Startups are prime targets for fraud due to limited resources and minimal safeguards. Behavioral analytics offers a modern, effective way to combat these threats by analyzing user behavior in real time. Instead of relying on outdated rules, it detects suspicious actions like rapid navigation or inconsistent typing patterns, helping startups prevent losses while maintaining a smooth customer experience.

Key Takeaways:

- Fraud Challenges: Account takeovers, synthetic identity fraud, and insider threats are common issues.

- Behavioral Analytics Benefits: Detects up to 90% of fraud with 99% accuracy, reduces false positives, and minimizes manual reviews.

- How It Works: Tracks digital actions (e.g., mouse movements, typing speed) to flag unusual behavior before submission.

- Implementation Steps: Collect real-time data, deploy machine learning models, and integrate insights into financial systems.

- Results: Faster fraud detection, fewer false alarms, and cost savings for startups.

Behavioral analytics is an effective tool for startups to protect themselves from fraud while ensuring a seamless user experience.

Behavioral Analytics Impact on Fraud Detection: Key Statistics and Benefits for Startups

Revolutionizing Fraud Prevention with Behavioral Intelligence

sbb-itb-17e8ec9

Common Fraud Problems Startups Face

Startups face several fraud challenges that exploit their unique vulnerabilities. Among the most pressing issues are account takeovers, synthetic identity fraud, and insider threats. Each of these requires vigilant monitoring and quick responses to mitigate damage effectively.

