The cost of capital - the price startups pay for funding - varies significantly between SaaS and hardware businesses due to differences in expenses, revenue models, and risk. SaaS startups rely on recurring revenue and minimal physical assets, making them more scalable but heavily dependent on equity financing with costs that can exceed 50%. Hardware startups face higher upfront costs for manufacturing and inventory, often using debt secured by tangible assets but at higher borrowing rates.

Key takeaways:

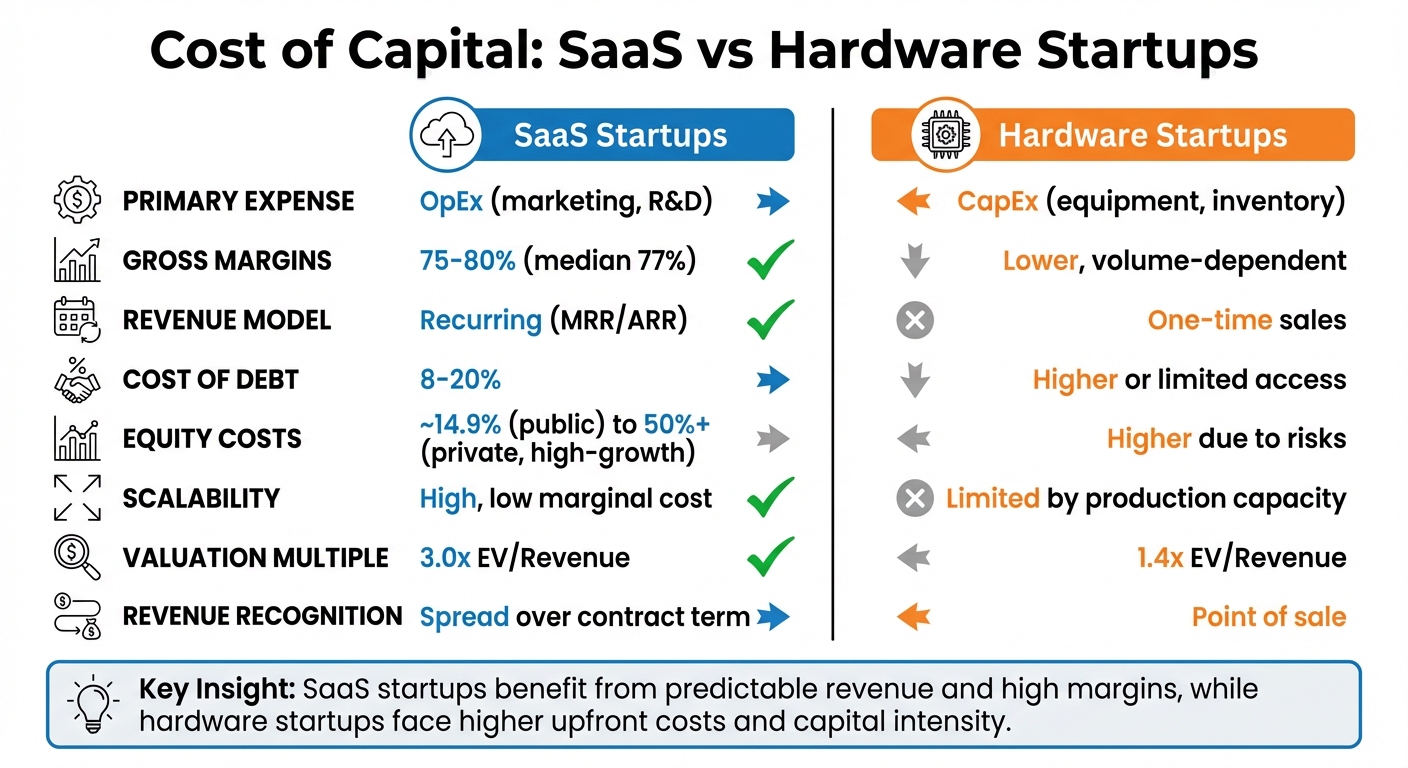

- SaaS startups: Focus on operational expenses (OpEx), high gross margins (~75-80%), predictable revenue (MRR/ARR), and faster scalability. They face higher equity costs but lower debt access barriers.

