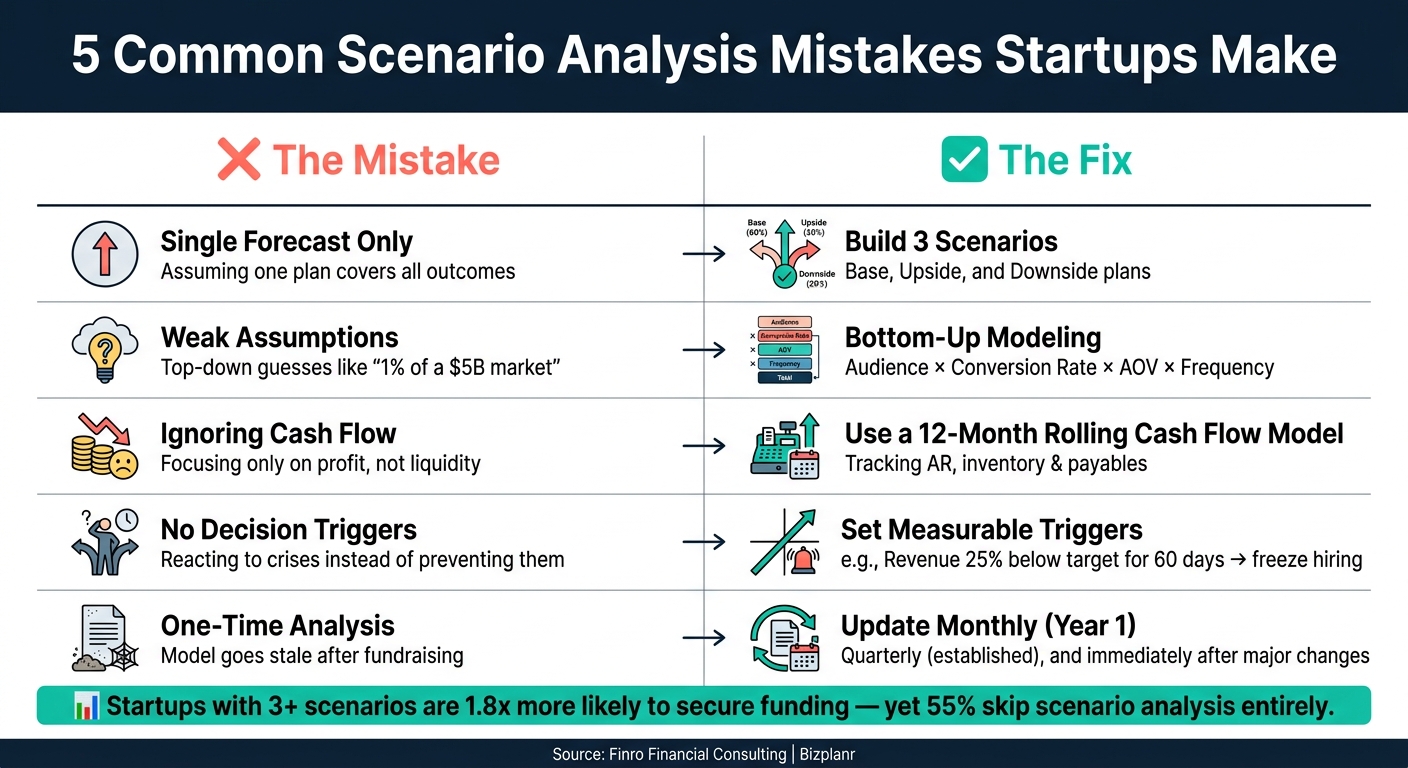

Scenario analysis is a powerful tool for startups to plan for uncertainty, yet many founders misuse or overlook it.

Key mistakes include:

- Treating a single forecast as scenario analysis.

- Relying on unrealistic or weak assumptions.

- Ignoring critical variables like cash flow timing.

- Failing to define actionable triggers for decision-making.

- Conducting scenario analysis only once, leading to outdated models.

Why it matters: Startups that prepare multiple scenarios are 1.8x more likely to secure funding, but 55% skip this step entirely. Proper scenario analysis helps identify risks, manage cash flow, and build investor confidence.