Account Takeovers and Payment Fraud

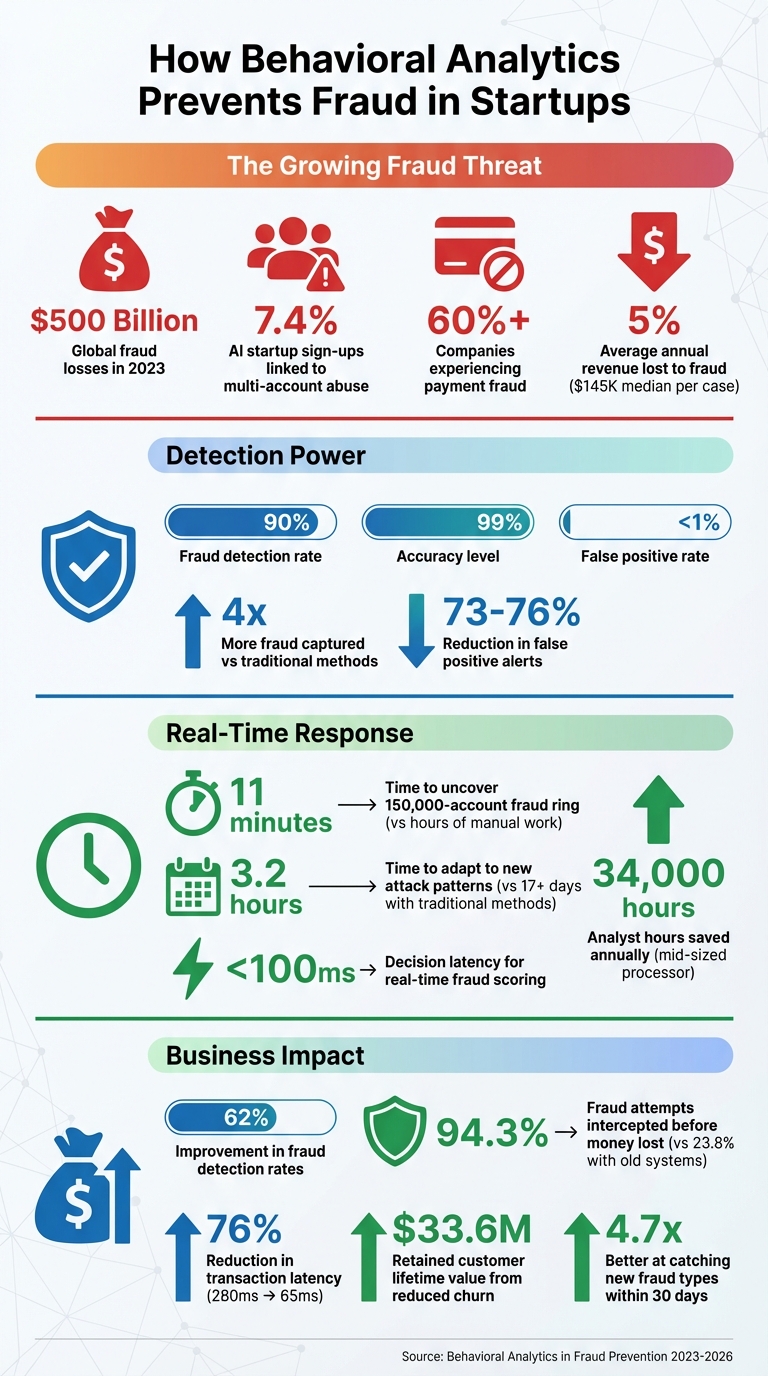

Fraudsters often use stolen credentials to break into user accounts through phishing or credential-stuffing techniques. Once they gain access, they waste no time changing payment details, making unauthorized transactions, or emptying account balances. These attacks bypass many traditional security methods with alarming ease. In fact, global fraud scams accounted for an astounding $500 billion in 2023.

Adding to the complexity, generative AI has become a tool for fraudsters. It can create fake IDs, voice prints, and even realistic selfies that can fool biometric verification systems. Jonathan Hart, Senior Product Manager of Digital Identity & Fraud at LSEG, explains:

"One thing a fraudster can't hide is their behaviour. Fraudsters who have taken over an account or 'activated' their Synthetic IDs will move fast to generate as much cash as possible before their financial institution detects their activities."

Traditional defenses like IP blocklists or device fingerprinting often fall short because criminals use advanced tools such as residential proxies and headless browsers, which mimic legitimate user activity. For example, fraudsters can paste stolen credit card information and act in under a second, far faster than the typical 4–15 seconds it takes for a legitimate user to complete similar actions.

This is just one layer of the problem. Startups must also address the growing threat of synthetic identity fraud.

Synthetic Identity Fraud

Synthetic identity fraud is a sophisticated tactic where criminals combine real and fake personal data to create entirely new identities. These "Frankenstein" identities are used to open accounts, build credit histories, and eventually secure loans they have no intention of repaying.

Fraudsters often let these accounts remain dormant or process small, legitimate-looking transactions to build trust. This "warming" phase can stretch over months, making it hard for traditional verification systems to detect.

AI startups are particularly vulnerable. Around 7.4% of customer sign-ups in AI companies are linked to suspected multi-account abuse. Startups offering self-service sign-ups or direct API access face even greater risks, experiencing 10 times more abuse attempts than enterprise-level solutions. Fraudsters exploit these platforms to access expensive computing resources using multiple fake accounts.

While external threats are a major concern, startups cannot ignore the dangers lurking within their own organizations.

Insider Threats and Financial Manipulation

Insider fraud occurs when employees, contractors, or partners abuse their access for personal gain. These threats are tough to identify because insiders use legitimate credentials, and their actions often resemble everyday administrative tasks.

On average, businesses lose 5% of their annual revenue to fraud, with median losses of about $145,000 per case. Over 60% of companies report experiencing some form of payment fraud, often involving schemes like fake vendors or inflated invoices. A common tactic is to submit multiple payments just below approval thresholds - such as several $4,950 payments to avoid triggering a $5,000 review requirement.

Most traditional security systems focus on external threats, leaving insider fraud undetected. Behavioral analytics can help by establishing "normal" patterns and flagging unusual activities, such as odd login times, unauthorized data access, or employees who avoid taking vacations - a potential red flag for fraud.

What Is Behavioral Analytics and How Does It Prevent Fraud?

Behavioral analytics focuses on tracking "digital body language" - the actions a user performs rather than just their identity. Instead of asking "Who is this person?" it shifts the question to "How is this person behaving?" By analyzing micro-interactions like keystrokes, mouse movements, pauses, clicks, and typing speed, it uncovers intent. This approach highlights fraud signals that traditional, static controls often miss.