- Hardware startups: Capital-intensive with significant CapEx needs for production and inventory. Margins depend on scale, and cash flows are less predictable, leading to higher financing costs.

Quick Comparison:

| Metric | SaaS Startups | Hardware Startups |

|---|---|---|

| Primary Expense | OpEx (marketing, R&D) | CapEx (equipment, inventory) |

| Gross Margins | 75-80% | Lower, volume-dependent |

| Revenue Model | Recurring (MRR/ARR) | One-time sales |

| Cost of Debt | 8-20% | Higher or limited access |

| Equity Costs | ~14.9% (public) to 50%+ | Higher due to risks |

| Scalability | High, low marginal cost | Limited by production |

Understanding these differences helps founders choose the right funding strategies and manage costs effectively.

SaaS vs Hardware Startups: Cost of Capital Comparison

1.2.4: Hardware VS SaaS Startup - Why Building Physical Products Is So Different

sbb-itb-17e8ec9

How SaaS and Hardware Startups Differ

SaaS startups and hardware startups operate in fundamentally different ways, especially when it comes to revenue generation, capital needs, and risk management. SaaS businesses thrive on recurring subscription models with minimal physical assets, while hardware companies face significant upfront costs tied to production and inventory. Let’s break this down further.

SaaS Startups: Recurring Revenue and Minimal Capital Needs

SaaS businesses rely heavily on recurring revenue streams like Monthly Recurring Revenue (MRR) and Annual Recurring Revenue (ARR). These models provide steady, predictable cash flow, which is a big plus for investors as it reduces uncertainty and makes future earnings easier to project.

"SaaS is considered an Operating Expense (OpEx) rather than a Capital Expense (CapEx). This is because it operates on a rental model with no upfront cost, where businesses pay for the software as they use it." - Rowell, Founder, SaaS Lucid

After the initial development phase, the cost of serving additional customers is minimal. There’s no need for physical production, inventory, or distribution. Instead, SaaS companies channel their spending into R&D, marketing, and customer acquisition. This model scales efficiently, often through "pay-as-you-go" cloud services, keeping expenses aligned with growth.

"Software companies generally require much lower capital to reach profitability and continued growth. This is primarily because they don't need to invest in expensive equipment." - Phil Morettini, President, PJM Consulting

In short, SaaS startups benefit from lower capital requirements, faster scalability, and a more predictable financial outlook compared to their hardware counterparts.

Hardware Startups: Manufacturing and Inventory Challenges

Hardware startups face a completely different set of challenges. Significant upfront investments are required for manufacturing facilities, production equipment, tooling, and raw materials - all before any revenue is generated. These costs fall under capital expenditures (CapEx), creating tangible assets but requiring substantial funding early on.

Cash flow cycles are longer and more complex for hardware companies. They must pay for inventory, manufacturing, and logistics months before they can sell products and see revenue. This delay in cash flow creates what’s often called the "Valley of Death", particularly at the Series B stage when hardware startups typically need around $30 million or more to fund pilot facilities or first-of-a-kind plants.

For instance, climate tech hardware startups often raise 20% to 50% more equity than SaaS businesses, and nearly double that amount when including non-dilutive funding sources. A real-world example is Northvolt, a battery developer that raised 14 funding rounds between 2017 and 2024 - 8 equity and 6 debt rounds - to finance its manufacturing and infrastructure needs. By contrast, SaaS startups often exit after just 3 or 4 equity rounds.

Another challenge for hardware startups is their limited ability to pivot. Unlike software, which can be quickly updated based on market feedback, hardware products are costly and time-consuming to modify once manufacturing begins. This lack of flexibility increases risks and makes pivots financially burdensome, further driving up the cost of capital for hardware founders.

Financial Metrics and Capital Requirements Compared

The financial dynamics of SaaS and hardware startups are worlds apart, influencing both their capital needs and the cost of that capital.

Gross Margins and Scalability

SaaS startups enjoy gross margins between 75% and 80%, with the median sitting at 77% for private companies. Top performers can even exceed 85%. This is because once the software is built, the cost of adding new customers is minimal. Expenses like hosting (on platforms like AWS or Google Cloud), customer support, and third-party integrations grow much slower than revenue.