How to avoid these pitfalls:

- Build three scenarios: Base, Upside, and Downside.

- Validate assumptions with data, not guesses.

- Focus on cash flow, not just profit, and use a rolling 12-month model.

- Set specific triggers tied to measurable metrics for quick action.

- Regularly update your model to reflect changing conditions.

Get this right, and scenario analysis becomes a decision-making tool, not just a spreadsheet exercise.

5 Scenario Analysis Mistakes Startups Make (And How to Fix Them)

How to Show Upside, Base Case, and Downside Scenarios in Financial Model for Investors

sbb-itb-17e8ec9

Mistake 1: Treating Scenario Analysis as a Single Forecast

Many founders fall into the trap of confusing a single forecast with genuine scenario analysis. True risk assessment means preparing for multiple possible futures - not just the one you’re hoping for.

The Flaws of One-Case Forecasting

Relying on a single forecast assumes everything will go as planned - perfect execution, stable markets, and no surprises. But even small deviations can derail this approach. For instance, if customer acquisition ends up 40% lower than expected, your model quickly becomes irrelevant. This kind of thinking often reflects confirmation bias, where the forecast simply reinforces what you already believe.

"Investors know the plan will not go exactly as forecasted. What they want to see is how the business performs under different conditions." - Finro Financial Consulting

When you only provide one forecast, it signals to investors that you haven’t adequately considered risks. Without a plan for setbacks - like slower growth or delayed funding - you leave yourself vulnerable. The solution? Shift to a multi-scenario framework that examines a range of outcomes.

Building Multiple Scenarios

To create effective scenarios, avoid simply tweaking top-line numbers. Instead, base each scenario on real, measurable drivers. A good starting point is to develop three cases:

- Base Case: Represents your most realistic assumptions (approximately 60% probability). This is the main guide for your team and investors.

- Upside Case: Models faster growth, better margins, and lower customer acquisition costs (approximately 20% probability). Use this to plan for scaling and aggressive hiring.

- Downside Case: Accounts for slower traction, higher burn rates, and potential delays in funding (approximately 20% probability). This is your safety net for risk management and extending runway.

| Scenario | Probability | Focus | Purpose |

|---|---|---|---|

| Base Case | ~60% | Realistic growth and standard costs | Primary guide for investors and team |

| Upside Case | ~20% | Faster growth, lower CAC, higher efficiency | Planning for scale and hiring aggressively |

| Downside Case | ~20% | Slower traction, higher burn, delayed funding | Risk management and runway extension |

Stress-test key variables, like revenue growth rates and customer acquisition costs, to uncover potential cash flow challenges. This disciplined approach not only improves decision-making but also reassures investors.

"A projection that shows where it might break often builds more confidence than one that only shows upside." - Bizplanr

Mistake 2: Using Weak or Unrealistic Assumptions

Even the best-designed scenarios can fall apart if they rely on shaky assumptions. Faulty inputs lead to models that are neither accurate nor dependable.

"Most financial projection mistakes in a business plan come down to the assumptions underneath the numbers: where they came from, whether they hold up, and whether they connect to how the business actually works." - Kaylee Philbrick-Theuerkauf, Bizplanr

Common Unrealistic Assumptions

One of the most common missteps is the top-down revenue assumption: "We'll capture just 1% of a $5B market." While this might seem like a modest goal, it often lacks a clear strategy to back it up. There's no mention of how many leads are needed, what conversion rates are expected, or how long the sales cycle might take.

Another frequent error is overestimating how quickly customers will adopt a product. Many startups predict rapid Year 1 growth, ignoring that it usually takes one to three years to establish product-market fit and build reliable customer acquisition channels. Similarly, costs are often underestimated. Founders might forget about payment processing fees (e.g., Stripe charges around 2.9% + $0.30 per transaction), payroll taxes, or the cumulative expense of software subscriptions, which can easily run $1,500–$2,000 per month for user-based pricing models.

Other unrealistic assumptions include expecting 100% customer retention or neglecting to account for founder salaries, both of which distort the true picture of costs and growth.