For example, a legitimate user is unlikely to hesitate when entering their own name or Social Security number. On the other hand, a fraudster working with stolen credentials might pause, make corrections, or rely on copy-pasting unfamiliar information. The results are impressive: behavioral analytics can detect up to 90% of fraud with 99% accuracy, keeping false positives below 1%.

Josh Eurom, Manager of Fraud at Aspiration Banking, shared the impact of this approach:

"With NeuroID at the top of our funnel, we implemented automatic denial based on the risky signal, saving us additional API calls and reviews. And we're capturing roughly four times more fraud".

This method provides a proactive way to spot fraud, setting the stage for a deeper dive into how these behavioral insights work.

How Behavioral Analytics Works

Behavioral analytics evaluates user interactions before submission, monitoring every action leading up to the "submit" button. It examines patterns like dwell time and keystroke rhythm. For instance, spending less than 0.5 seconds on a page or typing with perfectly consistent keystrokes can indicate bot activity rather than human behavior. This level of precision is invaluable for startups combating rapid, automated fraud attempts.

Advanced systems can even recognize fraud bots by detecting specific frameworks like Puppeteer or Stealth based on their behavioral patterns. Beyond bots, these systems also identify coercion and scams in real time. Hesitation or repeated corrections during a transaction often point to someone being coached by a scammer.

In a striking example from March 2026, a Sardine customer used an AI Data Analyst Agent to combine device fingerprints with true IP detection. This uncovered a massive 150,000-account fraud ring in just 11 minutes, a task that previously required extensive manual SQL analysis.

By analyzing user behavior, these systems go beyond traditional fraud detection, offering a proactive and efficient approach.

Advantages Over Older Fraud Detection Methods

Unlike older, reactive methods that rely on spotting known attack patterns, behavioral analytics is proactive. It identifies anomalies in how users interact with a platform, catching unknown threats early on. This approach allows fraud teams to distinguish between legitimate spikes in activity - like a successful marketing campaign - and coordinated bot attacks, providing critical context for effective action.

Another key advantage is that behavioral analytics operates at the top of the onboarding funnel. By automatically denying bots and high-risk users early, it prevents unnecessary third-party API calls or manual reviews, saving time and money. For genuine users, this means a smoother experience. Mauro Jacome, Head of Data Science at Addi, explained:

"Using NeuroID decisioning, we can confidently reject bad actors today who we used to take to step-up. We also have enough information on good applicants sooner, so we can fast-track them".

Additionally, this method can reduce false positive alerts by 73% to 75%, ensuring fewer legitimate customers face unnecessary blocks. Unlike behavioral biometrics, which link data to specific identities and often face regulatory challenges, behavioral analytics focuses solely on actions and intent. This makes it easier to comply with privacy laws while maintaining effectiveness.

How to Implement Behavioral Analytics in Your Startup

Tackling fraud effectively requires startups to embrace behavioral analytics, but the good news is that you don’t need a massive team or a bottomless budget to get started. The secret lies in setting clear goals and building your system step by step. Start by pinpointing the specific fraud risks your business faces - whether it’s account takeovers, card testing, or promo abuse. Then, establish measurable targets, like keeping false positives below 0.5% and ensuring decision latency stays under 100 milliseconds.

The implementation process revolves around three key areas: collecting real-time data, deploying models to identify fraud patterns, and integrating insights into your financial operations. Each of these steps works together to create a system that evolves alongside emerging fraud tactics. Let’s break down these steps further.

Real-Time Data Collection and Monitoring

The foundation of fraud prevention is high-quality, real-time data. Start by implementing a unified SDK to track behavioral signals - keystrokes, mouse movements, typing speed, and device fingerprints - throughout the entire user journey. This means monitoring every interaction from account creation to payment. To manage this constant data flow efficiently, many systems rely on event streaming platforms.

Once you’ve captured the raw data, enrich it with third-party verification sources like phone, email, and banking data for real-time identity validation. Advanced techniques, such as "True Piercing", can help counteract VPNs, emulators, and remote access tools, ensuring the data you collect is as accurate as possible.

