Cross-border payments are growing fast, projected to reach $320 trillion by 2032 from $195 trillion in 2024. However, the process remains costly and complex due to fragmented regulations, slow systems, and compliance hurdles. Here's what you need to know:

- Global Efforts: Initiatives like the G20 Roadmap and BIS projects aim to improve speed, cost, and transparency, but progress is slower than planned.

- Regional Differences: The EU offers unified licensing (passporting), while the U.S. requires state-by-state licenses, and APAC focuses on linking domestic systems.

- Compliance Challenges: Startups face high costs, AML requirements, and sanctions screening. Compliance can consume up to 50% of early-stage budgets.

- AI Solutions: Advanced tools help reduce false positives in AML checks by up to 80%, saving time and money.

For fintech startups, understanding licensing rules, using AI for compliance, and focusing on specific regions can help navigate this complex landscape.

Global Regulatory Trends in Cross-Border Payments

The G20 Roadmap for Cross-Border Payments

The G20 Roadmap is a global initiative aimed at improving cross-border payments through three main strategies: enhancing payment system interoperability, standardizing data via ISO 20022 messaging, and aligning legal and regulatory frameworks. The goal is to make international payments faster, more affordable, and transparent for users, including fintech companies.

However, progress has been slower than anticipated. In late 2025, the Financial Stability Board (FSB) admitted that meeting the original 2027 targets for cost, speed, and transparency improvements is unlikely. To address this, the FSB held a Cross-Border Payments Summit in London in March 2026, where countries pledged to take concrete steps to upgrade their domestic payment systems.

"The clear message from today's Summit is that we are not stopping until the job of making a genuine difference to the user experience of cross-border payments is done." - Andrew Bailey, Chair of the FSB

Following the summit, Swift CEO Javier Pérez-Tasso announced that banks would implement a retail payments framework by June 2026 to improve speed, cost predictability, and transparency. Swift is also working on a blockchain-based shared ledger to enable 24/7 real-time cross-border transactions.

Key Findings from BIS and FSB Studies

Recent studies from the Bank for International Settlements (BIS) and the FSB highlight the current state of cross-border payments. A 2024 survey of 68 central banks revealed steady progress in adopting ISO 20022, though interoperability between payment systems still varies widely across regions.

Compliance costs for payment providers have surged by 20–30% annually, largely due to data localization requirements in countries like India and China. Additionally, manual investigations into failed transactions cost providers $30–$50 per case.

To address these challenges, the BIS introduced Project Nexus, which connects instant payment systems like India's UPI and Singapore's PayNow, enabling cross-border retail payments to settle in under 60 seconds. Another initiative, Project Mandala, aims to streamline compliance processes by automating the exchange of regulatory information between countries.

"Frictions in international payments have the potential to act as a driver of fragmentation of the global system, and this can ultimately reduce the system's ability to absorb shocks." - FSB Chair

Regional Frameworks: EU, US, and APAC

While global initiatives provide a broad direction, regional frameworks show how different regulatory approaches shape fintech operations. Here's a snapshot of key frameworks:

| Region | Key Framework | Focus for Fintechs |

|---|---|---|

| EU | MiCA (Markets in Crypto-Assets Regulation) | Licensing for crypto-asset service providers; strict AML and data transparency rules |

| US | FinCEN (Financial Crimes Enforcement Network) | Money Services Business registration; Bank Secrecy Act compliance; state-level licensing |

| APAC | Sandbox regimes (e.g., MAS in Singapore, RBA in Australia) | Regulatory sandboxes and integration of domestic payment systems |

The APAC region is currently ahead in linking domestic fast payment systems to facilitate cross-border transactions. In the EU, the MiCA framework simplifies crypto-asset licensing by creating a unified regulatory environment, reducing the complexity of operating across multiple countries. Meanwhile, fintech companies in the US face a more fragmented system, with FinCEN registration requirements and varying state-level money transmitter licenses making compliance particularly challenging.