In contrast, hardware startups face a completely different reality. Their margins are tied to production volume and economies of scale. Costs for manufacturing, raw materials, and physical distribution significantly reduce profits - challenges SaaS companies don't encounter. For example, a cloud company with 50% gross margins, like Twilio, struggles to generate the same free cash flow as a company with 90% margins, such as Autodesk. These differences also impact valuation multiples.

"Software products, particularly those in SaaS and AI, can be scaled rapidly and reach a global market with minimal marginal costs." - Venture Capital

Investors are willing to pay more for SaaS businesses because high margins translate into better scalability and operational efficiency. On average, SaaS companies have a median valuation of 3.0x EV/Revenue and 15.2x EV/EBITDA, while hardware firms trail at 1.4x EV/Revenue and 11.0x EV/EBITDA. These margin advantages also influence how revenue is recognized and how cash flows are managed.

Revenue Models and Cash Flow Patterns

SaaS companies leverage subscription-based revenue models, generating Monthly Recurring Revenue (MRR) and Annual Recurring Revenue (ARR). This spreads revenue recognition over the length of contracts, providing predictable cash flows. On the other hand, hardware companies recognize revenue at the point of sale, resulting in more variable and less predictable cash flows.

This predictability gives SaaS startups a clear edge when it comes to raising capital. While the median Customer Acquisition Cost (CAC) payback period is 20 months - creating a short-term cash flow gap - investors are familiar with the model and its long-term potential. SaaS businesses can often secure debt financing at rates between 8% and 20%, with Debt-to-ARR ratios ranging from 0.3x to 1.0x. Hardware startups, however, face higher borrowing costs and often struggle to access debt due to their less predictable revenue streams and higher capital needs.

"SaaS businesses can uniquely benefit from this pricing disparity because of their highly predictable recurring revenue models and well-understood unit economics. That predictability... is the SaaS entrepreneur's secret weapon." - Randall Lucas, Managing Director, SaaS Capital

Equity costs tell a similar story. Public SaaS companies average a long-term cost of equity of 14.9%. For private, fast-growing SaaS startups, this can rise to around 50%, as selling shares in a high-margin, high-growth business comes at a premium. Hardware startups, with their longer road to profitability and higher risks, face even steeper equity costs. These cash flow differences directly affect the availability and cost of both debt and equity financing for SaaS and hardware companies.

SaaS vs. Hardware Financial Metrics

Here's a comparison of key financial metrics between SaaS and hardware startups:

| Metric | SaaS Startups | Hardware Startups |

|---|---|---|

| Gross Margins | 75-80% (median 77%) | Volume-dependent (typically lower) |

| Revenue Model | Recurring subscription (MRR/ARR) | One-time point-of-sale |

| Primary Expense Type | OpEx (cloud, salaries, marketing) | CapEx (equipment, inventory, tooling) |

| Scalability | Exponential; low marginal cost | Linear; limited by production capacity |

| Valuation Multiple | 3.0x EV/Revenue | 1.4x EV/Revenue |

| Cost of Debt | 8-20% | Higher or limited access |

| Revenue Recognition | Ratable over contract term | Recognized at point of sale |

SaaS founders must focus on maintaining high gross margins while managing their CAC payback periods. Early-stage companies should aim for at least 50% gross margins, with mature businesses targeting 70% to 80%. For hardware founders, achieving production volume quickly is essential for improving margins and demonstrating a clear path to profitability - both critical for reducing capital costs.

Capital Structure and Risk Factors

When comparing SaaS and hardware startups, their approaches to funding and the risks they face are vastly different. These differences directly influence their cost of capital.

Equity and Debt Financing

SaaS startups rely on their recurring revenue streams to secure venture debt at competitive rates. Unlike hardware companies, which often use physical assets like equipment or inventory as collateral, SaaS businesses typically lack such tangible assets. Still, they can secure debt financing with interest rates ranging from 8% to 20%, depending on their size and profitability. On the other hand, hardware startups utilize their physical assets to secure loans, but their initial capital requirements are much higher.