Training and Deploying Machine Learning Models

For startups, starting with pre-trained machine learning models is often the most practical approach. Models like XGBoost or LightGBM are particularly effective for fraud detection because they handle tabular data well and can deliver results in just 10 to 20 milliseconds. These models analyze both "velocity counters" (e.g., how many transactions a card processes in five minutes) and behavioral features, such as comparing a current transaction to a user’s 30-day average.

Before going live, test these models in shadow mode for 30 to 90 days using historical data. This step helps fine-tune performance and minimizes the risk of false positives during live operations. Matt Vega, Director of Fraud Strategy, highlights the importance of this testing phase:

"My favorite Sardine feature is that I can create complex rulesets to catch new fraud patterns, and then test them against the last 30/60/90 days. If they perform well, I can instantly push them to production. That's game-changing."

Once deployed, assign risk scores to specific actions. For instance, low-risk users might get automatic approval, medium-risk cases could trigger multi-factor authentication, and high-risk situations may result in immediate blocks. Incorporating feedback loops - such as feeding chargeback outcomes back into the system - ensures your models continuously adapt to new fraud tactics. Since fraud typically impacts less than 1% of transactions, focus on precision-recall metrics rather than overall accuracy when evaluating model performance.

Using Behavioral Analytics in Financial Systems

Behavioral analytics can also transform how startups manage financial operations, providing early warnings of suspicious activity before any damage occurs. Whether it’s payments, bookkeeping, or investor reporting, these insights can identify anomalies like unauthorized logins or unusual transaction patterns.

For example, platforms like Lucid Financials use behavioral analytics to monitor interactions with sensitive financial data. Subtle red flags - such as hesitation when entering familiar account details or repeated corrections - can trigger alerts before fraudulent transactions are processed. On the technical side, a feature store ensures consistency between training and production environments, enabling real-time scoring with sub-millisecond lookup speeds. This keeps decision latency under 100 milliseconds, allowing the system to integrate seamlessly into payment authorization workflows.

Benefits of Behavioral Analytics for Startups

Behavioral analytics offers three key benefits for startups: better fraud detection, improved customer experience, and increased operational efficiency.

Better Fraud Detection Accuracy

Behavioral analytics can detect fraudulent activity that traditional methods often miss. Instead of relying solely on static data like passwords or IP addresses, it analyzes user behavior - things like typing speed, mouse movements, and scrolling patterns. This creates a digital "body language" that’s much harder for fraudsters to mimic.

For example, financial institutions using AI-driven behavioral systems have intercepted 94.3% of fraud attempts before any money was lost, compared to just 23.8% with older systems. Startups implementing these systems can see fraud detection rates jump from 94% to 99.2%. Traditional methods often lag behind, taking over 17 days to identify new attack patterns. In contrast, behavioral models with continuous learning can adapt in just 3.2 hours. One fintech platform handling over 100 million monthly transactions reduced its fraud detection time from 17.3 days to 3.2 hours. This led to a 4.7x improvement in catching new fraud types within 30 days and a 64% reduction in losses from emerging threats.

These advancements not only improve security but also create a smoother experience for legitimate customers.

Fewer False Alarms and Better Customer Experience

False positives - when legitimate customers are mistakenly flagged as fraudsters - can harm your business. Research shows that 15% to 25% of falsely declined customers may never return. Worse, 68% share their bad experiences with friends and family, and 34% post about it on social media.

Behavioral analytics minimizes these false alarms. Advanced systems can cut false positive rates by up to 76.8% annually. By providing deeper context, they help fraud teams distinguish between real threats, like bot attacks, and harmless spikes in activity, such as those from marketing campaigns. This ensures legitimate transactions aren’t interrupted.

Speed is equally critical. Slow fraud analysis can make checkout processes feel glitchy, leading to cart abandonment. For instance, if analysis delays hit 300ms, mobile checkout abandonment can rise by 23%, and e-commerce conversions may drop by 17%. One mid-market payment processor tackled this issue by adopting a tiered behavioral system, reducing latency from 280ms to 65ms - a 76% improvement. This change cut customer churn from 23% to 9%, saving the company $33.6 million in retained lifetime value.