For fintech startups, adopting ISO 20022 standards and modern API architectures is crucial to navigating these regional differences. Staying updated on regulatory changes, especially those granting non-bank access to domestic payment systems, can help reduce transaction costs and lessen dependence on traditional correspondent banking.

sbb-itb-17e8ec9

Cross-Border Payments Innovation & Strategy | Mick Fennell

Licensing and Compliance Requirements for Fintech Startups

Cross-Border Payment Licensing: US vs EU vs APAC Compared

Licensing Rules for Non-Bank Payment Providers

Understanding licensing requirements is a critical step for fintech startups, especially given the regulatory challenges they face. Around the world, regulators are increasingly adopting functional regulation. This means your licensing obligations depend on what your product does, not how you label it. For example, if your platform holds customer funds or processes transactions, you’ll likely need to comply with payment institution rules - even if you’re not a bank.

Compliance isn’t just a one-time task; it’s an ongoing expense. For established fintechs, it can account for 15–25% of operating costs, while startups in the early licensing phase might see it consume up to 40–50% of their monthly budget.

"The cost of implementing compliance correctly is substantial, but the cost of implementing it incorrectly proves existential." - Peter Ruggle, Founder, Ruggle Partner

US Licensing for Cross-Border Payments

In the United States, there’s no single federal license for cross-border payment providers. Instead, fintechs must navigate a two-tier system. First, they must register federally with FinCEN as a Money Services Business (MSB) under the Bank Secrecy Act. Then, they need to secure Money Transmitter Licenses (MTLs) in each state where they operate. To operate nationwide, this means managing 50+ state licenses in addition to the federal registration.

State MTL requirements can vary widely, covering aspects like capital reserves, surety bonds, and renewal schedules. Many early-stage fintechs opt to partner with federally chartered sponsor banks to meet these requirements. However, regulators are increasingly demanding that these fintechs maintain compliance documentation at the same level as banks.

For stablecoin issuers, the 2025 GENIUS Act introduced a federal framework, simplifying what was previously a complex, state-level patchwork of rules.