The cost of financing also varies significantly. Equity financing is far pricier than debt, especially for high-growth SaaS companies. For instance, in July 2024, SaaS Capital analyzed RocketRide Inc., a hypothetical company with $10 million in ARR growing at 60% annually, estimating its equity cost at 50%. In contrast, SlowSoft Inc., with $50 million in ARR and a slower growth rate of 10%, faced a much lower equity cost of 19.8%. To put this into perspective, in a $100 million exit, a SaaS founder who used debt financing might walk away with $96 million after repaying $3.6 million in debt. However, a founder who gave up 17% equity would retain only $83 million.

Increasingly, SaaS companies turn to debt for predictable expenses like sales and marketing while reserving equity for riskier growth initiatives or when they require more capital than lenders are willing to provide.

"Equity is more expensive than debt in the long run due to its lack of accessibility, the hyper-competitive nature of the current equity deal landscape, and the hidden costs associated with it due to the risk investors take on."

- Wendy Jarchow, Chief Investment Officer, River SaaS Capital

These differences in financing lay the groundwork for the unique risks that influence each model's cost of capital.

Risk Factors That Affect Cost of Capital

Operational risks further shape how capital costs differ between SaaS and hardware companies. For SaaS businesses, concerns like customer churn, net new ARR growth, and pricing pressures take center stage. Lenders tend to favor companies with low churn rates and consistent revenue growth. High churn, however, signals unstable cash flows, driving up the cost of both debt and equity.

Hardware startups face a different set of challenges, including supply chain disruptions, manufacturing delays, and inventory issues. A single supplier hiccup can halt production entirely, disrupting cash flow and profitability. These risks lead to higher equity premiums and stricter debt terms, as investors demand greater returns to offset the uncertainty.

Revenue predictability makes a big difference here. SaaS companies benefit from clear unit economics and recurring revenue, which reduces perceived risk. In contrast, hardware companies deal with more unpredictable operational factors, making it essential for them to tightly manage supply chains and demonstrate scalability before they can lower their cost of capital.

What Investors Look For and How Founders Should Respond

Why Investors Prefer SaaS or Hardware

Investors often gravitate toward SaaS startups because of their scalability and steady revenue streams. Subscription-based models provide predictable, long-term income, which reduces risk and appeals to venture capitalists aiming for rapid growth. For instance, private SaaS companies with strong performance metrics can secure valuation multiples of 7–10× ARR if they grow at 40% or more annually. In contrast, slower-growing SaaS companies typically see multiples between 3–5×.

Hardware startups, on the other hand, face a different set of challenges. They require significant upfront capital to handle lengthy R&D cycles and the high costs of scaling production. Constraints like physical manufacturing and material expenses can limit their growth potential compared to software companies. For hardware investments, tangible assets and personal guarantees often play a crucial role, as loans can’t easily be secured against non-tangible assets like prepaid subscriptions.

The metrics investors focus on also vary widely. For SaaS businesses, strong unit economics are critical. Key benchmarks include Net Revenue Retention (NRR) above 110%, gross margins in the 75–80% range, and healthy LTV:CAC ratios. Conversely, hardware investors prioritize metrics like capital expenditures, manufacturing efficiency, and supply chain resilience. Additionally, private equity firms now account for nearly half (46%) of SaaS acquisitions, often emphasizing compliance with the "Rule of 40" - a balance between growth rate and profit margins - and the importance of predictable revenue streams.

These differences highlight the importance of aligning your funding strategy with the specific growth stage and industry expectations of your business.

How to Lower Your Cost of Capital

To reduce capital costs, founders need to align their funding strategies with investor expectations and their company’s growth stage. One effective approach is to match the type of funding to its intended use. For example, debt financing, which typically costs between 8% and 20% for tech companies, is better suited for predictable expenses like sales and marketing. In contrast, equity - often more expensive, with costs reaching up to 50% for fast-growing SaaS startups - should be reserved for higher-risk initiatives or situations where the required capital surpasses what debt providers are willing to offer.

"SaaS businesses can uniquely benefit from this pricing disparity because of their highly predictable recurring revenue models and well‑understood unit economics."