The solution? Validate every assumption with solid, data-driven evidence.

How to Validate Assumptions with Reliable Data

Shift from broad, top-down estimates to bottom-up modeling. This approach builds revenue projections from specific, traceable factors: reachable audience × conversion rate × average order value × purchase frequency. Each assumption should be backed by credible data, whether from industry benchmarks like IBISWorld, competitor pricing, or your own historical performance.

"Revenue without unit economics is meaningless. Investors care far more about the efficiency and sustainability of growth than the size of the top line." - Lior Ronen, Founder, Finro Financial Consulting

When modeling costs, tie them to operational triggers such as adding new team members or upgrading infrastructure, instead of using a flat percentage of revenue. Include a 15–20% buffer in variable costs to account for unexpected expenses. Also, remember to factor in seasonal trends. For instance, a B2B consulting firm might see 40% of its annual revenue in Q1 and Q4, while summer months account for as little as 10%. Distributing revenue evenly across the year could obscure these fluctuations.

| Assumption Type | Unrealistic | Realistic (Bottom-Up) |

|---|---|---|

| Revenue | "We'll get 1% of the $5B market." | 2,000 site visitors × 3% conversion × $50 order value |

| Growth | "Hockey stick" spike without explanation | Growth tied to specific paid campaigns or partnerships |

| Costs | Expenses as a flat 10% of revenue | Costs tied to headcount, usage, and specific milestones |

| Retention | 100% retention (no churn modeled) | Churn tracked by cohort; revenue decay included |

Mistake 3: Ignoring Key Variables and Cash Flow Effects

Leaving out key variables in a scenario model can give you a distorted view of your finances. Many startups focus almost entirely on their income statement - revenue, gross margin, EBITDA - and stop there. But here’s the catch: profit and cash aren’t the same thing. This misunderstanding can create a gap between what your income statement says and your actual liquidity.

"Profit is an accrual concept. Cash is a timing concept. The gap between the two widens precisely when it matters most - during growth, during stress, and during the transitions between the two." - One Tribe Advisory

The Risks of Overlooking Key Variables

When key variables are ignored, the financial model may look cleaner, but it’s not accurate. For example, a startup might appear profitable on paper while unknowingly heading toward a liquidity crunch. Why? Because the model doesn’t account for when cash actually moves. This flaw leaves your financial planning fragile, especially in multi-scenario frameworks.

Three commonly overlooked variables are accounts receivable (AR) collection periods, inventory days, and supplier payment terms. These factors determine how long your cash is tied up, which is measured by the Cash Conversion Cycle (CCC): receivable days + inventory days − payable days. If your CCC worsens, it means cash is being consumed faster than your profit and loss (P&L) statement suggests. For instance, a 50-day increase in the CCC for a company with $10 million in revenue could tie up about $1.4 million in extra working capital.

Both growth and decline can drain cash. During rapid growth, cash is stretched thin as inventory builds up and payment terms extend. On the flip side, in a downturn, customers take longer to pay, and suppliers may tighten payment terms. In either case, cash disappears faster than profit figures would indicate.

Other often-missed variables include committed capital expenditures (capex), debt service, and tax payment timing. These factors can create unexpected cash drains. For instance, if your revenue drops but you owe taxes based on last year’s profits, your cash flow could take a significant hit - something a P&L-focused model wouldn’t catch.

Building a More Accurate Cash Flow Model

To close the gap between profit and cash, you need a refined scenario model that bridges the P&L to actual liquidity. Start with EBITDA and work through adjustments to account for cash flow impacts. Here’s a step-by-step breakdown:

| Step | Item | Source / Calculation |

|---|---|---|

| 1 | EBITDA | From the P&L scenario |

| 2 | Working Capital Movement | Change in receivables + change in inventory − change in payables |

| 3 | Capital Expenditure | Committed capex + variable capex |

| 4 | Debt Service | Interest payments + scheduled principal repayments |

| 5 | Tax Payments | Based on prior-year liability and current estimates |

| 6 | Net Cash Flow | EBITDA − Working Capital − Capex − Debt Service − Tax |

Use a 12-month rolling cash flow model instead of annual totals. Annual models tend to smooth over the critical seasonal dips when cash might actually run out. A monthly model helps you pinpoint specific months where slow collections overlap with large outflows - giving you a chance to act before it’s too late.