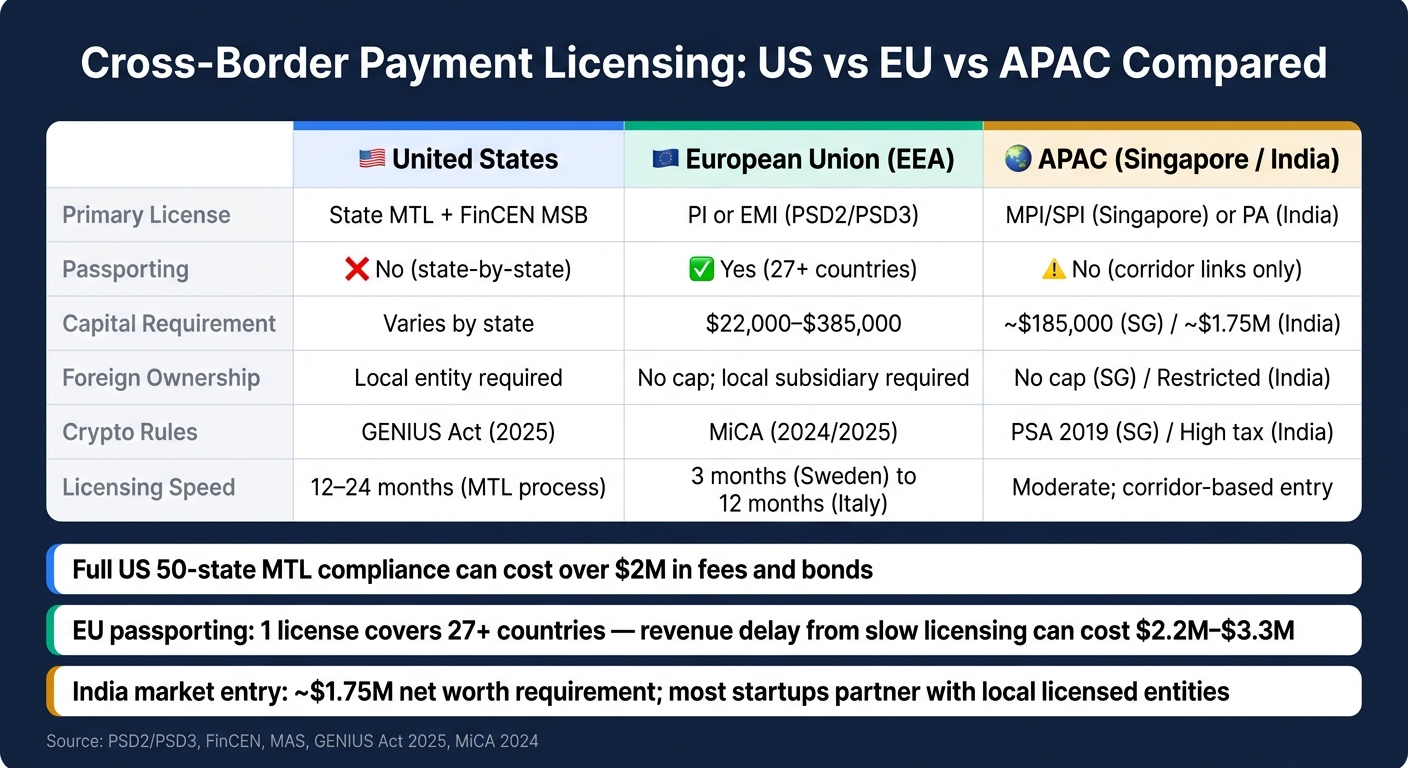

Licensing Requirements: US, EU, and APAC Compared

Regulatory frameworks differ significantly across regions, affecting both the speed and cost of market entry. Choosing the right jurisdiction is often as much a strategic decision as it is a legal one.

| Feature | United States | European Union (EEA) | APAC (Singapore / India) |

|---|---|---|---|

| Primary License | State MTL + FinCEN MSB | PI or EMI (PSD2/PSD3) | MPI/SPI (Singapore) or PA (India) |

| Passporting | No (state-by-state) | Yes (27+ countries) | No (corridor links only) |

| Capital Requirement | Varies by state | $22,000–$385,000 (PI to EMI) | ~$185,000 (SG) / ~$1.75M (India) |

| Foreign Ownership | Local entity required | No cap; local subsidiary required | No cap (SG) / Restricted (India) |

| Crypto Rules | GENIUS Act (2025) | MiCA (2024/2025) | PSA 2019 (SG) / High tax (India) |

The EU’s "one license, one market" approach is a standout feature. A license from one EEA member state can be used across all 27+ countries. However, the choice of jurisdiction still matters. For instance, licensing in Sweden takes about 3 months, whereas in Spain or Italy, it can take 6–12 months. Delays in the EU licensing process can have a significant financial impact, with one case in early 2025 reporting a $2.2M–$3.3M revenue loss due to prolonged application timelines.

In APAC, Singapore’s Major Payment Institution (MPI) license is highly regarded and provides direct connections to key payment corridors with countries like India (UPI) and Thailand (PromptPay). On the other hand, India poses higher barriers, including a requirement for local incorporation and a net worth of approximately $1.75 million. For most startups, partnering with a locally licensed entity is often the most practical way to enter the Indian market.

AML, Sanctions, and Transparency Compliance

AML/CFT Challenges in Cross-Border Payments

The rise of faster payment systems has significantly reduced the time available to flag suspicious transactions. Adding to the complexity, intermediary banks often pass along incomplete data, which increases the risk of missing potential red flags. Combined, these issues create a heavier compliance burden for fintech startups already grappling with fragmented regulations across jurisdictions.

The financial consequences are hard to ignore. In 2025, global AML-related fines imposed on financial institutions surpassed $6 billion.

One of the toughest hurdles is beneficial ownership verification. FinCEN's Beneficial Ownership Information (BOI) database rules require fintechs to continuously verify and update ownership details for their business clients - not just at the onboarding stage. This becomes even more challenging with the rise of mule account networks, where fraud syndicates quickly move funds across borders, making it difficult for any one institution to detect suspicious patterns in time. These hurdles also extend into sanctions screening and broader transparency obligations.

Sanctions Screening and Transparency Standards

Cross-border payment providers operating in or through the U.S. must screen counterparties against OFAC sanctions lists, as well as EU and UN lists for international transactions. With geopolitical tensions driving frequent updates to these lists, screening tools must be capable of keeping pace automatically.