- Randall Lucas, Managing Director, SaaS Capital

Founders should also explore R&D tax credits and grants to offset innovation costs without diluting equity. For SaaS companies, capitalizing software development expenses shifts these costs to the balance sheet, improving EBITDA and boosting valuations. Hardware startups can take advantage of government grants aimed at manufacturing innovation and consider using "Digital Twin" technology to create virtual prototypes, cutting down on costly physical iterations.

Maintaining strong unit economics is another way to attract favorable investor terms. For example, private SaaS companies typically achieve a median gross margin of 77%, with top performers exceeding 85%. It's also essential to demonstrate financial stability by maintaining at least 12–18 months of runway after securing funding. Hardware companies, meanwhile, can adopt modular designs to simplify product updates and reduce future iteration costs.

Lastly, having investor-ready financials is crucial for reducing perceived risk and securing better funding terms. Tools like Lucid Financials can help ensure your financial records are accurate, current, and prepared for investor scrutiny. Whether you’re building software or hardware, presenting well-organized financials can make a big difference in lowering your cost of capital.

Conclusion

Grasping the cost of capital isn't just a financial exercise - it's a critical decision-making tool for founders navigating funding and growth strategies. The challenges faced by SaaS and hardware startups differ significantly, and understanding these distinctions can help avoid costly mistakes and unnecessary dilution.

For example, launching a typical SaaS startup in 2026 might require over $400,000 in initial costs, with founders enduring about 23 months of negative EBITDA before breaking even. On the other hand, hardware startups face steeper hurdles, with higher manufacturing and inventory expenses. Some software companies have even raised massive amounts before going public, further complicating the traditional understanding of capital needs.

To succeed, founders must align their funding strategies with their business models. SaaS founders often encounter debt rates ranging from 8% to 20% and equity costs that can soar to 50% during periods of rapid growth. Meanwhile, hardware founders must navigate the constraints of physical assets and supply chains. Both models demand financial discipline: SaaS companies should aim for customer acquisition cost (CAC) payback periods of less than 12 months, while hardware startups can benefit from operational efficiencies to cut costs.

Accurate financials are a powerful asset, reducing risks and improving funding terms. Tools like Lucid Financials can help ensure your financial records are precise and up-to-date, empowering you to make smarter funding decisions. Founders who understand these capital dynamics can better tailor their strategies, preserve equity, and fuel sustainable growth - even as the cost of capital fluctuates based on growth rates, revenue models, and business stages.

FAQs

When should a SaaS startup use debt instead of equity?

Debt financing can be a smart choice for a SaaS startup if it has consistent cash flow, wants to maintain full ownership, and could use the advantage of tax-deductible interest payments. This approach works well for more established SaaS companies with reliable revenue streams, as it involves regular repayments. However, it does carry risk - especially if cash flow becomes unstable.

For startups with unpredictable or irregular cash flow, equity financing might be a safer route. While it means giving up a portion of ownership, it eliminates the pressure of repayment obligations, providing more flexibility during uncertain times.

What makes hardware startups more expensive to finance?

Hardware startups often come with a hefty price tag, primarily because they require substantial upfront investments. These costs typically include manufacturing, supply chains, and infrastructure, all of which demand significant capital expenditures (CapEx). Unlike software startups, hardware ventures also face longer development timelines, making it harder to adapt quickly to market changes. On top of that, they often need continuous funding to stay on track until they become viable businesses. All these challenges not only heighten risks for investors but also drive up the overall cost of capital compared to their software counterparts.

Which metrics most affect cost of capital for SaaS vs. hardware?

The cost of capital varies significantly between SaaS and hardware startups because of the different metrics and challenges each faces. For SaaS startups, key drivers include Monthly Recurring Revenue (MRR), churn rate, Customer Acquisition Cost (CAC), and growth rate. These metrics highlight both the company's stability and its potential for growth, which are crucial for attracting investors.

On the other hand, hardware startups deal with a more capital-intensive model. Their cost of capital is shaped by factors like capital expenses (CapEx), operational expenses (OpEx), and regulatory costs. These businesses often face longer development cycles and industry-specific risks, making these financial elements more critical in determining their funding landscape.