Dynamic credit risk models are transforming how fast-growing startups secure funding. Unlike slower, manual methods, these AI-powered systems use real-time data to deliver faster, more accurate decisions. Here’s why they matter:

- Speed: Decisions take seconds, not days or weeks.

- Data Variety: Includes non-traditional sources like smartphone activity and e-commerce behavior.

- Accuracy: Predictive scores range from 0.80–0.90 ROC AUC, outperforming older methods.

- Better Outcomes: Reduced default rates (up to 30%) and faster loan approvals (up to 60%).

For startups, these systems are a game-changer, offering quicker access to capital and better financial insights. Though implementation can be complex, the benefits of speed, precision, and flexibility outweigh the challenges.

Multi-Agent Systems for Credit Risk Assessment

sbb-itb-17e8ec9

1. Dynamic Credit Risk Assessment

Traditional credit assessments often fall short in addressing the fast-paced needs of modern lending. Dynamic models, powered by AI and machine learning, offer a more agile and precise alternative.

Dynamic credit risk assessment evaluates borrower data in real time, delivering up-to-date creditworthiness scores. Unlike static methods that rely on fixed snapshots, these systems analyze thousands of data points simultaneously, enabling lending decisions in just seconds.

Data Sources

Dynamic models draw from a wide range of data sources, including non-traditional ones. These alternative inputs, such as behavioral and smartphone activity data, complement conventional credit scores and income statements. This approach is particularly helpful for startups or individuals with limited credit histories.

In 2023, a Southeast Asian bank adopted Credolab's machine learning–based scoring system, which utilized anonymized smartphone activity and behavioral signals. As a result, the bank reduced default rates by 30% and cut loan approval times by 60%, making it easier to set precise credit limits and onboard applicants with thin credit files.

Update Frequency

One of the key advantages of dynamic models is their ability to continuously monitor borrower behavior and market trends. By incorporating new data as it becomes available, these systems improve predictive accuracy by about 1% each month . This constant recalibration not only enhances risk scoring but also provides timely fraud alerts.

Decision Speed

AI-driven systems process loan applications within seconds by analyzing vast amounts of data. This eliminates the need for manual verification, making the process faster and more efficient . Machine learning enables these systems to assess smartphone data and real-time behavioral patterns, streamlining credit decisions.

FinTech startup MicroCredit used an AI-powered credit risk model to approve previously unscorable applicants, lower processing costs, and reduce defaults. These advancements played a role in securing its Series C funding.

This speed is crucial for startups, where agility and quick decision-making are essential.

Startup Suitability

Dynamic credit risk assessments are particularly beneficial for fast-growing startups. These systems can handle large volumes of data and adapt to rapid changes in revenue and operations .

CreditVidya, an Indian company, improved loan approval rates by 25% and reduced delinquency rates by 33% by leveraging behavioral and mobile data.

Additionally, platforms like Lucid Financials are designed specifically for startups, providing real-time financial insights and supporting scalable decision-making processes. This makes dynamic credit risk assessment a powerful tool for businesses navigating rapid growth.

2. Static and Manual Credit Risk Models

Static and manual credit risk models take a more traditional and slower approach compared to dynamic models. These methods rely heavily on historical financial records, such as annual tax filings, periodic bookkeeping, and quarterly financial statements, to evaluate creditworthiness.

Data Sources

These models depend on documents like balance sheets, income statements, and cash flow statements. However, for startups with limited financial history - often less than a year - this presents a major hurdle. Tracy Mitchell, CBA and AR senior team lead at Trinity Logistics, highlights this issue:

For a startup or a newly formed business, we're looking at less than a year in business or less than a year of financial data.

This lack of data makes it nearly impossible to generate accurate credit scores using these traditional methods.

Update Frequency

One of the key drawbacks of manual models is their infrequent updates. Data is typically reviewed on a quarterly or semi-annual basis. For fast-growing startups, this delay creates a significant blind spot, as burn rates can deplete liquidity between reporting periods. The manual reconciliation process adds further delays, slowing down critical financial decisions.

Decision Speed

Manual credit risk assessments are notoriously slow and labor-intensive. Zolvo describes the outdated nature of these processes:

Commercial lenders manage billions in assets but service their loans like it's 2005: spreadsheets, legacy software, and teams of people doing manual reconciliation all day.

While AI-driven tools can process financial data up to 100 times faster than these methods, manual systems require human verification at every step. This extends decision-making timelines from mere seconds to days or even weeks, which is far too slow for startups that need quick and agile responses.

Startup Suitability

For startups experiencing rapid growth, static models often fall short. The manual nature of these processes can overwhelm founders, increasing the likelihood of missing crucial financial details. Without real-time insights into metrics like burn rate and runway, startups lack the clarity needed to make informed decisions during critical growth phases. Additionally, the inability to quickly model various financial scenarios - such as best- and worst-case projections - further limits strategic planning. Considering that 20% of new businesses fail within their first two years and 45% fail within five years, the delayed insights from static models can have serious consequences.