The Travel Rule adds another layer of complexity. FATF's updated Recommendation 16 (June 2025) mandates that providers transmit standardized originator and beneficiary information for transfers exceeding $1,000. For fintechs, implementing this across multiple jurisdictions - each with slightly different technical standards - while maintaining data quality under ISO 20022 presents a significant challenge. Compounding the issue is uneven adoption of these standards, which often results in missing key data fields, making investigations and manual reviews even more difficult.

How AI Supports Compliance

Modern AI solutions are stepping in to tackle inefficiencies in compliance processes. Traditional rule-based systems, for instance, are notorious for generating false positives, with rates as high as 95–99%, which wastes valuable analyst time.

"If your compliance team is reviewing 500 alerts per week and 490 of them are false positives, analysts are spending most of their time confirming that legitimate transactions are legitimate." - Sahil Kataria, Fluxforce

AI and machine learning models can cut false positive rates by 60–80% when compared to traditional systems. These models don't rely on static thresholds. Instead, they create behavioral baselines for individual customers, flagging deviations from normal activity by analyzing hundreds of data points simultaneously.

Real-time risk scoring is another game-changer. Modern AI tools evaluate transactions as they happen, rather than relying on outdated overnight batch processes. For example, under EU regulations, SEPA Instant Credit Transfers became mandatory for receiving payments as of October 2025. This means AML and sanctions checks must operate at the same speed as instant payment systems. For fintechs working in these environments, relying on legacy compliance stacks is no longer a viable option.

For startups aiming to streamline compliance while maintaining fast transaction speeds, adopting AI-driven platforms is crucial. Tools like Lucid Financials integrate AI to provide real-time risk assessments and data-driven compliance, helping fintechs meet tough regulatory requirements without compromising efficiency.

Practical Guidance for Fintech Startups

Now that we've covered licensing and compliance essentials, let’s dive into actionable strategies to bring those insights to life.

Building a Regulation-Ready Business Model

For fintech startups in the U.S., it’s smart to focus on specific payment corridors - such as routes between two countries or regions - before attempting broader expansion. For example, if you’re targeting US-to-Mexico transfers, prioritize compliance with FinCEN, OFAC, and local Mexican regulations rather than stretching yourself thin across multiple jurisdictions.

Achieving full 50-state Money Transmitter License (MTL) compliance can cost over $2 million in fees and bonds. California alone mandates a minimum net worth of $2.5 million, while New York’s bonding requirements range from $500,000 to $10 million. For startups in their early stages, partnering with a licensed bank through Banking-as-a-Service (BaaS) can significantly reduce the typical 12–24 month MTL application process. Be aware, though, that this route may require sacrificing some control over pricing and customer relationships. It’s also crucial to clearly define responsibilities for tasks like Suspicious Activity Reports (SARs) and handling customer complaints to avoid regulatory missteps.

"Compliance is not a one-time checklist but a core, ongoing business function that dictates your technology stack, partnership model, and geographic rollout." - Able Finance

A smart strategy is to design your compliance framework to meet the strictest state standards first - often those of New York or California. This approach simplifies multi-state expansion and minimizes costly adjustments down the road.

Once you’ve nailed your business model, the next step is creating a financial system that tracks every transaction with precision.

Setting Up a Compliance-Ready Financial Stack

Your financial infrastructure should be built to generate clear, auditable records for every transaction from day one. These records need to detail the regulatory reasoning behind any automated decisions, the data inputs used, and a confidence score. In both the U.S. and EU, such records must typically be retained for five to seven years after a business relationship ends.

This level of detail is especially critical for cross-border payments. A single transaction can trigger compliance checks under FinCEN, OFAC, FATF, and the central bank rules of the receiving country. Without a system capable of managing these overlapping regulations, gaps can quickly emerge, becoming more expensive as transaction volumes grow. For example, failing to catch a match on the OFAC Specially Designated Nationals (SDN) list could result in penalties as high as $20 million per violation.

Another key tip? Track compliance costs as a separate line item in your budget. Compliance teams often spend 60–70% of their time on manual reviews, which highlights opportunities for automation to save time and money.