"Most founders struggle with cash flows because they're used to managing budgets, not working capital. That's why AR, AP, and billing assumptions, not just topline, separate a fantasy model from reality." - Pam Prior, Financial Expert

If this level of detail feels overwhelming, tools like Lucid Financials can simplify the process. Lucid’s CFO support can provide cash flow visibility, runway tracking, and scenario modeling to ensure your plans reflect actual cash timing - not just projected profit.

Mistake 4: Not Defining Triggers and Response Actions

Once you've fine-tuned your financial scenarios, the next step is making them actionable. This means setting up clear triggers that dictate when to act and what to do. Without these, even the most detailed scenarios can become useless, sitting in spreadsheets until a crisis forces a reaction. The problem isn’t the scenarios themselves; it’s the lack of a plan for when and how to respond. Defining triggers transforms your analysis into a proactive strategy.

Why Triggers and Actions Are Critical

In a real-world scenario, hesitation can be costly. If you don’t have predefined decision points, your leadership team might waste valuable time debating next steps as the situation worsens. Triggers eliminate this uncertainty by establishing clear instructions: if X happens, then Y follows. No second-guessing required.

These numerical triggers do more than just ensure quick internal reactions, like pausing non-essential spending when your runway drops below six months. They also show investors that your startup is prepared and managing risks strategically. In fact, startups that prepare three or more financial scenarios are 1.8 times more likely to secure funding compared to those relying on just one projection.

How to Create Effective Triggers

To make triggers work, they need to be specific and measurable. Vague criteria - like "if growth slows" - leave too much room for interpretation. Instead, tie your triggers to concrete metrics you’re already tracking.

By defining measurable triggers, you create a direct link between your scenario models and your financial strategy. This ensures you're ready to act, no matter what happens.

| Scenario Type | Trigger | Response Action |

|---|---|---|

| Downside Case | Revenue 25% below target for 60 days | Freeze non-essential hiring; cut marketing spend |

| Cash/Funding Case | Runway drops below 6 months | Start bridge fundraising or cut costs immediately |

| Upside Case | CAC 20% lower than projected | Invest surplus cash into expanding sales |

In addition to revenue and runway, keep an eye on unit economics like Customer Acquisition Cost (CAC), Net Revenue Retention (NRR), and lead conversion rates. For example, if NRR dips below 100%, it means new customers are only replacing churned ones. This could signal deeper issues with your product or pricing strategy.

Assigning ownership is another key step. Make sure specific team members are responsible for monitoring each trigger and escalating issues when thresholds are breached. Regularly review these triggers during monthly or quarterly meetings to ensure they stay relevant as market conditions change.

Technology can make this process easier. Tools like Lucid Financials use AI to monitor triggers and send real-time alerts, helping you act quickly when something changes. This complements the scenario planning you've already done and ensures you're always a step ahead.

Mistake 5: Running Scenario Analysis Only Once

Many startups fall into the trap of conducting scenario analysis just once - often before a fundraising round. But the reality is, markets shift, hiring plans evolve, customer behaviors change, and costs fluctuate. A financial model created even six months ago can quickly become outdated and irrelevant.

The Problem with Outdated Models

When your model remains static, it loses accuracy as soon as real-world conditions deviate from the original assumptions. One of the most dangerous risks here is the gap between accounting profit and actual cash flow. A startup might appear profitable on paper while silently running out of cash. Why? Because the model doesn't account for things like delayed payments, irregular billing cycles, or sudden cost spikes (e.g., infrastructure expenses).

As your business grows or unexpected costs arise, leadership might miss early warning signs, creating a disconnect between projected and actual performance. This makes regular updates to your scenario analysis not just helpful but essential.

How to Keep Scenarios Up to Date

The key to staying ahead is establishing a dynamic review process. Regular updates based on real-time data and specific triggers ensure your model reflects current realities.