By reducing false positives and improving transaction speeds, behavioral analytics protects customer trust while boosting revenue.

Cost Savings and Efficiency Gains

Behavioral analytics also cuts costs by automating fraud detection, saving countless hours of manual review. A mid-sized payment processor, for example, saved 34,000 analyst hours annually by automating routine tasks. This allows fraud teams to focus on the small percentage of transactions - typically 2–3% - that require human judgment.

False positives are expensive. They waste marketing dollars and increase support costs. Reducing these errors not only protects customer acquisition investments but also streamlines operational expenses.

Piyoosh Rai, Founder & CEO of The Algorithm, explains it well:

"The goal isn't zero fraud. The goal is optimal fraud... the point where the marginal cost of preventing additional fraud exceeds the marginal benefit."

Behavioral analytics helps businesses find this balance. It catches more fraud while keeping the customer experience smooth, allowing startups to focus on growth. With tools like these, platforms such as Lucid Financials can deliver real-time insights and robust fraud prevention, giving startups the confidence to scale.

Conclusion

In a world where threats evolve faster than traditional security measures can keep up, behavioral analytics offers startups a smarter way to stay ahead. Fraud is becoming increasingly sophisticated, with over 50% of incidents now driven by AI-powered attacks. Relying on outdated, rules-based systems isn't just ineffective - it can also alienate genuine customers. Behavioral analytics changes the game by focusing on human intent and context rather than static signals, leading to measurable gains in fraud prevention.

For example, advanced behavioral analytics platforms have been shown to improve fraud detection rates by 62% while reducing false positives by 73%, compared to older systems. These improvements not only save countless hours of manual work but also drastically cut chargebacks and create smoother customer experiences. The result? Protected revenue, enhanced trust, and a more efficient fraud prevention strategy. This makes it clear that integrating fraud prevention with broader financial management isn't just a good idea - it's essential.

Fraud prevention works best when it’s part of a unified system. Combining financial management, real-time risk monitoring, and fraud detection into a single platform allows startups to identify anomalies faster, respond to threats immediately, and maintain accurate, investor-ready financial records - all without the hassle of managing multiple vendors. This streamlined approach boosts ROI and frees up your team to concentrate on growth instead of chasing down fragmented data.

Take Lucid Financials, for instance. It brings together AI-driven bookkeeping, tax services, and CFO support, all integrated with real-time Slack updates. This gives founders clear, up-to-date financial insights and the ability to maintain clean, investor-ready books in just seven days. With proactive alerts and always-on reporting, you’re never caught off guard - whether you're gearing up for fundraising or navigating rapid growth. Pair this with behavioral analytics protecting your transactions, and you’ve got the tools to focus on what truly matters: growing your business.

FAQs

What user behaviors are the strongest fraud signals?

The clearest signs of fraud include failed login attempts, unexpected navigation behaviors, switching devices, and patterns of coordinated bot activity. Using behavioral analytics, these red flags can be spotted in real time, making it easier to catch potential fraud as it happens.

How do you add behavioral analytics without slowing checkout?

To incorporate behavioral analytics while keeping checkout speeds intact, rely on real-time, automated analysis tools. These systems can evaluate behavioral patterns and customer identity in just milliseconds, spotting potential fraud without slowing down transactions. Additionally, advanced solutions create profiles of typical customer behavior, allowing them to flag unusual activity instantly. This approach ensures a smooth user experience while strengthening fraud detection efforts.

How do you handle privacy and consent for behavioral data?

When it comes to using behavioral data for fraud prevention, privacy and consent are non-negotiable. Organizations must prioritize transparency by clearly explaining to users how their data is collected and used. This includes securing explicit consent and ensuring compliance with privacy laws like the California Consumer Privacy Act (CCPA) and General Data Protection Regulation (GDPR).

Behavioral analytics typically collects non-identifiable information, such as typing patterns or mouse movements, often in a passive manner. To protect user privacy while effectively preventing fraud, companies should follow key principles like data minimization - only collecting what’s necessary - and ensuring secure storage of this information. This careful balance helps maintain trust while addressing security concerns.