Advantages and Disadvantages

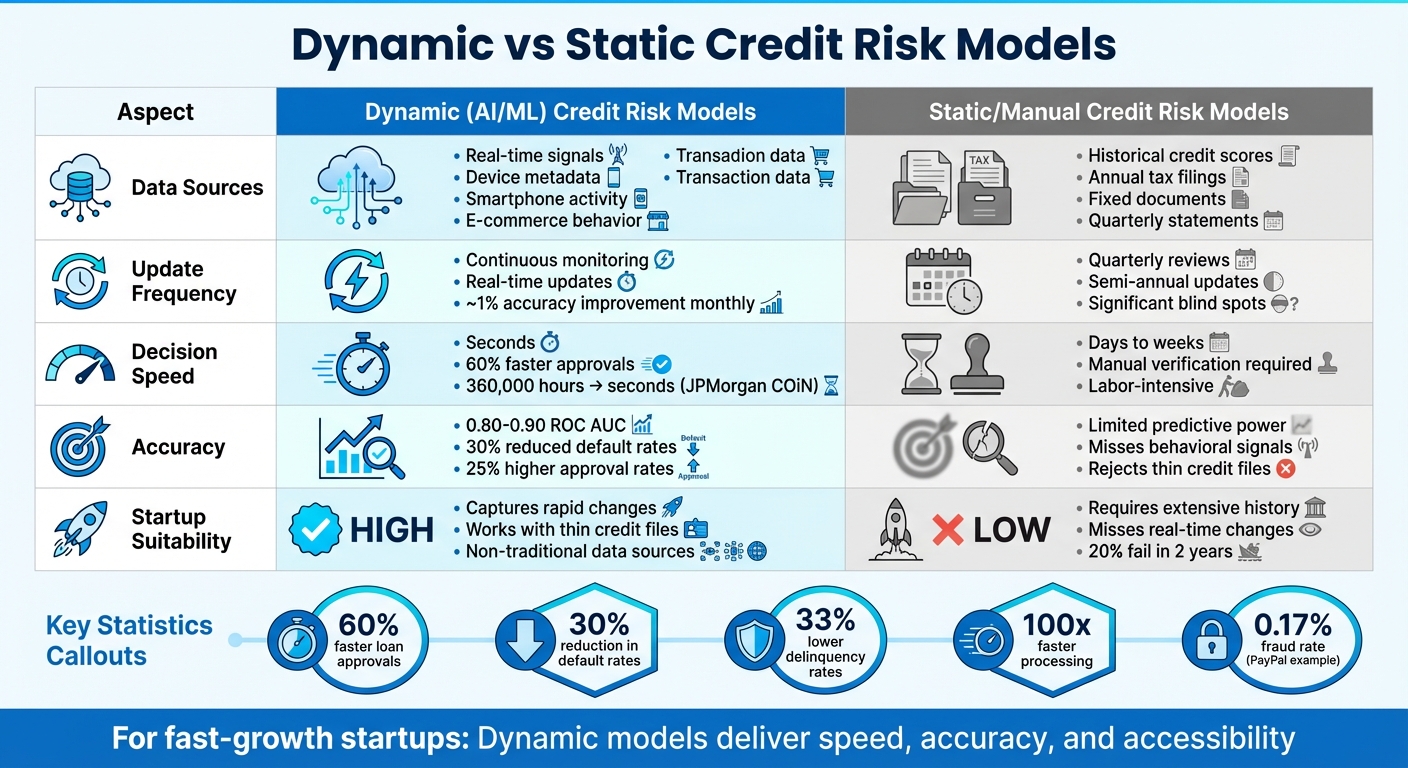

Dynamic vs Static Credit Risk Models Comparison for Startups

Dynamic systems thrive on real-time data, such as smartphone usage, digital wallet activity, and behavioral metadata. In contrast, static models depend on outdated annual credit reports, while manual methods rely on limited bank data. These differences directly address the challenges startups face when seeking funding.

The speed advantage of dynamic systems is hard to ignore. For instance, JPMorgan Chase's COiN platform reduced the time needed to review commercial credit contracts from 360,000 hours annually to just seconds. Similarly, a Southeast Asian bank using machine learning for credit scoring slashed loan approval times by 60% and cut default rates by 30%. On the other hand, manual processes often drag on for days or even weeks due to the need for human verification.

Dynamic models also shine when evaluating startups with limited credit history. Unlike static models, which might reject such applications outright, these systems use a broader range of data to make informed decisions. CreditVidya’s success with dynamic scoring further highlights how non-traditional data sources can overcome the limitations of static assessments.

To better understand the differences, here’s a comparison of the key aspects:

| Aspect | Dynamic (AI/ML) | Static/Manual |

|---|---|---|

| Data Sources | Real-time signals, device metadata, transactions | Historical credit scores, fixed documents |

| Update Frequency | Continuous, real-time monitoring | Periodic updates (quarterly or annual) |

| Decision Speed | Seconds (e.g., 60% faster approvals) | Days to weeks |

| Startup Suitability | High (captures rapid changes, thin credit files) | Low (misses non-traditional data) |

For startups, the benefits are clear: faster, more reliable funding decisions that align with their rapid growth and evolving needs.