Here’s a suggested update cadence based on your startup's stage:

| Business Stage | Update Frequency | Primary Focus |

|---|---|---|

| Pre-Revenue | Quarterly | Validating assumptions |

| Post-Launch (Year 1) | Monthly | Integrating real-world data and monitoring burn rate |

| Established/Post-Funding | Quarterly | Tracking milestones and refining capital strategy |

| Major Change Event | Immediately | Adjusting for revenue variances or cost shifts |

In addition to scheduled updates, be ready to act on specific triggers. For example, if revenue falls short of projections by more than 20% for two consecutive months, update your model immediately - don’t wait for the next quarterly review. Similarly, make adjustments when you introduce a new revenue stream, onboard a key hire, or face a major supplier change.

To streamline updates, use driver-based inputs. Instead of relying on broad market share estimates, drill down into actionable metrics like website traffic, conversion rates, and customer acquisition costs. When one variable changes, adjust that input, and let the model update automatically. Linking your financial statements - so changes in payment terms ripple across your cash flow and balance sheet - saves time and ensures accuracy.

"A great financial model does not live in Excel. It lives at the center of how the company plans, operates, and scales." - Lior Ronen, Founder, Finro Financial Consulting

Platforms like Lucid Financials can help by automating real-time financial updates. Whether you’re hiring, fundraising, or navigating challenges, a regularly updated model becomes a reliable decision-making tool - not just a static document collecting dust.

Conclusion: How to Get Scenario Analysis Right

Looking at these common mistakes highlights how essential solid scenario analysis is for effective financial planning in startups. For scenario analysis to deliver real value, it requires accurate assumptions, detailed cash flow modeling, and frequent updates. The errors discussed - like relying on a single forecast, using unrealistic assumptions, overlooking cash timing, skipping trigger points, or sticking with a static model - can all be avoided with a disciplined approach.

When startups address these issues, they can turn financial forecasting into a real strategic edge. For example, startups that prepare at least three scenarios are 1.8 times more likely to secure funding, yet a staggering 88% of financial models contain critical errors. The challenge lies in bridging the gap between knowing what effective scenario analysis looks like and actually implementing it.

"A credible startup financial forecast is not about predicting the future perfectly. It is about proving that you understand how your business works and how it will scale." - Lior Ronen, Founder, Finro Financial Consulting

The solution? Start from scratch when necessary, ensure cash timing and step-function costs are modeled correctly, and revisit your assumptions regularly.

For startups looking to streamline this process, Lucid Financials offers tools designed specifically for these challenges. Its AI-powered platform delivers real-time financial insights, automated forecasts, and investor-ready reports - eliminating the manual errors that come with spreadsheets. Whether you're raising funds or managing burn, having up-to-date financials can make every decision sharper.

FAQs

Which drivers should I vary between Base, Upside, and Downside?

To create a well-rounded financial forecast, adjust critical factors like customer acquisition, revenue growth, retention rates, and cost assumptions across three scenarios: Base, Upside, and Downside. This approach helps account for uncertainties and ensures your projections reflect a range of potential outcomes.

What cash-flow timing items should my scenarios include?

When creating financial scenarios, it's essential to factor in cash-flow timing. This means accounting for the exact timing of when money comes in (revenue inflows) and when it goes out (expense outflows). Why? Because it gives you a more accurate picture of your business's financial health.

By aligning your financial planning with the actual flow of cash, you avoid surprises like running out of money to cover expenses simply because payments from customers haven't arrived yet. It’s not just about knowing how much money you’ll have - it’s about knowing when you’ll have it.

How do I choose triggers and actions for each scenario?

Start by pinpointing the key signals - or triggers - that indicate a specific scenario is developing. For instance, a noticeable drop in sales or shifts in market trends could act as these early warning signs. Once you've identified these triggers, outline the actions your team should take in response. This might include reallocating resources, tweaking strategies, or revisiting priorities.

It's also crucial to assign clear responsibilities. Designate team members to monitor these triggers and take charge of executing the corresponding actions. This ensures your responses are both timely and effective.

By directly linking triggers to actions, your startup can react faster to changes and refine its scenario planning process.