Using AI Tools for Finance and Compliance

Once your financial infrastructure is set, advanced AI tools can help optimize both compliance and financial operations.

"Compliance-first architecture costs 2–3 times less than rebuilding and withstands FinCEN examinations." - Haithem Abdelfattah, CEO, LaderaLABS

On the compliance side, AI-powered semantic entity resolution can dramatically reduce false positives - from rates as high as 95–98% down to 18–22% - while maintaining a 99.7% true positive detection rate. Fine-tuned AI models for cross-border entity resolution also outperform generic ones, achieving 94% accuracy compared to 67%. Regulators, however, now expect firms to document AI model development and test for algorithmic bias, making explainability a key requirement.

For financial operations, tools like Lucid Financials offer AI-driven bookkeeping, CFO-level forecasting, and real-time reporting. These features are especially valuable for fintechs managing complex structures like multi-entity setups, cross-border payments, and investor reporting. Keeping your books accurate and up-to-date ensures you’re always ready for audits and fundraising opportunities.

Key Takeaways on Cross-Border Payment Regulations

Cross-border payment volumes are expected to skyrocket, climbing from $195 trillion in 2024 to a staggering $320 trillion by 2032. With such massive growth on the horizon, regulatory clarity becomes a critical factor for fintech startups operating on a global scale.

Several important trends are shaping the regulatory environment. While regulatory fragmentation persists, it’s gradually diminishing. For instance, the EU's move from PSD2 to PSD3 aims to standardize rules across all member states. Meanwhile, real-time payment systems like SEPA Instant are transitioning from optional to mandatory. On the other hand, the UK, post-Brexit, is carving out its own regulatory path, creating dual compliance requirements for companies operating in both regions.

Jurisdiction matters. The choice of licensing jurisdiction can greatly influence operational efficiency. In the EU, processing times for the same license can vary dramatically - ranging from about 3 months in Sweden to as long as 12 months in Italy. Making the right decision upfront and leveraging passporting into larger markets can help fintech companies avoid delays and significant revenue losses.

AI is now a standard tool in compliance efforts. Traditional anti-money laundering (AML) systems often generate 90–95% false positives, but advanced AI models are slashing these rates by 80–90%. This not only boosts accuracy but also speeds up compliance processes.

Beyond compliance, having a solid infrastructure is indispensable. Real-time, auditable financial records are critical for passing FinCEN examinations, satisfying investor due diligence, and meeting reporting requirements across jurisdictions. Tools like Lucid Financials simplify this complexity by combining AI-powered bookkeeping with CFO-level expertise, ensuring startups stay ahead in managing their finances.

"Sustainable progress will require ongoing collaboration between financial firms, technology providers, and public-sector institutions." - World Economic Forum

FAQs

Which license do I need for cross-border payments in the U.S.?

To manage cross-border payments in the U.S., you’ll generally need a money transmitter license. This involves meeting the requirements of both federal and state regulations. However, depending on your business model and the states you operate in, there may be exemptions or alternative licensing approaches available.

How should a startup pick its first cross-border payment corridor?

Startups looking to select a cross-border payment corridor need to weigh several important factors. First, examine the regulatory environment to ensure it aligns with compliance needs, such as AML (Anti-Money Laundering) and KYC (Know Your Customer) requirements. A clear and well-defined licensing framework is also crucial to avoid legal hurdles.

Additionally, prioritize corridors that offer robust infrastructure and multi-currency support. Transparent foreign exchange (FX) rates can significantly improve cost efficiency, which is key for startups managing tight budgets.

Regions with scalable payment systems and reasonable entry barriers, such as Singapore or certain areas in Latin America, can be ideal choices. These locations often provide smoother operations and room for growth, making them attractive for businesses aiming to expand internationally.

What AI compliance records do regulators expect to see?

Regulators often require AI compliance records that include detailed governance documentation, comprehensive risk management frameworks, and proof of adherence to established standards like the Financial Services AI Risk Management Framework (FS AI RMF). These records must also show compliance with both U.S. and international regulations, covering areas such as Know Your Customer (KYC), Anti-Money Laundering (AML), OFAC sanctions screening, and transaction monitoring.