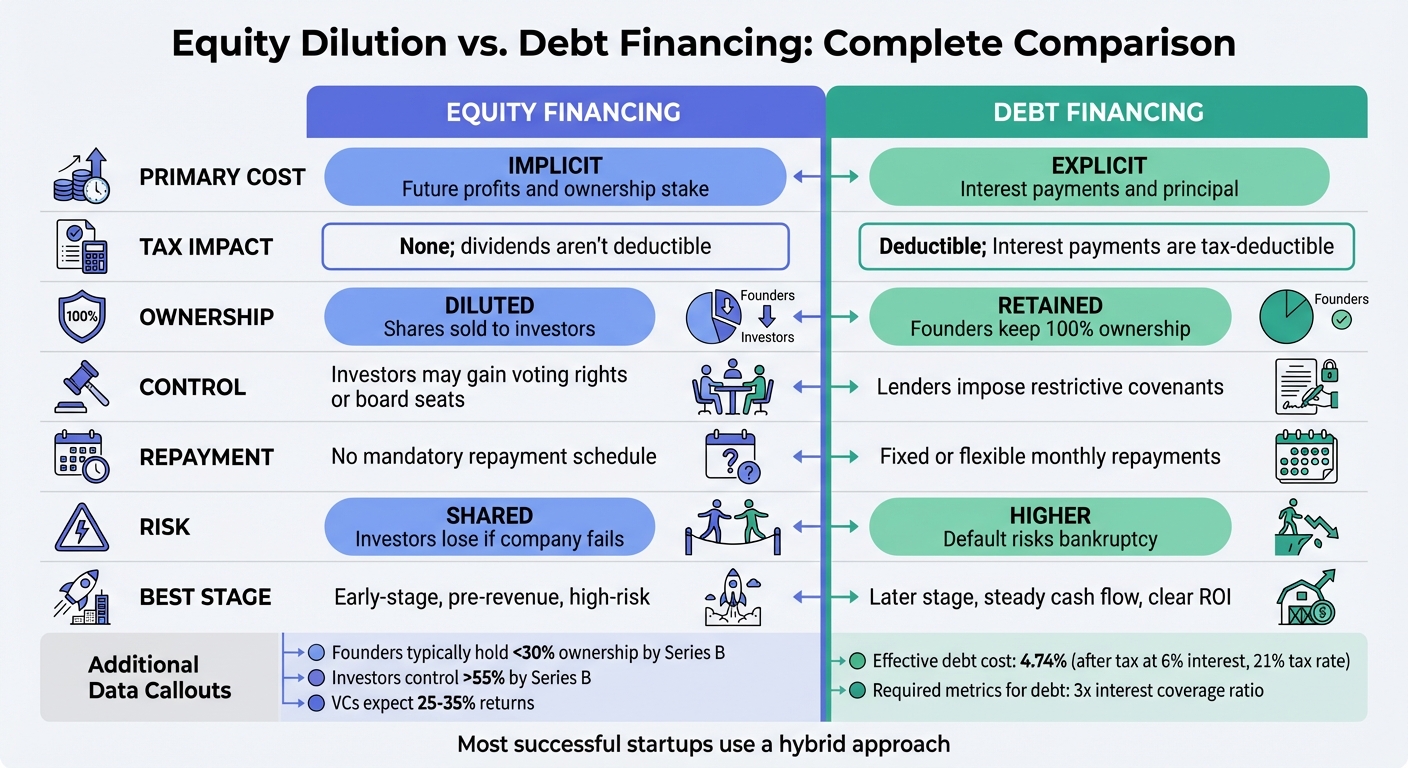

| Factor | Equity Dilution | Debt Financing |

|---|---|---|

| Primary Cost | Implicit: Future profits and ownership stake | Explicit: Interest payments and principal |

| Tax Impact | None; dividends aren’t deductible | Interest payments are tax-deductible |

| Ownership | Diluted; shares sold to investors | Retained; founders keep 100% ownership |

| Control | Investors may gain voting rights or board seats | Lenders impose restrictive covenants |

| Repayment | No mandatory repayment schedule | Fixed or flexible monthly repayments |

| Risk | Shared; investors lose if the company fails | Higher; default risks bankruptcy |

| Best Stage | Early-stage, pre-revenue, high-risk | Later stage, steady cash flow, clear ROI |

This comparison highlights how each option influences your startup’s financial health and governance over time.