But there are tradeoffs. Dynamic models can be complex to implement, requiring robust data quality and careful attention to privacy concerns. In contrast, static and manual approaches are simpler and more transparent but fail to capture the behavioral insights that often signal a startup's potential success. This contrast highlights why dynamic systems are particularly suited for fast-growing startups looking to stay competitive.

How Fast-Growth Startups Benefit

Real-time insights give founders the ability to tweak strategies on the fly, making decisions that can stretch their runway without waiting for the next monthly report. In a fast-paced, competitive market, this kind of immediate visibility can make all the difference.

Continuous monitoring pairs seamlessly with dynamic models to fine-tune cash flow management. For example, instead of relying on rigid monthly payments that can create large gaps in working capital, platforms like Lucid Financials introduce daily repayment adjustments. These micro-deductions, taken directly from digital wallets, sync up with daily earnings. This approach keeps cash flow steady and avoids the financial crunches that can threaten fast-growing startups.

AI-powered portfolio monitoring is another game-changer, slashing financial processing times by up to 100x. This allows startups to compare scenarios quickly and refine their growth strategies more effectively. Startup leaders have praised these tools for their impact:

Lucid's CFO services give us the visibility we need, while their bookkeeping and tax support keep everything accurate and stress-free. It's been a game-changer for our operations.

Risk-based pricing also benefits from real-time data. Lenders can better assess creditworthiness, offering stronger terms to startups with solid fundamentals - even if they lack an extensive credit history. At the same time, enhanced fraud detection protects both lenders and borrowers, reducing default rates and bad debt. These improvements make it easier for startups to secure competitive financial terms.

In addition to better risk scoring, platforms like Lucid Financials provide AI-driven insights and bookkeeping services starting at $150 per month. These tools include benchmarks for key metrics like Customer Acquisition Cost (CAC) and valuation, giving startups the resources they need to stay competitive while maintaining sound financial practices during their growth phase.

Conclusion

Dynamic credit risk assessment leaves static and manual models in the dust, especially for fast-growth startups. The difference in speed is staggering: decisions that once took hours - or even days - now happen in seconds. For example, JPMorgan Chase's COiN platform reduced review times from hundreds of thousands of hours to mere seconds. In markets where timing can make or break a startup, this kind of agility means quicker access to capital when it’s needed most.

But it’s not just about speed. These systems also deliver better accuracy and broader accessibility. By analyzing real-time data and alternative signals, dynamic models uncover risk insights that static systems simply miss. Take CreditVidya, for instance: their approach boosted approval rates by 25% and slashed delinquency by 33% for first-time borrowers in India. Similarly, a Southeast Asian bank using Credolab's machine learning scoring reduced default rates by 30% while cutting approval times by 60%. These results show how dynamic models combine precise risk prediction with rapid decision-making.

For startups with little to no credit history, dynamic models are a game-changer. They tap into alternative data and advanced fraud detection to help secure funding based on actual performance metrics. PayPal, for example, uses AI to maintain an impressively low fraud rate of just 0.17%. This opens the door to competitive financing options that might otherwise be out of reach.

Given the clear advantages in speed, accuracy, and accessibility, adopting dynamic credit risk models is a no-brainer for startups that want to scale effectively. Tools like Lucid Financials make this transition seamless, offering AI-driven accounting, real-time Slack updates, and CFO-level reporting - all starting at just $150 per month. These platforms provide the financial infrastructure needed to make smarter decisions, impress investors, and maintain the momentum critical for success.

In today’s fast-paced market, outdated tools simply won’t cut it. Dynamic credit risk assessment turns financial management into a powerful competitive edge.

FAQs

What data do dynamic credit risk models use besides credit scores?

Dynamic credit risk models go beyond traditional credit scores by examining over 1,600 real-time data points. These models incorporate alternative factors like education background, banking habits, and utility payment history to create a more detailed picture of someone's creditworthiness. This approach offers a broader and more nuanced evaluation compared to relying solely on credit scores.

How do dynamic models protect privacy when using behavioral data?

Dynamic models protect privacy by processing data in real time and relying on advanced algorithms, minimizing the need to store or share raw personal information. By prioritizing immediate analysis over retaining sensitive details, this method reduces the risk of data exposure and strengthens security.

What does it take to implement dynamic credit risk at a startup?

Introducing dynamic credit risk management at a startup means leveraging AI-driven tools to analyze real-time data, such as banking activity and utility payment patterns. This approach relies heavily on machine learning models, natural language processing, and continuous monitoring to adjust credit limits on the fly based on a user's financial behavior.

To make this work, startups need more than just cutting-edge technology. A robust data infrastructure is essential to handle large volumes of real-time information. Additionally, having a team with the right expertise to build, train, and maintain these systems is crucial. Finally, startups must ensure they comply with all relevant regulations to integrate these tools effectively while supporting rapid growth.