Equity financing is often favored in the early stages when cash flow is unpredictable. It provides flexibility but comes at the cost of reducing your future profit share. Venture capitalists usually seek returns of 25% to 35%, so they expect significant growth to justify their investment. On the other hand, debt financing allows you to retain ownership but demands disciplined financial management. For instance, with a 6% interest rate and a 21% corporate tax rate, the effective cost of debt drops to about 4.74% after tax deductions. However, lenders typically require you to maintain an interest coverage ratio of at least 3x and a net leverage ratio of 3x or less. Failing to meet these benchmarks can trigger loan covenants.

"Use equity to fund uncertainty and potential, and use debt to fund certainty and execution." - Jared Sorensen, CFO, Preferred CFO

Understanding these trade-offs helps you navigate the challenges of finding the right financing mix for your business.

Conclusion

Deciding between equity and debt plays a critical role in shaping your capital structure. The right choice depends on your startup's current stage, cash flow stability, and how much control you're willing to share.

Debt can be cheaper in the long term because interest is tax-deductible, and you retain full ownership. For instance, with a 6% interest rate and a 21% corporate tax rate, the effective cost of debt could drop to just 4.74%. However, debt comes with fixed repayment obligations, which can put your business at risk if cash flow becomes unpredictable.

On the other hand, equity offers flexibility but comes at a higher cost over time. Instead of requiring monthly payments, equity involves giving up a portion of future profits. This makes it a better fit for startups without steady cash flow. By the time a company reaches Series B funding, founders typically hold less than 30% ownership, while investors control over 55%. Equity capital allows for shared risk and patience during uncertain stages of growth.

If your business has reliable cash flow and an interest coverage ratio of at least 3x, debt might be a practical option for scaling. However, if you're still testing your business model or need significant funding for rapid expansion, equity provides the resources without immediate repayment pressure. Many successful startups blend both approaches - using equity to navigate uncertainty and debt to fuel proven strategies.

Regardless of the choice, it’s essential to stress-test your financial assumptions. For example, model scenarios like a 30% drop in revenue to evaluate your ability to meet debt obligations. Simultaneously, assess how much equity you’re willing to part with. The best option isn’t about choosing one over the other - it’s about aligning the financing strategy with your business's current position and future goals.

To make these decisions effectively, having real-time financial insights is crucial. Lucid Financials (https://lucid.now) provides an all-in-one platform that integrates bookkeeping, tax services, and CFO support. With features like investor-ready reporting and Slack integration, you can confidently evaluate and optimize your capital structure.

FAQs

How do I estimate the real cost of equity dilution over time?

To get a handle on the cost of equity dilution over time, tools like equity dilution calculators can be a big help. These tools let you figure out how ownership percentages shift with each funding round. All you have to do is input details like the number of new shares issued and the total shares outstanding to see the impact.

Knowing the usual dilution rates for different funding stages - like 15-25% for seed rounds - can also give you a clearer picture. This understanding allows you to plan ahead, balancing the need for growth with the goal of retaining ownership.

When is my startup “cash-flow stable enough” to take on debt?

Your startup is considered "cash-flow stable enough" to manage debt when it has steady revenue, well-managed expenses, and a predictable cash flow that can handle loan repayments without strain. In simpler terms, your income consistently outweighs your expenses, minimizing the chance of running into financial trouble.

How do I decide the right mix of equity and debt for my stage?

Choosing the right mix of equity and debt depends on your startup's stage, cash flow, and objectives. Early-stage startups often lean toward equity to maintain flexibility, while businesses with steady revenue streams may opt for debt to retain ownership. Carefully weigh your options - whether it's debt, equity, or a combination - by considering factors like cash flow, ownership dilution, and risk tolerance. Make sure your choice aligns with your long-term vision. Tools like Lucid Financials can simplify these decisions and keep you on track.